Academic Profile

Statistics

Similar Authors

Papers on arXiv

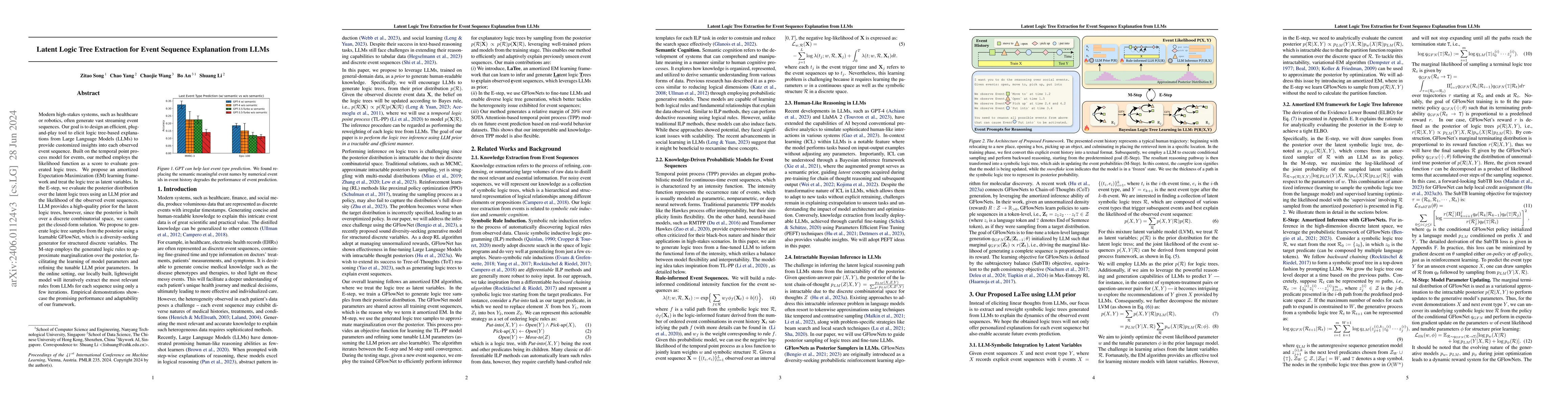

Modern high-stakes systems, such as healthcare or robotics, often generate vast streaming event sequences. Our goal is to design an efficient, plug-and-play tool to elicit logic tree-based explanation...

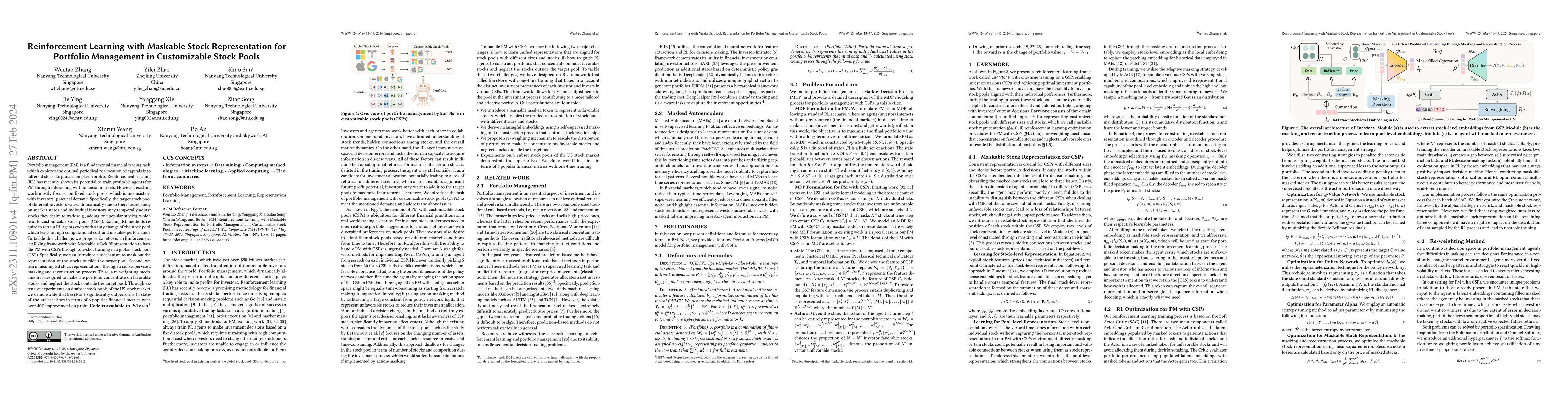

Portfolio management (PM) is a fundamental financial trading task, which explores the optimal periodical reallocation of capitals into different stocks to pursue long-term profits. Reinforcement lea...

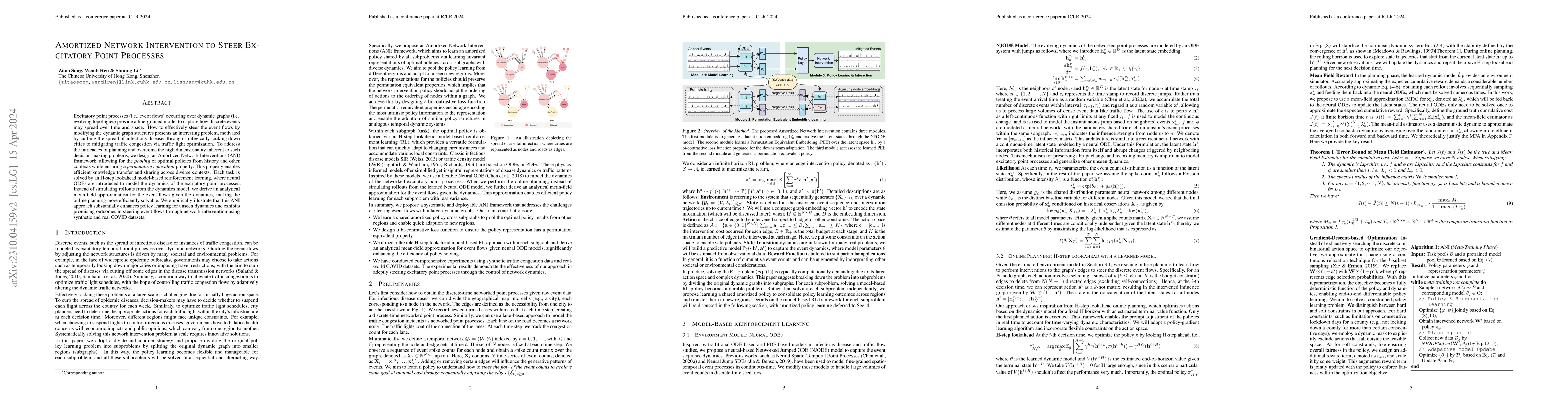

Excitatory point processes (i.e., event flows) occurring over dynamic graphs (i.e., evolving topologies) provide a fine-grained model to capture how discrete events may spread over time and space. H...

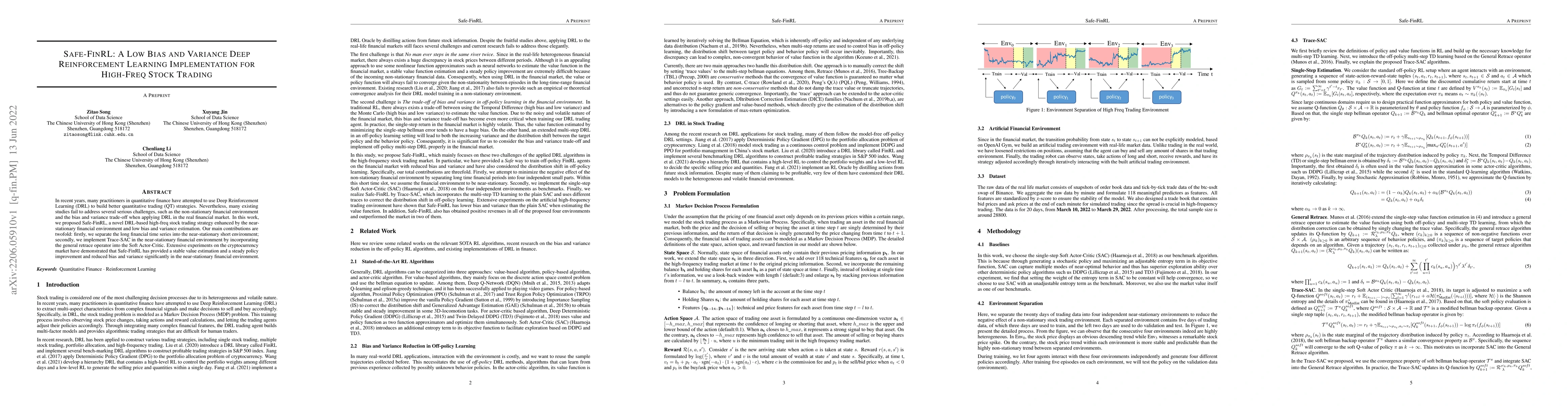

In recent years, many practitioners in quantitative finance have attempted to use Deep Reinforcement Learning (DRL) to build better quantitative trading (QT) strategies. Nevertheless, many existing ...

Adaptive methods like Adam have become the $\textit{de facto}$ standard for large-scale vector and Euclidean optimization due to their coordinate-wise adaptation with a second-order nature. More recen...

Training instabilities such as loss spikes are frequently the result of stochastic gradient noise. Because of rare expressions in language training data, and multiple layer composition, the noise impa...