Academic Profile

Statistics

Similar Authors

Papers on arXiv

Distributional Reinforcement Learning (RL) estimates return distribution mainly by learning quantile values via minimizing the quantile Huber loss function, entailing a threshold parameter often sel...

We show how D4PG can be used in conjunction with quantile regression to develop a hedging strategy for a trader responsible for derivatives that arrive stochastically and depend on a single underlyi...

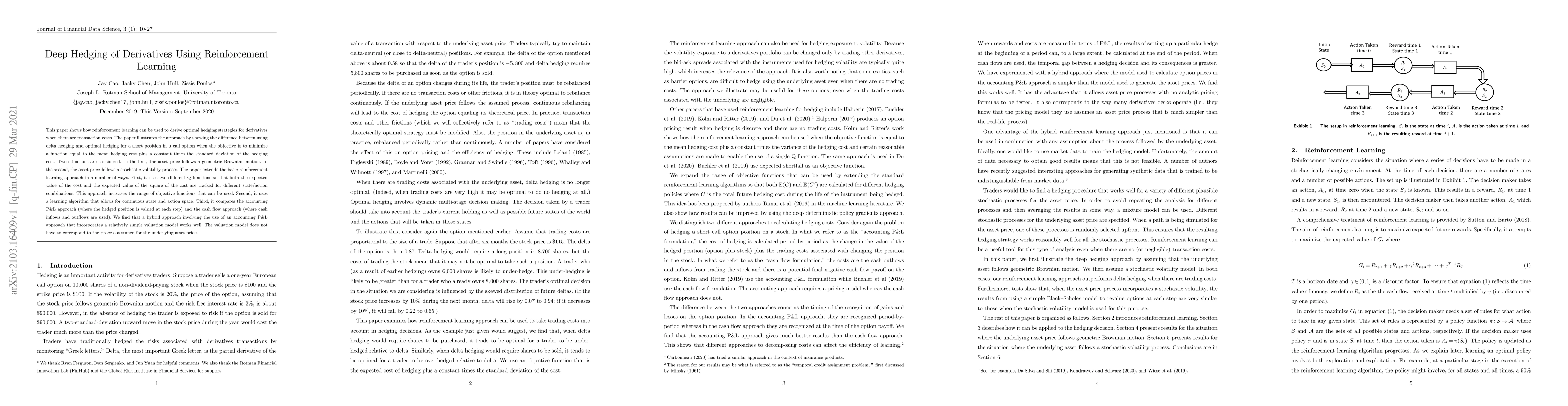

This paper shows how reinforcement learning can be used to derive optimal hedging strategies for derivatives when there are transaction costs. The paper illustrates the approach by showing the diffe...

A common approach to valuing exotic options involves choosing a model and then determining its parameters to fit the volatility surface as closely as possible. We refer to this as the model calibrat...

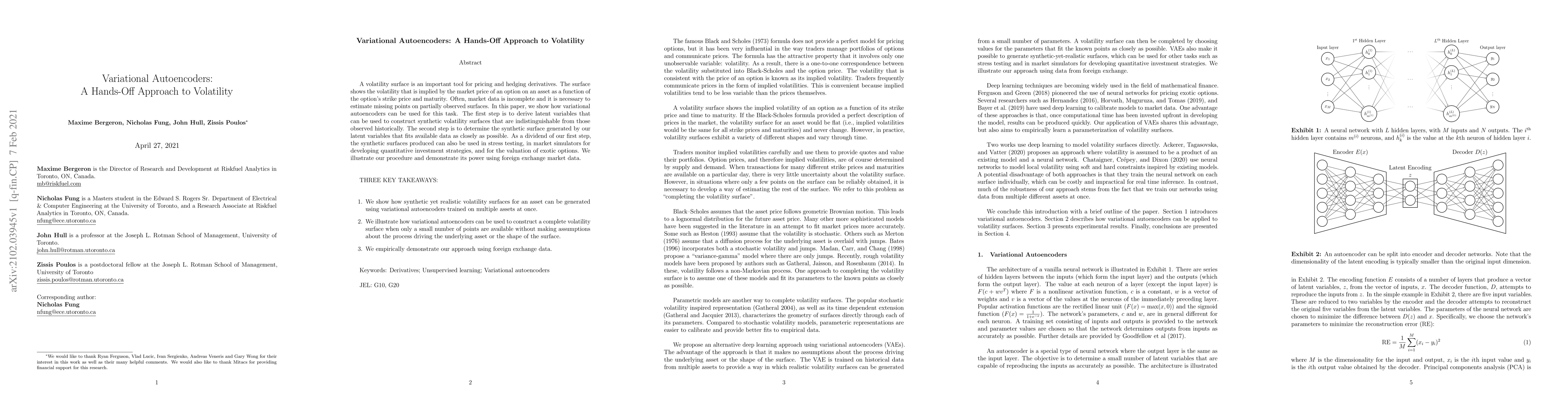

A volatility surface is an important tool for pricing and hedging derivatives. The surface shows the volatility that is implied by the market price of an option on an asset as a function of the opti...

We reduce training time in convolutional networks (CNNs) with a method that, for some of the mini-batches: a) scales down the resolution of input images via downsampling, and b) reduces the forward ...

Recent advancements in Distributional Reinforcement Learning (DRL) for modeling loss distributions have shown promise in developing hedging strategies in derivatives markets. A common approach in DRL ...

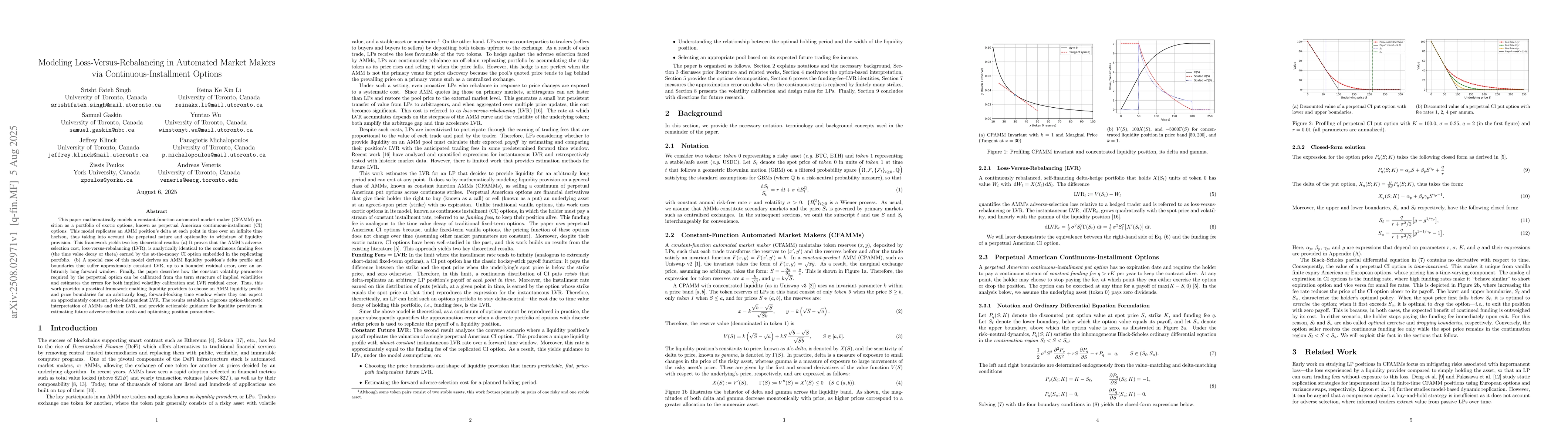

This paper mathematically models a constant-function automated market maker (CFAMM) position as a portfolio of exotic options, known as perpetual American continuous-installment (CI) options. This mod...