Academic Profile

Statistics

Similar Authors

Papers on arXiv

Time-uniform log-Sobolev inequalities (LSI) satisfied by solutions of semi-linear mean-field equations have recently appeared to be a key tool to obtain time-uniform propagation of chaos estimates. ...

For a certain class of McKean--Vlasov processes, we introduce proxy processes that substitute the mean-field interaction with self-interaction, employing a weighted occupation measure. Our study enc...

We study the kinetic mean field Langevin dynamics under the functional convexity assumption of the mean field energy functional. Using hypocoercivity, we first establish the exponential convergence ...

Recently there is a rising interest in the research of mean field optimization, in particular because of its role in analyzing the training of neural networks. In this paper by adding the Fisher Inf...

We study the mean field Langevin dynamics and the associated particle system. By assuming the functional convexity of the energy, we obtain the $L^p$-convergence of the marginal distributions toward...

In the context of mean field games, with possible control of the diffusion coefficient, we consider a path-dependent version of the planning problem introduced by P.L. Lions: given a pair of margina...

We study two-layer neural networks in the mean field limit, where the number of neurons tends to infinity. In this regime, the optimization over the neuron parameters becomes the optimization over t...

This paper extends the results of Ma, Wu, Zhang, Zhang [11] to the context of path-dependent multidimensional forward-backward stochastic differential equations (FBSDE). By path-dependent we mean th...

We study the long time behavior of an underdamped mean-field Langevin (MFL) equation, and provide a general convergence as well as an exponential convergence rate result under different conditions. ...

We consider a general formulation of the random horizon Principal-Agent problem with a continuous payment and a lump-sum payment at termination. In the European version of the problem, the random ho...

Mean field games are concerned with the limit of large-population stochastic differential games where the agents interact through their empirical distribution. In the classical setting, the number o...

In this paper we present a variational calculus approach to Principal-Agent problem with a lump-sum payment on finite horizon in degenerate stochastic systems, such as filtered partially observed li...

In this paper, we study a regularised relaxed optimal control problem and, in particular, we are concerned with the case where the control variable is of large dimension. We introduce a system of me...

Our work is motivated by a desire to study the theoretical underpinning for the convergence of stochastic gradient type algorithms widely used for non-convex learning tasks such as training of neura...

We consider a moral hazard problem with multiple principals in a continuous-time model. The agent can only work exclusively for one principal at a given time, so faces an optimal switching problem. ...

The theory of backward SDEs extends the predictable representation property of Brownian motion to the nonlinear framework, thus providing a path-dependent analog of fully nonlinear parabolic PDEs. I...

Backward stochastic differential equations extend the martingale representation theorem to the nonlinear setting. This can be seen as path-dependent counterpart of the extension from the heat equati...

We investigate Gibbs measures for diffusive particles interacting through a two-body mean field energy. By uncovering a gradient structure for the conditional law, we derive sharp bounds on the size o...

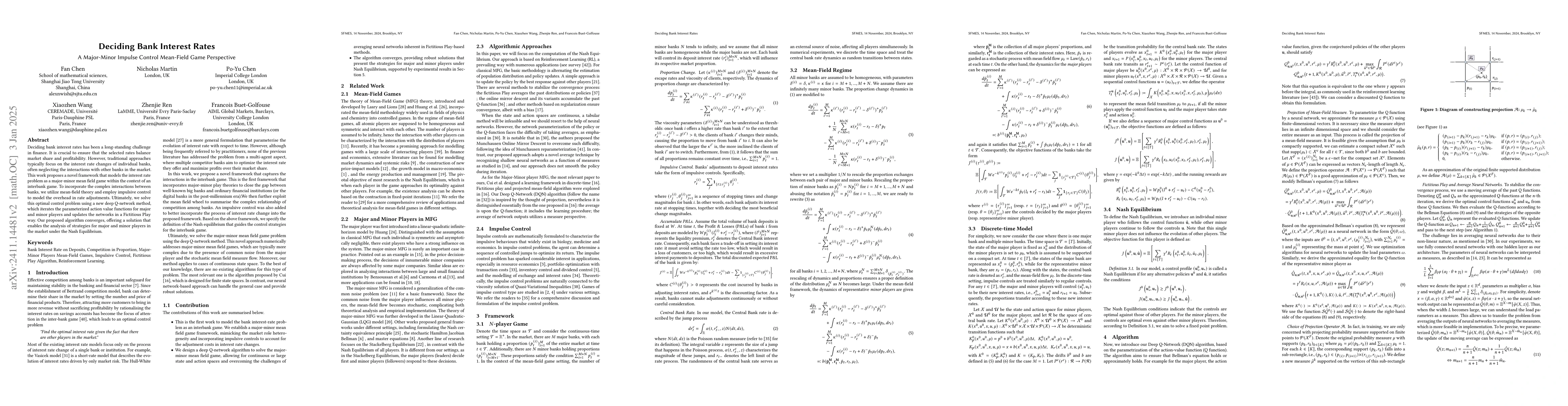

Deciding bank interest rates has been a long-standing challenge in finance. It is crucial to ensure that the selected rates balance market share and profitability. However, traditional approaches typi...

In this paper, we study the Entropic Martingale Optimal Transport (EMOT) problem on R. We begin by introducing the dual formulation and prove the exponential convergence of Sinkhorn's algorithm on the...

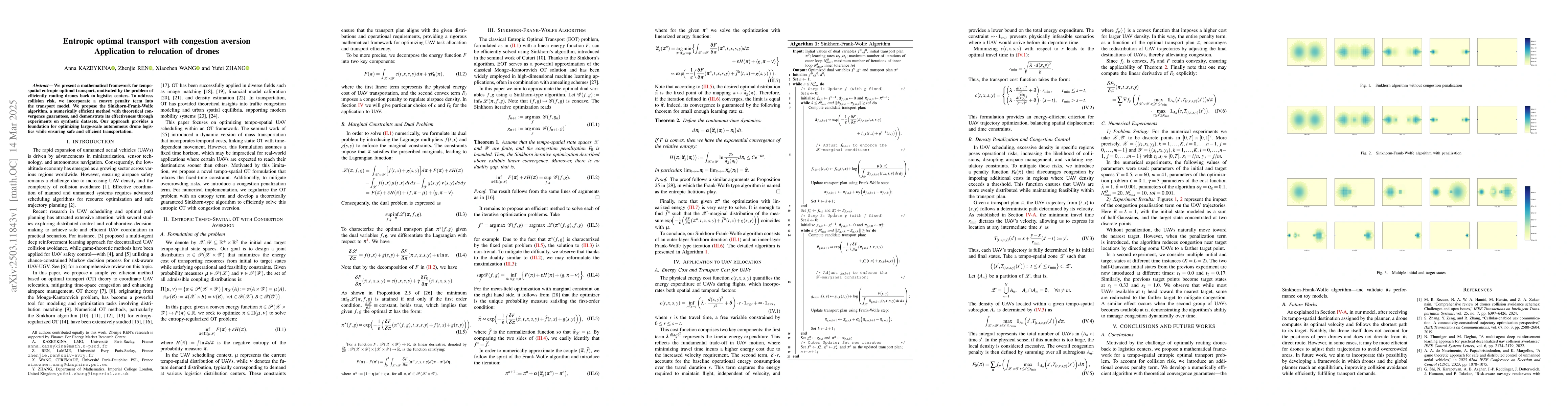

We present a mathematical framework for tempo-spatial entropic optimal transport, motivated by the problem of efficiently routing drones back to logistics centers. To address collision risk, we incorp...

Diffusion generative models have emerged as powerful tools for producing synthetic data from an empirically observed distribution. A common approach involves simulating the time-reversal of an Ornstei...

We study in this paper the weak propagation of chaos for McKean--Vlasov diffusions with branching, whose induced marginal measures are nonnegative finite measures but not necessary probability measure...

This paper is a continuation work of Ren et al. (2026) aiming to further devise q-learning algorithms for mean-field control (MFC) with controlled common noise. Based on the relaxed control formulatio...

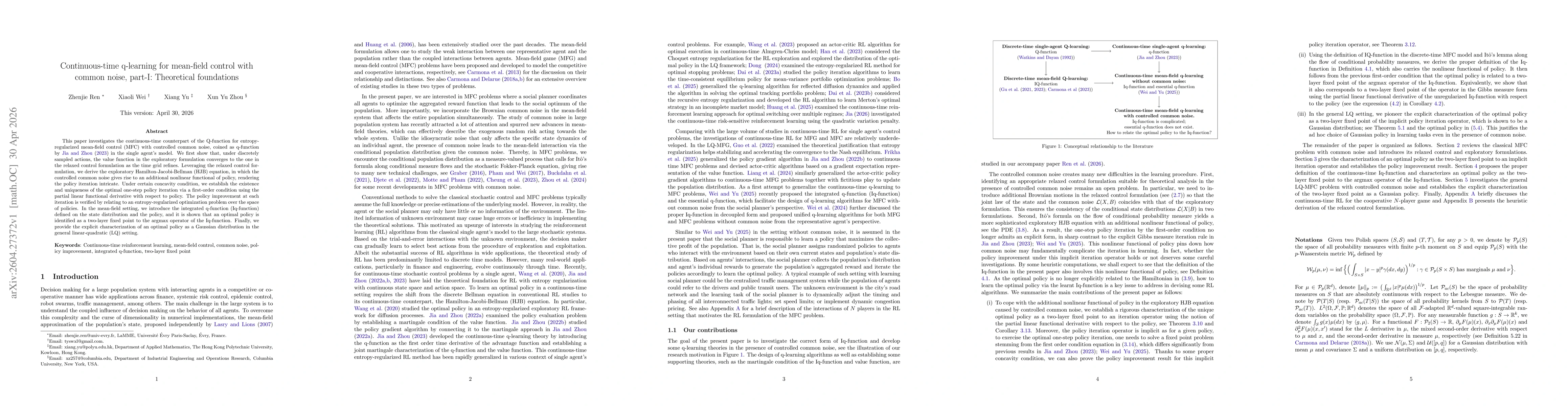

This paper investigates the continuous-time counterpart of the Q-function for entropy-regularized mean-field control (MFC) with controlled common noise, coined as q-function by Jia and Zhou (2023) in ...

Flow Matching has recently emerged as a popular class of generative models for simulating a target distribution $μ_1$ from samples drawn from a source distribution $μ_0$. This framework relies on a fi...

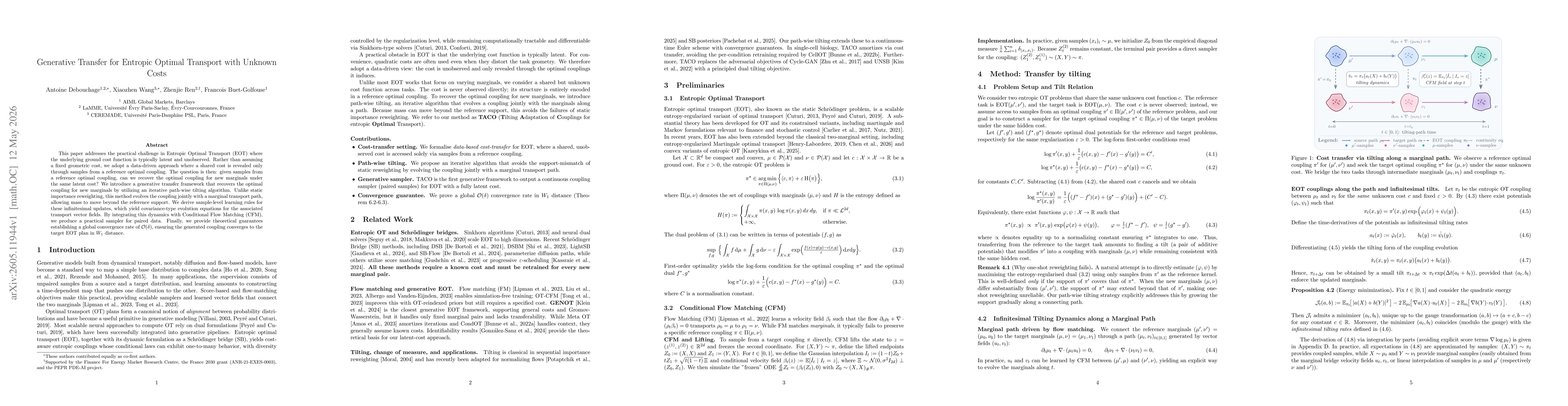

This paper addresses the practical challenge in Entropic Optimal Transport (EOT) where the underlying ground cost function is typically latent and unobserved. Rather than assuming a fixed geometric co...

Classical entropy regularization is poorly suited to continuous-time martingale transport, since relative entropy between diffusion laws typically forces their volatility characteristics to coincide. ...