Academic Profile

Statistics

Similar Authors

Papers on arXiv

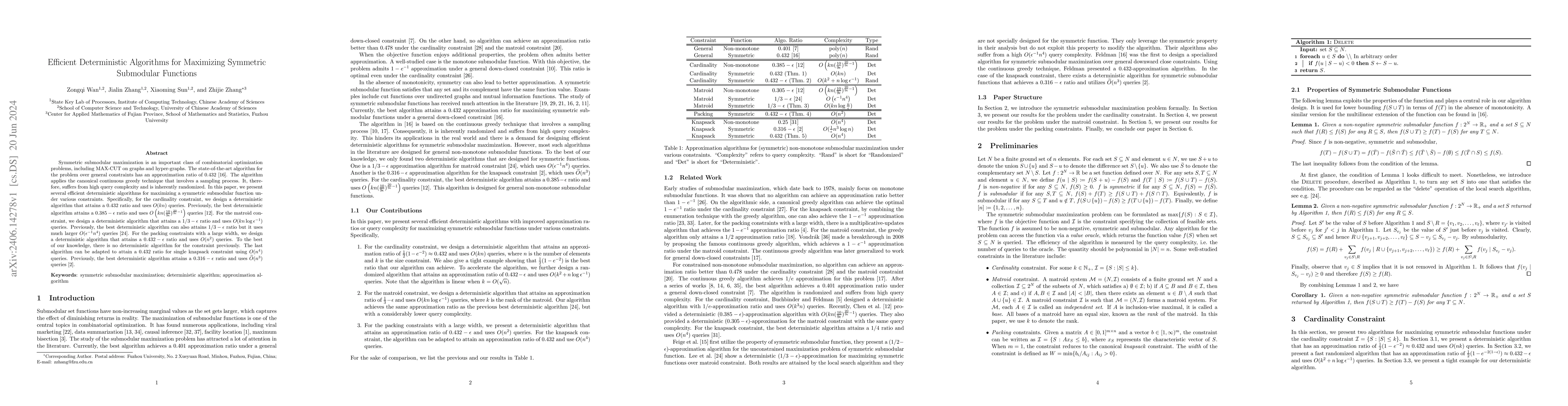

Symmetric submodular maximization is an important class of combinatorial optimization problems, including MAX-CUT on graphs and hyper-graphs. The state-of-the-art algorithm for the problem over gene...

Projected Gradient Ascent (PGA) is the most commonly used optimization scheme in machine learning and operations research areas. Nevertheless, numerous studies and examples have shown that the PGA m...

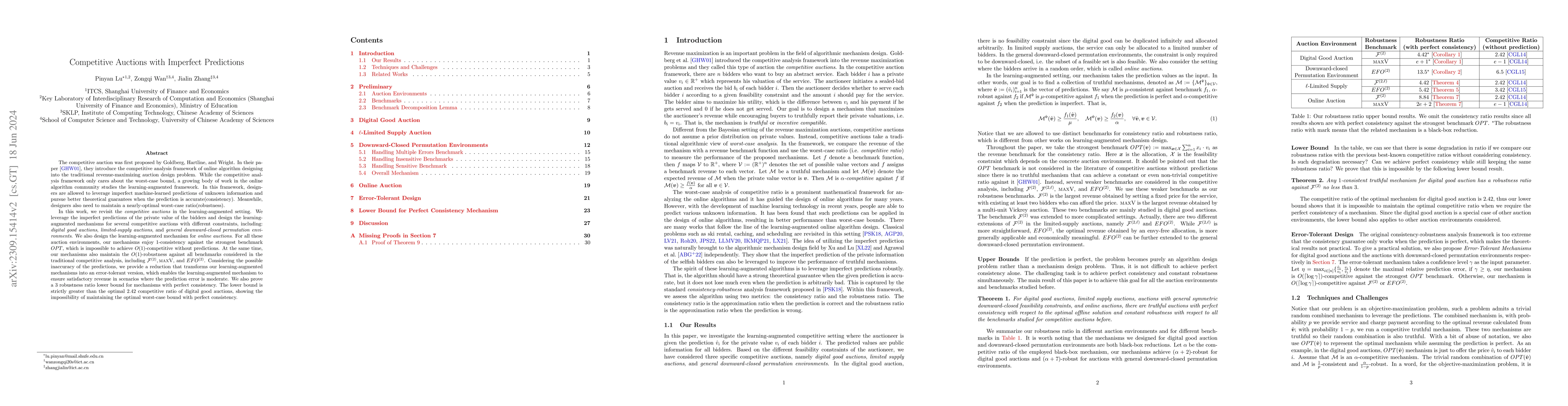

The competitive auction was first proposed by Goldberg, Hartline, and Wright. In their paper, they introduce the competitive analysis framework of online algorithm designing into the traditional rev...

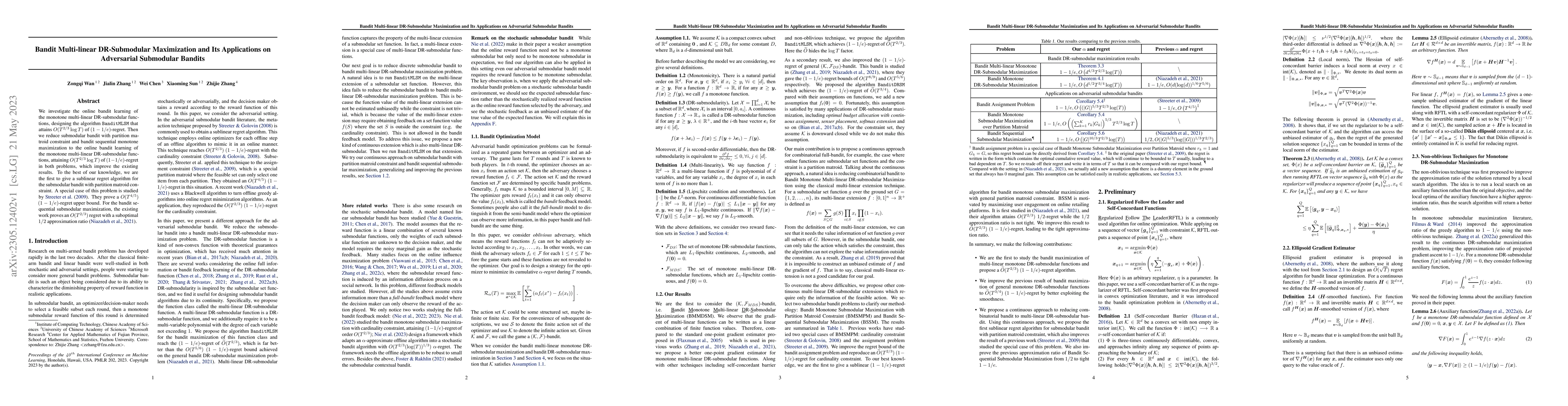

We investigate the online bandit learning of the monotone multi-linear DR-submodular functions, designing the algorithm $\mathtt{BanditMLSM}$ that attains $O(T^{2/3}\log T)$ of $(1-1/e)$-regret. The...

Multi-arm bandit (MAB) and stochastic linear bandit (SLB) are important models in reinforcement learning, and it is well-known that classical algorithms for bandits with time horizon $T$ suffer $\Om...

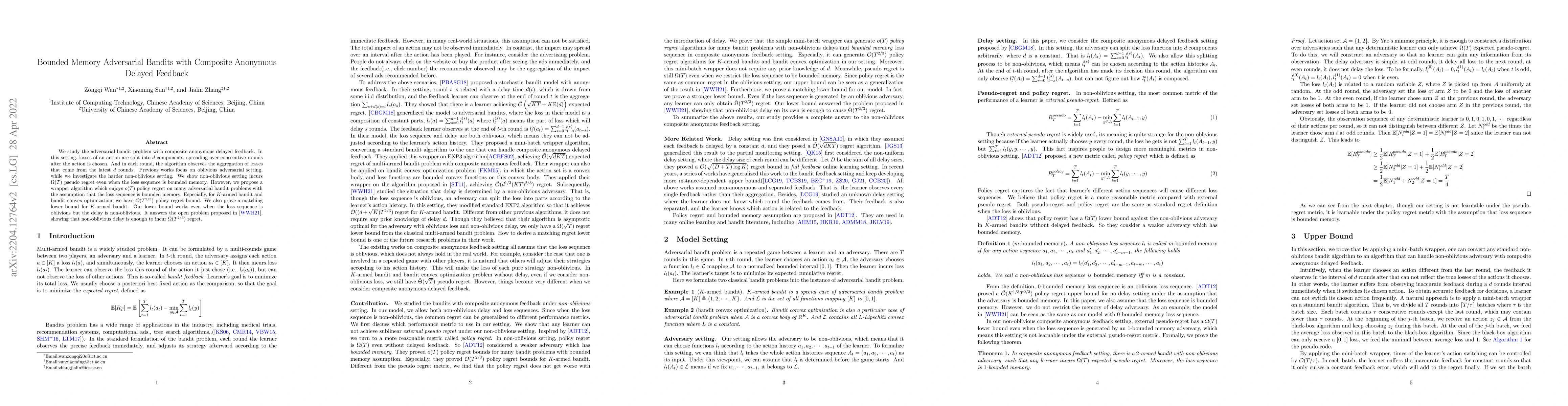

We study the adversarial bandit problem with composite anonymous delayed feedback. In this setting, losses of an action are split into $d$ components, spreading over consecutive rounds after the act...

Coordinating multiple agents to collaboratively maximize submodular functions in unpredictable environments is a critical task with numerous applications in machine learning, robot planning and contro...

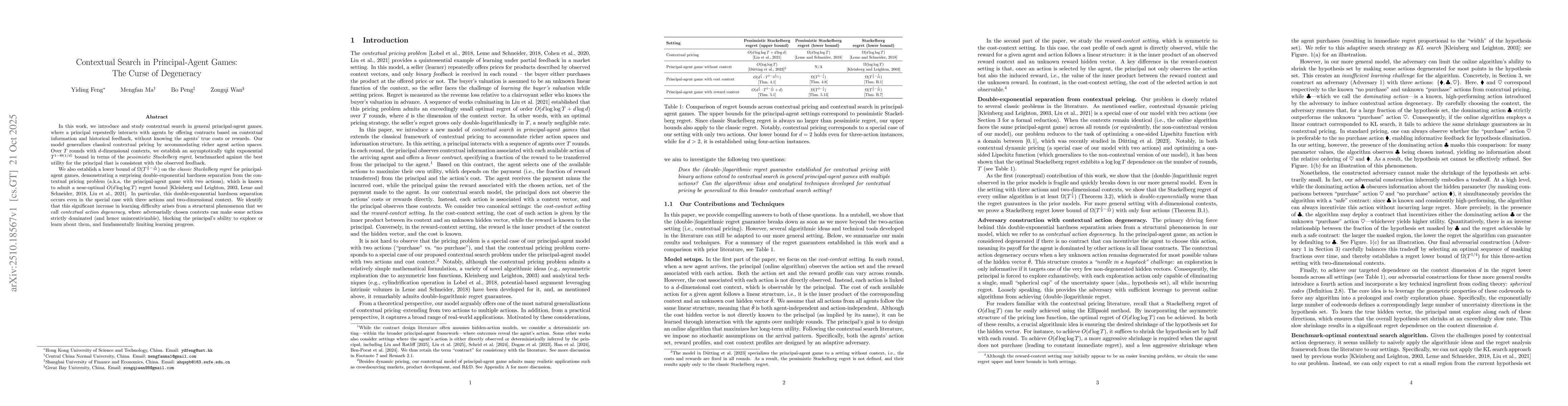

In this work, we introduce and study contextual search in general principal-agent games, where a principal repeatedly interacts with agents by offering contracts based on contextual information and hi...

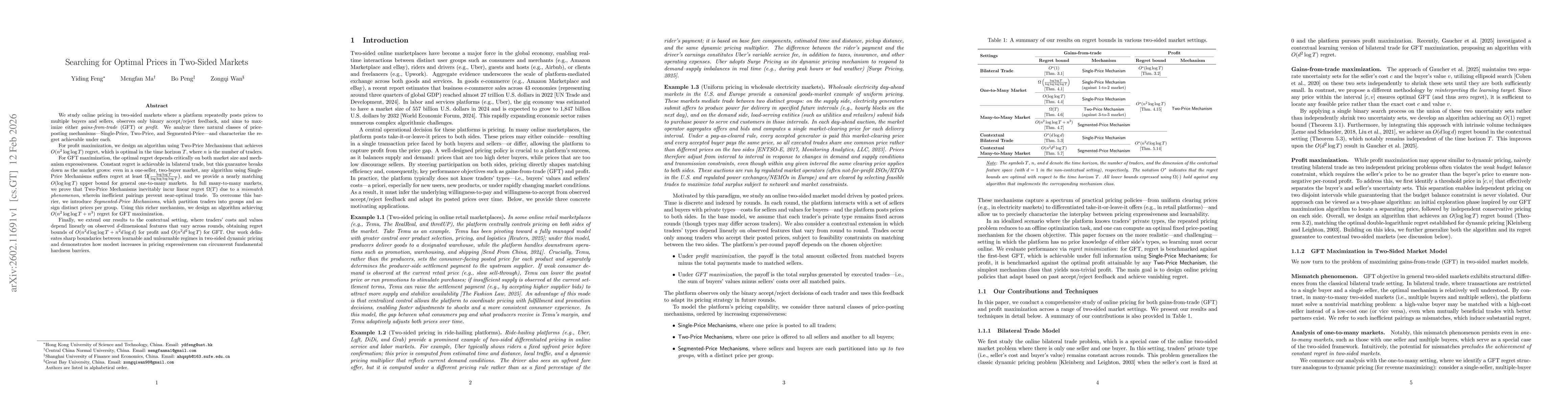

We investigate online pricing in two-sided markets where a platform repeatedly posts prices based on binary accept/reject feedback to maximize gains-from-trade (GFT) or profit. We characterize the reg...

We study stochastic zeroth-order optimization with decision-dependent distributions, where the sampling law depends on the current decision and only noisy function values are available. For the non-sm...