Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper proposes a novel method for sparse latent factor modeling using a new sparse asymptotic Principal Component Analysis (APCA). This approach analyzes the co-movements of large-dimensional pan...

Ridge regression is an indispensable tool in big data econometrics but suffers from bias issues affecting both statistical efficiency and scalability. We introduce an iterative strategy to correct t...

This paper proposes a novel dynamic forecasting method using a new supervised Principal Component Analysis (PCA) when a large number of predictors are available. The new supervised PCA provides an e...

This paper proposes a new approach to identifying the effective cointegration rank in high-dimensional unit-root (HDUR) time series from a prediction perspective using reduced-rank regression. For a...

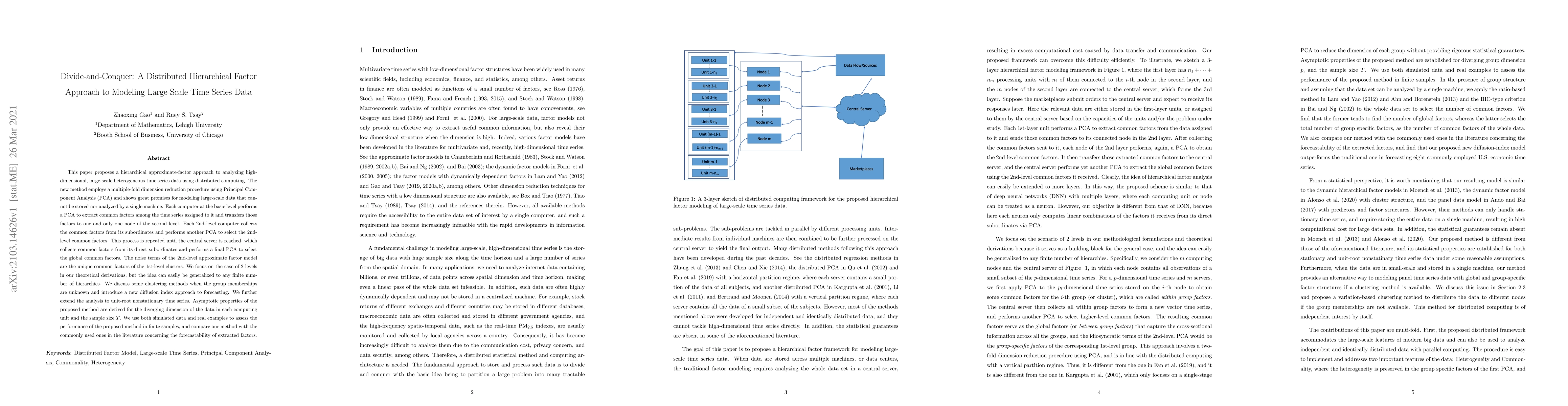

This paper proposes a hierarchical approximate-factor approach to analyzing high-dimensional, large-scale heterogeneous time series data using distributed computing. The new method employs a multipl...

We propose a new framework for modeling high-dimensional matrix-variate time series by a two-way transformation, where the transformed data consist of a matrix-variate factor process, which is dynam...

This paper proposes a new procedure to build factor models for high-dimensional unit-root time series by postulating that a $p$-dimensional unit-root process is a nonsingular linear transformation o...

Modeling matrix-valued time series is an interesting and important research topic. In this paper, we extend the method of Chang et al. (2017) to matrix-valued time series. For any given $p\times q$ ...

This article considers a novel and widely applicable approach to modeling high-dimensional dependent data when a large number of explanatory variables are available and the signal-to-noise ratio is lo...

Matrix-variate time series data are increasingly popular in economics, statistics, and environmental studies, among other fields. This paper develops regularized estimation methods for analyzing high-...

Factor-based forecasting using Principal Component Analysis (PCA) is an effective machine learning tool for dimension reduction with many applications in statistics, economics, and finance. This paper...

We investigate forward variable selection for ultra-high dimensional linear regression using a Gram-Schmidt orthogonalization procedure. Unlike the commonly used Forward Regression (FR) method, which ...

This paper proposes a novel diffusion-index model for forecasting when predictors are high-dimensional matrix-valued time series. We apply an $\alpha$-PCA method to extract low-dimensional matrix fact...

This paper investigates estimation and inference of a Spatial Arbitrage Pricing Theory (SAPT) model that integrates spatial interactions with multi-factor analysis, accommodating both observable and l...

In this paper, we propose a distributed framework for reducing the dimensionality of high-dimensional, large-scale, heterogeneous matrix-variate time series data using a factor model. The data are fir...

Estimating a sparse covariance matrix is a fundamental problem in high-dimensional statistics. However, thresholding methods developed for independent data are generally not directly applicable to hig...

This paper develops a canonical-correlation-based method for detecting structural changes in high-dimensional transformed factor models. The proposed approach exploits the low-rank canonical-correlati...