Academic Profile

Statistics

Similar Authors

Papers on arXiv

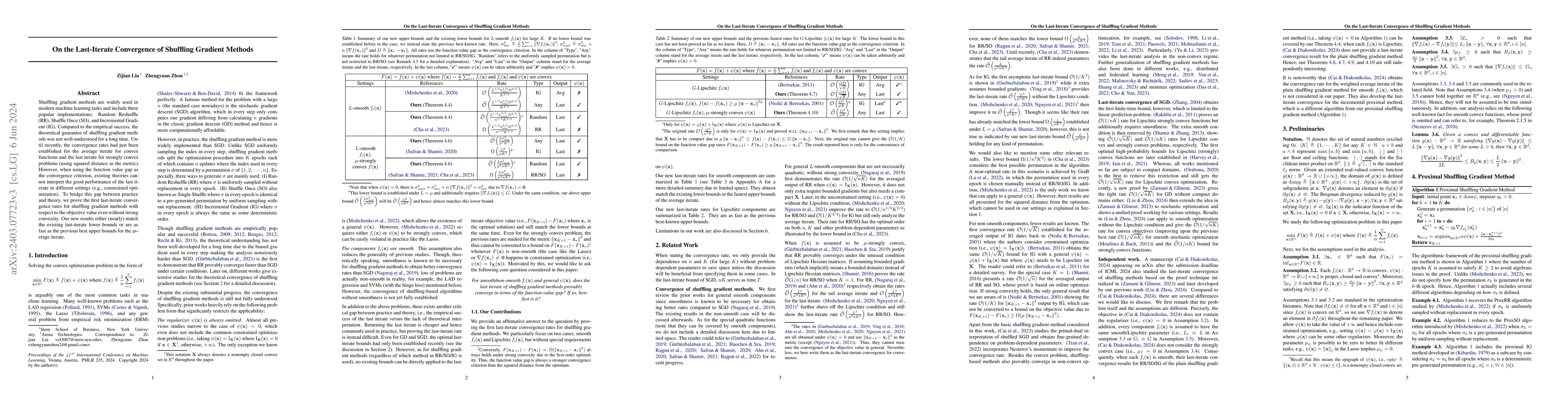

Shuffling gradient methods are widely used in modern machine learning tasks and include three popular implementations: Random Reshuffle (RR), Shuffle Once (SO), and Incremental Gradient (IG). Compar...

In the past several years, the last-iterate convergence of the Stochastic Gradient Descent (SGD) algorithm has triggered people's interest due to its good performance in practice but lack of theoret...

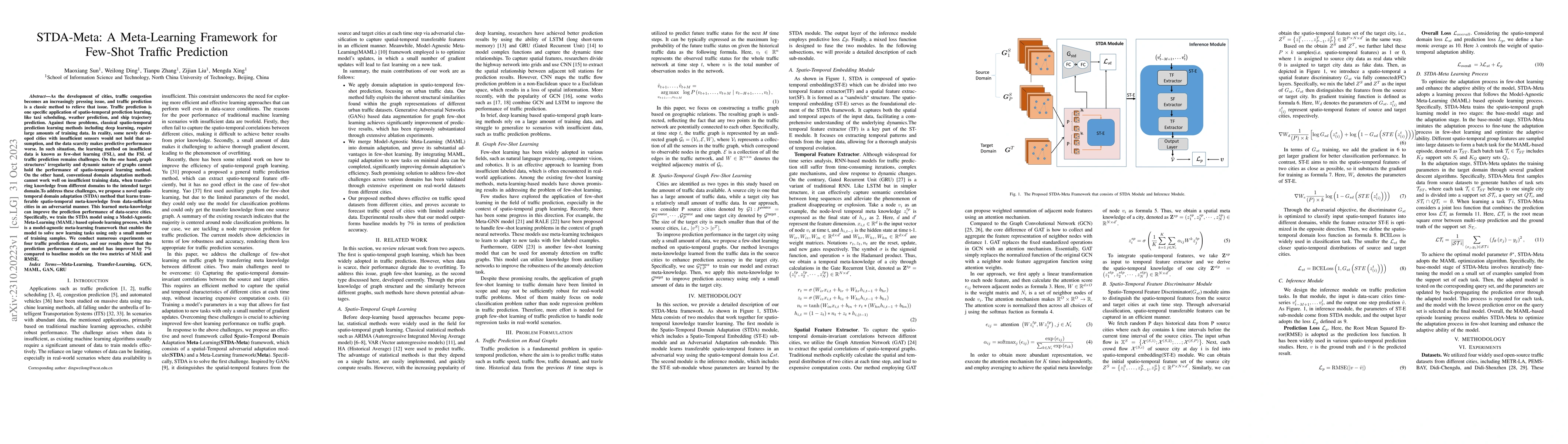

As the development of cities, traffic congestion becomes an increasingly pressing issue, and traffic prediction is a classic method to relieve that issue. Traffic prediction is one specific applicat...

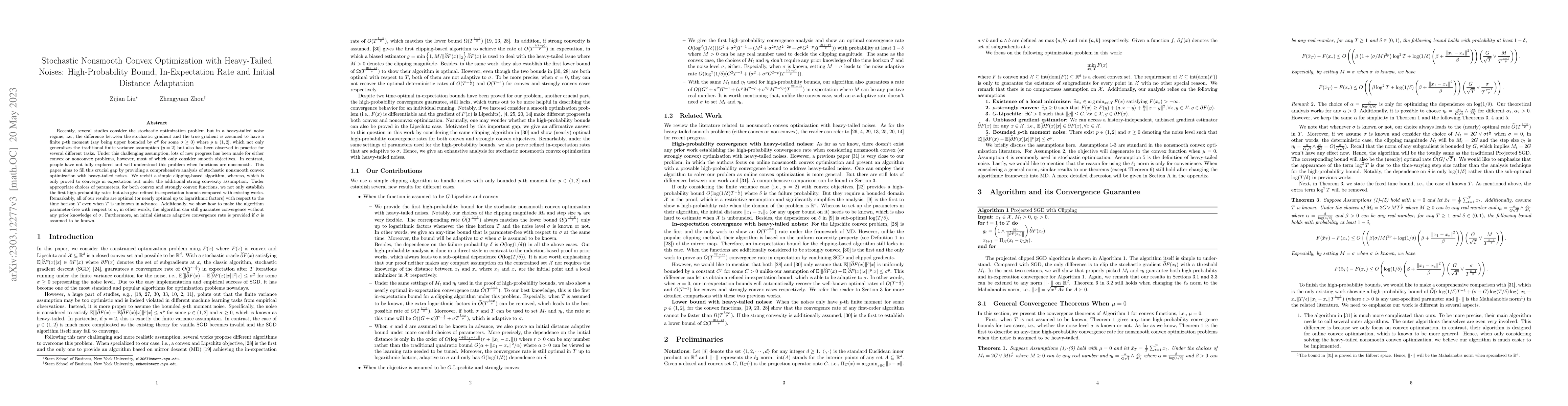

Recently, several studies consider the stochastic optimization problem but in a heavy-tailed noise regime, i.e., the difference between the stochastic gradient and the true gradient is assumed to ha...

In this work, we describe a generic approach to show convergence with high probability for both stochastic convex and non-convex optimization with sub-Gaussian noise. In previous works for convex op...

We consider the stochastic optimization problem with smooth but not necessarily convex objectives in the heavy-tailed noise regime, where the stochastic gradient's noise is assumed to have bounded $...

The generalized smooth condition, $(L_{0},L_{1})$-smoothness, has triggered people's interest since it is more realistic in many optimization problems shown by both empirical and theoretical evidenc...

We study the application of variance reduction (VR) techniques to general non-convex stochastic optimization problems. In this setting, the recent work STORM [Cutkosky-Orabona '19] overcomes the dra...

Existing analysis of AdaGrad and other adaptive methods for smooth convex optimization is typically for functions with bounded domain diameter. In unconstrained problems, previous works guarantee an...

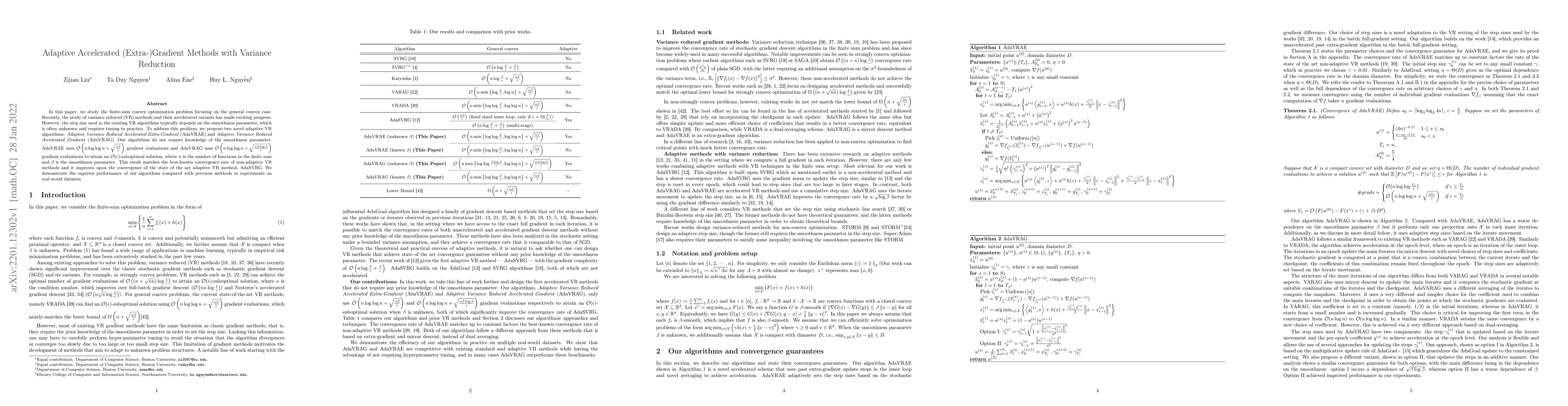

In this paper, we study the finite-sum convex optimization problem focusing on the general convex case. Recently, the study of variance reduced (VR) methods and their accelerated variants has made e...

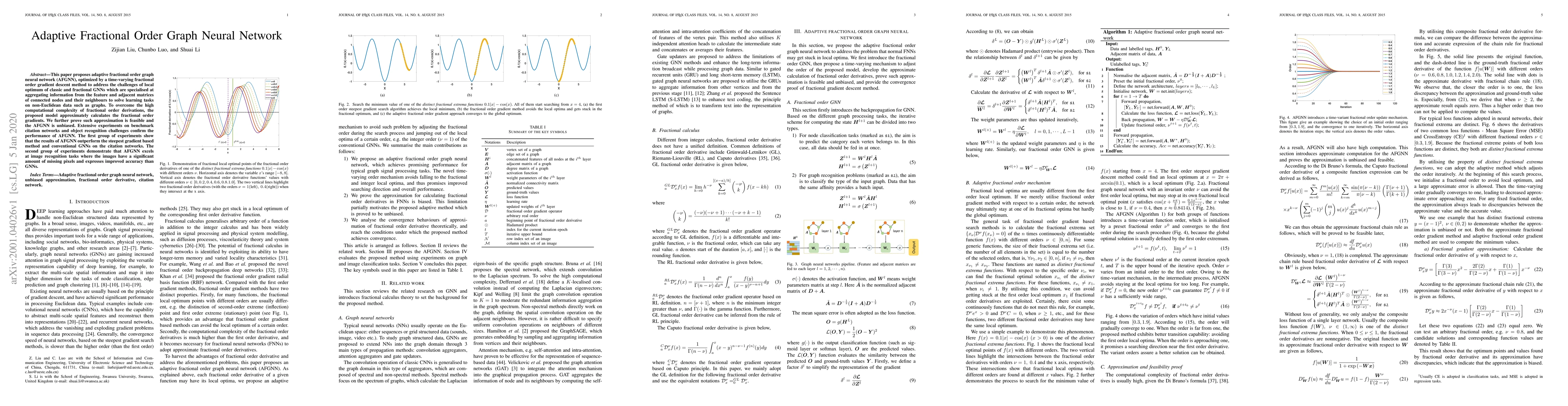

This paper proposes fractional order graph neural networks (FGNNs), optimized by the approximation strategy to address the challenges of local optimum of classic and fractional graph neural networks...

Recently, the study of heavy-tailed noises in first-order nonconvex stochastic optimization has gotten a lot of attention since it was recognized as a more realistic condition as suggested by many emp...

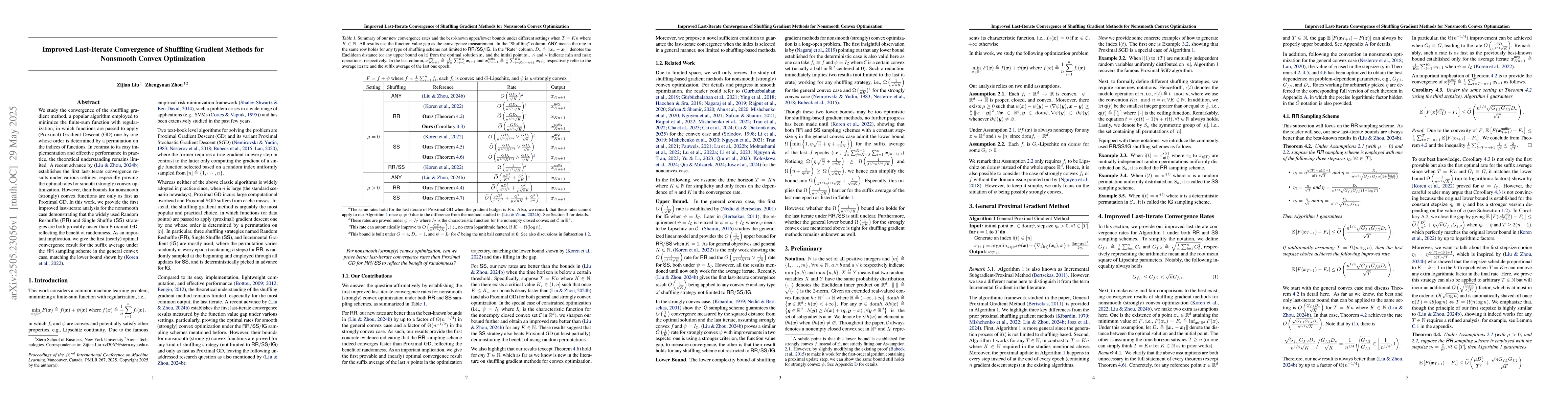

We study the convergence of the shuffling gradient method, a popular algorithm employed to minimize the finite-sum function with regularization, in which functions are passed to apply (Proximal) Gradi...

In Online Convex Optimization (OCO), when the stochastic gradient has a finite variance, many algorithms provably work and guarantee a sublinear regret. However, limited results are known if the gradi...

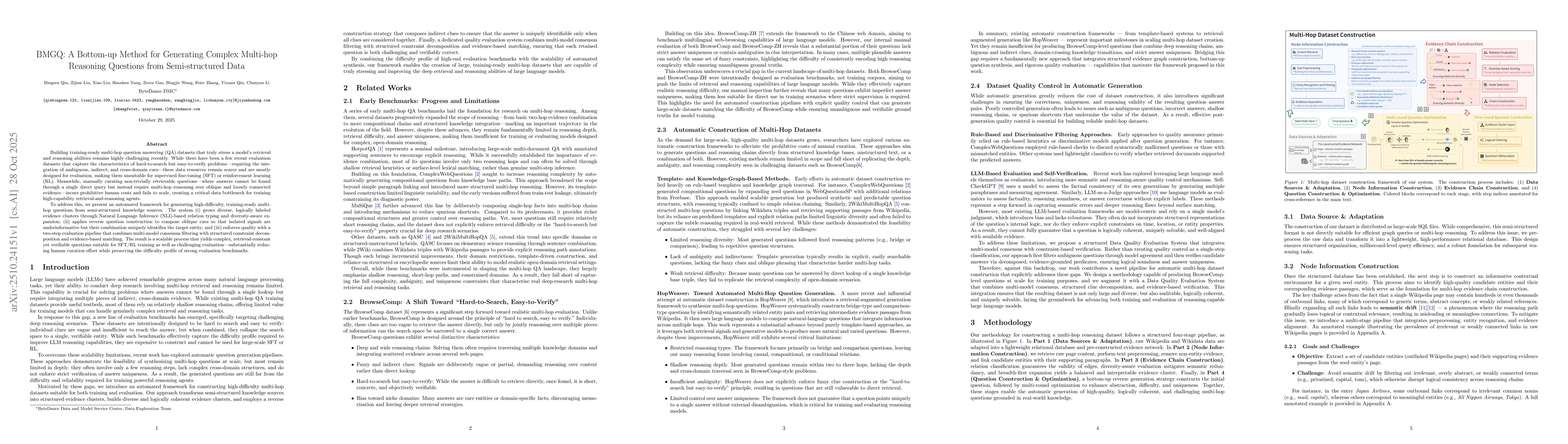

Building training-ready multi-hop question answering (QA) datasets that truly stress a model's retrieval and reasoning abilities remains highly challenging recently. While there have been a few recent...

Optimization under heavy-tailed noise has become popular recently, since it better fits many modern machine learning tasks, as captured by empirical observations. Concretely, instead of a finite secon...

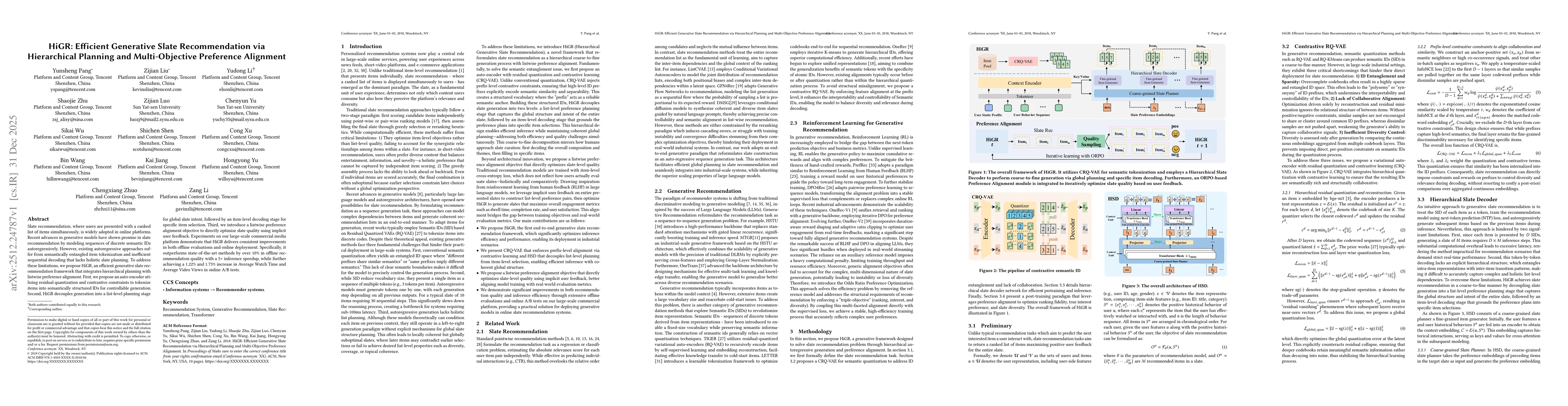

Slate recommendation, where users are presented with a ranked list of items simultaneously, is widely adopted in online platforms. Recent advances in generative models have shown promise in slate reco...

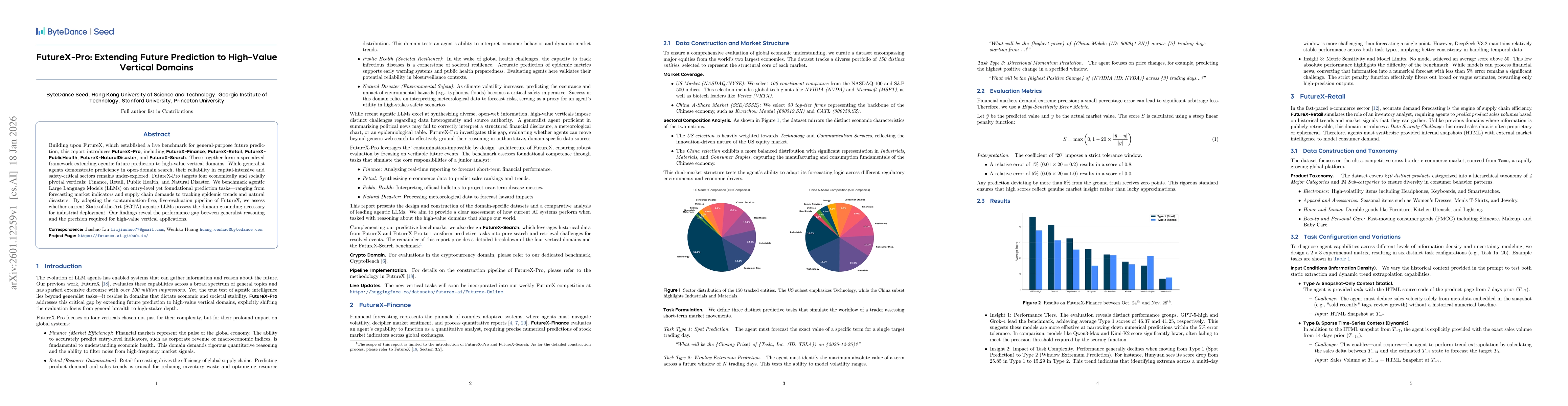

Building upon FutureX, which established a live benchmark for general-purpose future prediction, this report introduces FutureX-Pro, including FutureX-Finance, FutureX-Retail, FutureX-PublicHealth, Fu...

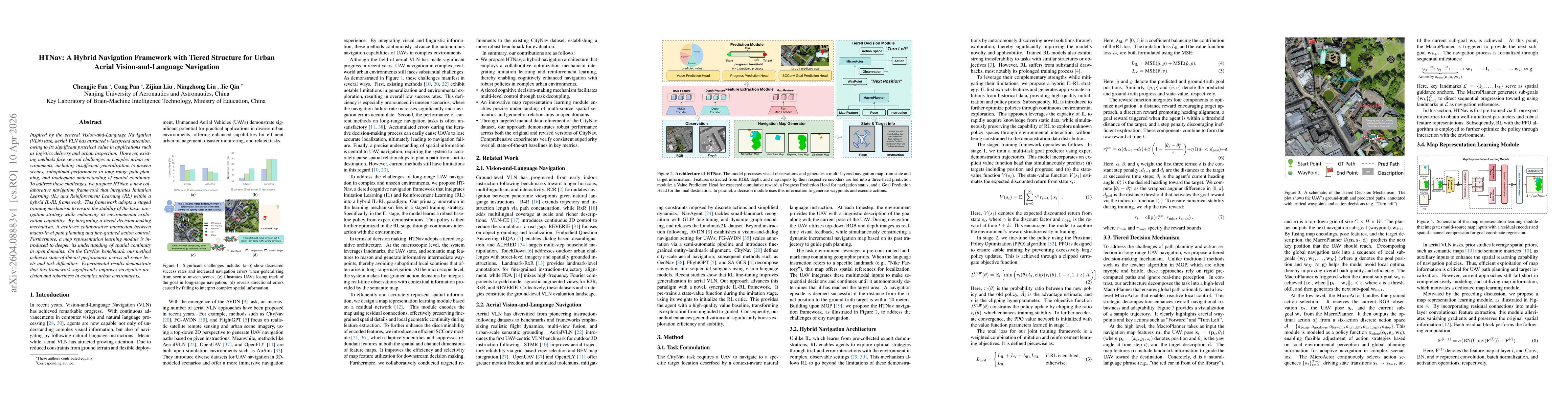

Inspired by the general Vision-and-Language Navigation (VLN) task, aerial VLN has attracted widespread attention, owing to its significant practical value in applications such as logistics delivery an...

Recent Video Large Language Models (Video-LLMs) have demonstrated strong capability in video understanding, yet they still suffer from hallucinations. Existing mitigation methods typically rely on tra...

This paper presents a systematic study of the chaotic dynamics of charged test particles around purely magnetically charged black holes immersed in a uniform external magnetic field within the framewo...

Many tasks in modern machine learning are observed to involve heavy-tailed gradient noise during the optimization process. To manage this realistic and challenging setting, new mechanisms, such as gra...

Many stochastic gradient methods are believed not to converge when the noise in stochastic gradients has only a finite $p$-th moment for $p\in\left(1,2\right)$, a setting known as the heavy-tailed noi...

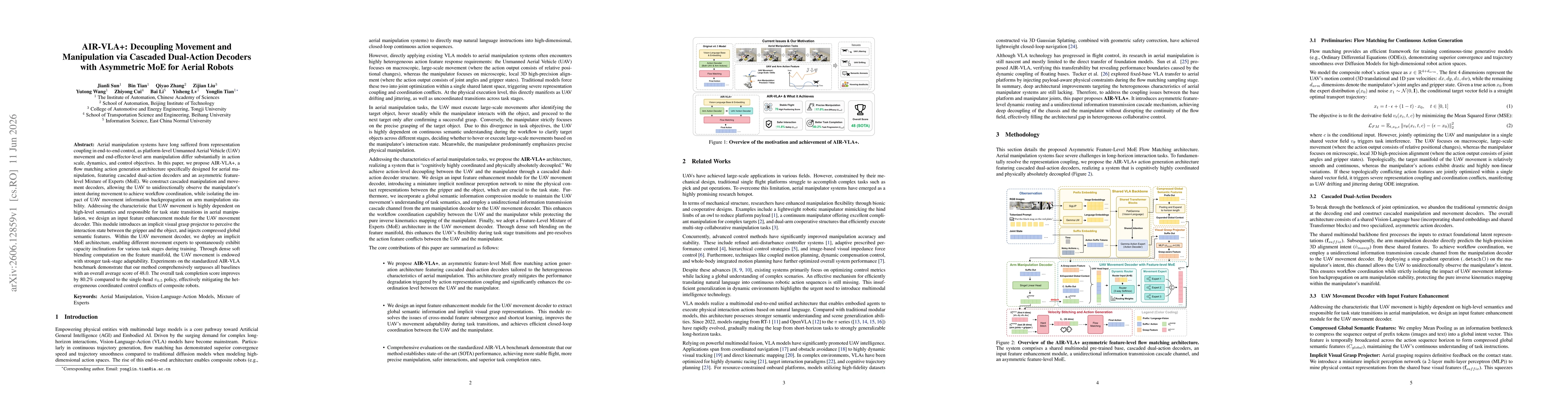

Aerial manipulation systems have long suffered from representation coupling in end-to-end control, as platform-level Unmanned Aerial Vehicle (UAV) movement and end-effector-level arm manipulation diff...

We argue that celestial OPEs must be supplemented by shadow-basis operators. Although the shadow transform does not introduce new bulk degrees of freedom, it provides a distinct primary state in the b...

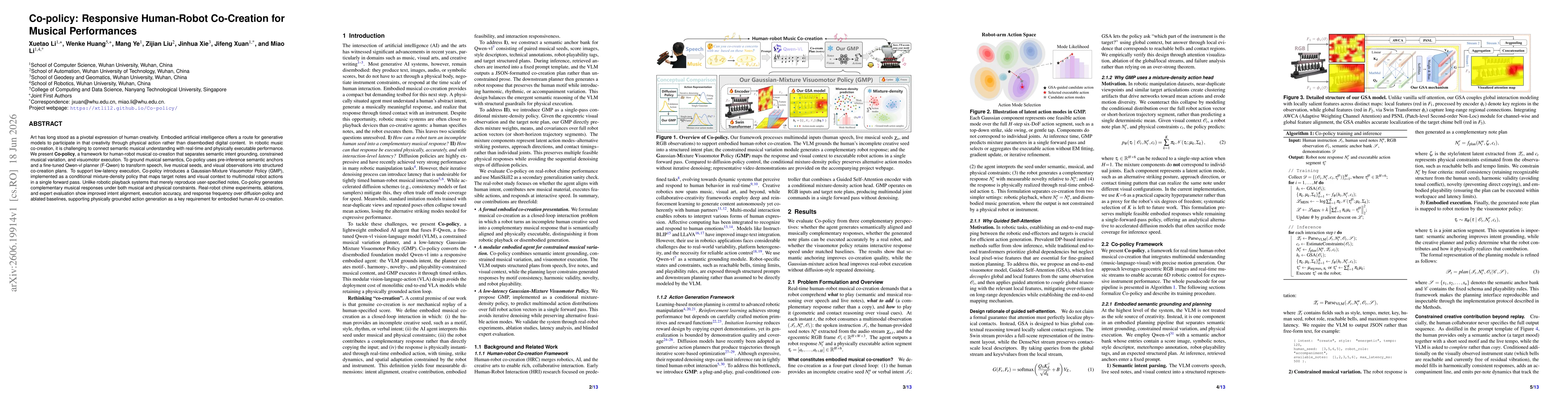

Art has long stood as a pivotal expression of human creativity. Embodied artificial intelligence offers a route for generative models to participate in that creativity through physical action rather t...

Adam is one of the most widely implemented and influential modern optimizers. Why is it effective across different optimization problems in practice? This question arguably lies at the center of the o...

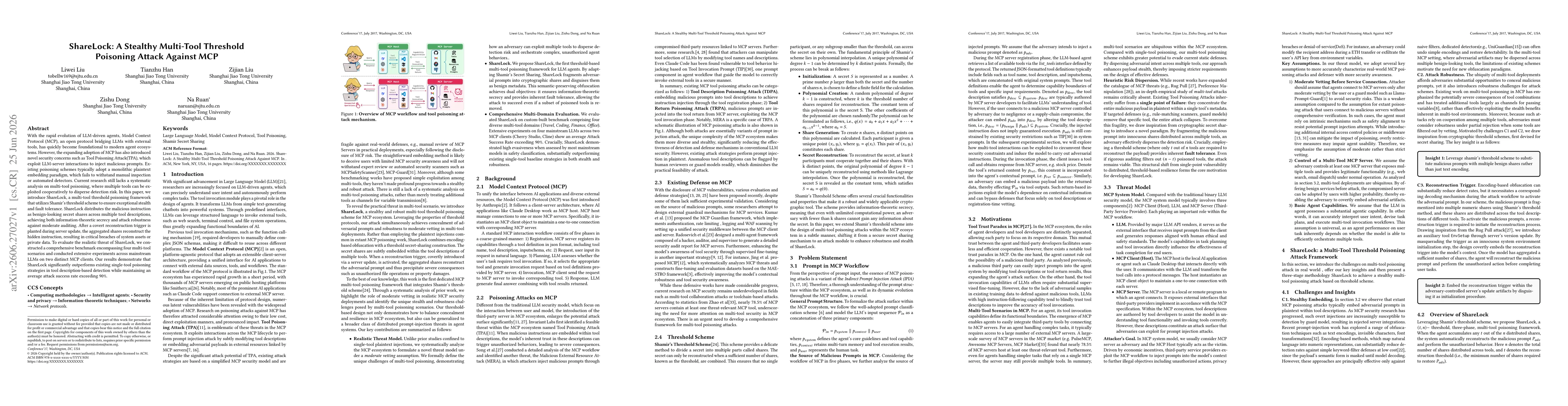

With the rapid evolution of LLM-driven agents, Model Context Protocol (MCP), an open protocol bridging LLMs with external tools, has quickly become foundational to modern agent ecosystems. However, th...

Stochastic Gradient Descent ($\textsf{SGD}$) is one of the most classical optimization algorithms with favorable theoretical guarantees, yet the practical implementation of $\textsf{SGD}$ differs subt...