A bivariate Normal Inverse Gaussian process with stochastic delay: efficient simulations and applications to energy markets

Publication

Metrics

AI Quick Summary

This paper introduces a new bivariate Normal Inverse Gaussian process with stochastic delay, utilizing self-decomposable subordinators. It presents an efficient simulation method based on L\'evy-driven Ornstein-Uhlenbeck processes, improving upon existing schemes by avoiding acceptance-rejection methods, and applies these advancements to energy market modeling and spread option pricing.

Paper Preview

Abstract

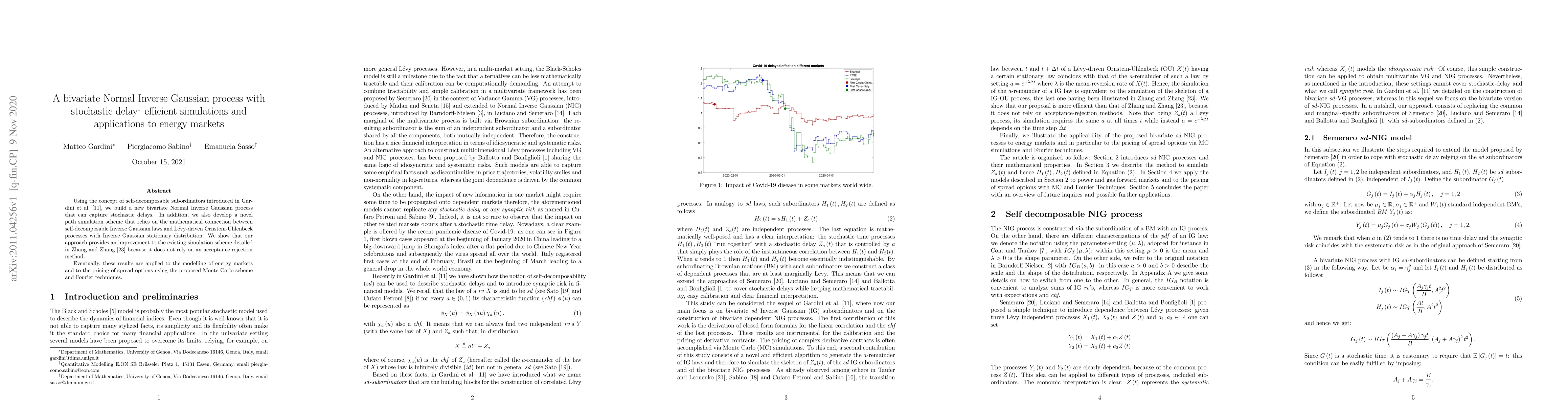

Using the concept of self-decomposable subordinators introduced in Gardini et al. [11], we build a new bivariate Normal Inverse Gaussian process that can capture stochastic delays. In addition, we also develop a novel path simulation scheme that relies on the mathematical connection between self-decomposable Inverse Gaussian laws and L\'evy-driven Ornstein-Uhlenbeck processes with Inverse Gaussian stationary distribution. We show that our approach provides an improvement to the existing simulation scheme detailed in Zhang and Zhang [23] because it does not rely on an acceptance-rejection method. Eventually, these results are applied to the modelling of energy markets and to the pricing of spread options using the proposed Monte Carlo scheme and Fourier techniques

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0