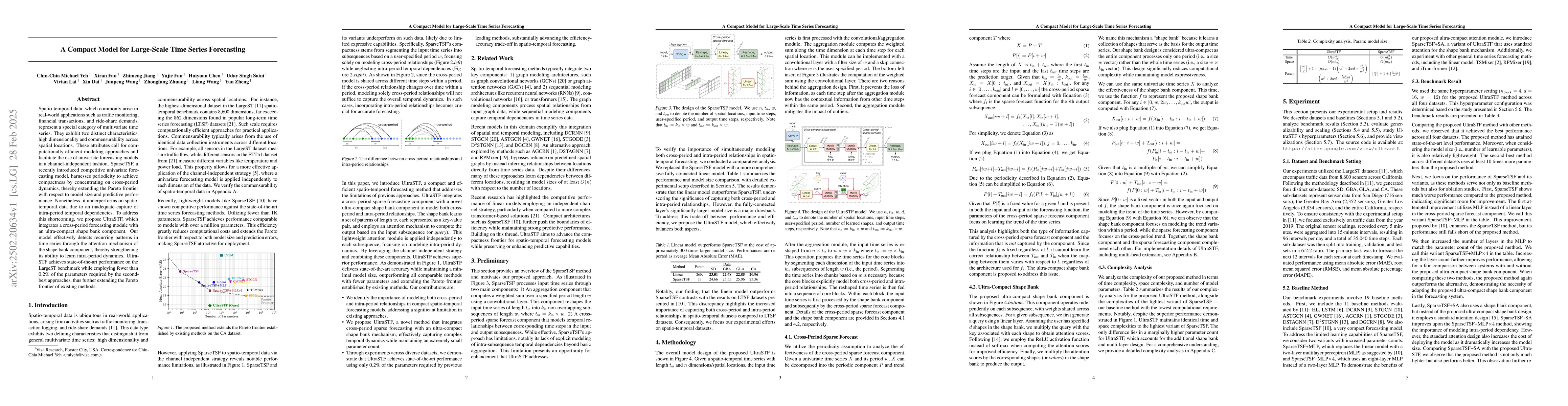

Spatio-temporal data, which commonly arise in real-world applications such as

traffic monitoring, financial transactions, and ride-share demands, represent a

special category of multivariate time series. They exhibit two distinct

characteristics: high dimensionality and commensurability across spatial

locations. These attributes call for computationally efficient modeling

approaches and facilitate the use of univariate forecasting models in a

channel-independent fashion. SparseTSF, a recently introduced competitive

univariate forecasting model, harnesses periodicity to achieve compactness by

concentrating on cross-period dynamics, thereby extending the Pareto frontier

with respect to model size and predictive performance. Nonetheless, it

underperforms on spatio-temporal data due to an inadequate capture of

intra-period temporal dependencies. To address this shortcoming, we propose

UltraSTF, which integrates a cross-period forecasting module with an

ultra-compact shape bank component. Our model effectively detects recurring

patterns in time series through the attention mechanism of the shape bank

component, thereby strengthening its ability to learn intra-period dynamics.

UltraSTF achieves state-of-the-art performance on the LargeST benchmark while

employing fewer than 0.2% of the parameters required by the second-best

approaches, thus further extending the Pareto frontier of existing methods.

Discussion 0