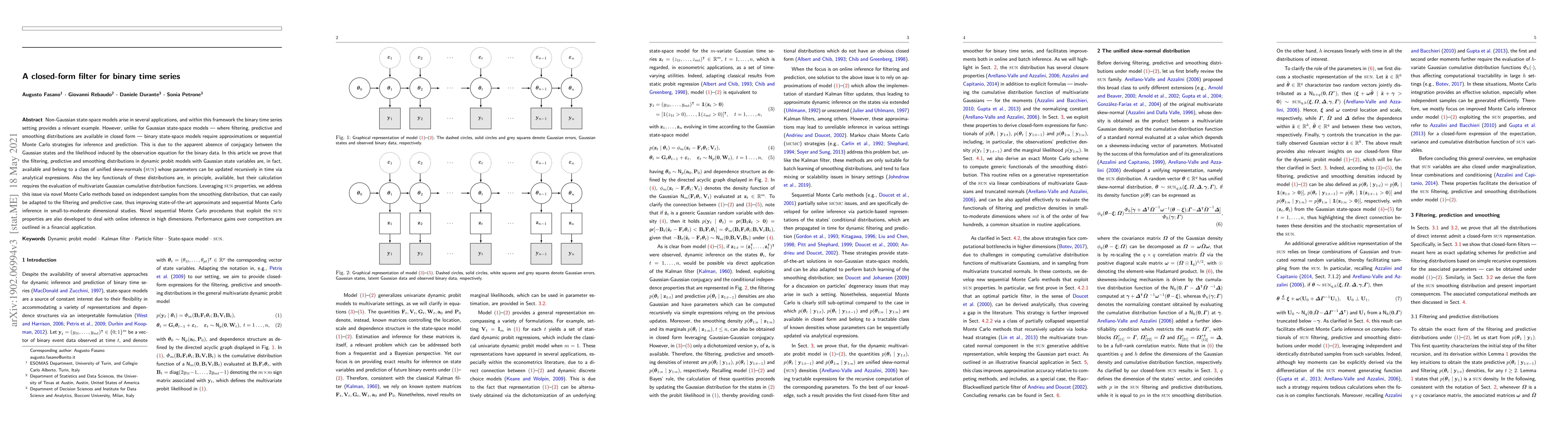

A closed-form filter for binary time series

Publication

Metrics

AI Quick Summary

This paper presents a closed-form filter for binary time series using dynamic probit models, showing that filtering, predictive, and smoothing distributions belong to a unified skew-normal class. The proposed method leverages Monte Carlo techniques to improve inference and prediction in small-to-moderate dimensional studies.

Paper Preview

Abstract

Non-Gaussian state-space models arise in several applications, and within this framework the binary time series setting provides a relevant example. However, unlike for Gaussian state-space models - where filtering, predictive and smoothing distributions are available in closed form - binary state-space models require approximations or sequential Monte Carlo strategies for inference and prediction. This is due to the apparent absence of conjugacy between the Gaussian states and the likelihood induced by the observation equation for the binary data. In this article we prove that the filtering, predictive and smoothing distributions in dynamic probit models with Gaussian state variables are, in fact, available and belong to a class of unified skew-normals (SUN) whose parameters can be updated recursively in time via analytical expressions. Also the key functionals of these distributions are, in principle, available, but their calculation requires the evaluation of multivariate Gaussian cumulative distribution functions. Leveraging SUN properties, we address this issue via novel Monte Carlo methods based on independent samples from the smoothing distribution, that can easily be adapted to the filtering and predictive case, thus improving state-of-the-art approximate and sequential Monte Carlo inference in small-to-moderate dimensional studies. Novel sequential Monte Carlo procedures that exploit the SUN properties are also developed to deal with online inference in high dimensions. Performance gains over competitors are outlined in a financial application.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0