Publication

Metrics

AI Quick Summary

This paper proposes a computationally efficient Expectation-Maximization algorithm for estimating correlated mixed Probit models, addressing the computational burden of existing methods. The new approach significantly reduces computation time while maintaining accurate parameter estimates, demonstrated through a simulation study and an application to credit risk modeling for UK SMEs.

Paper Preview

Abstract

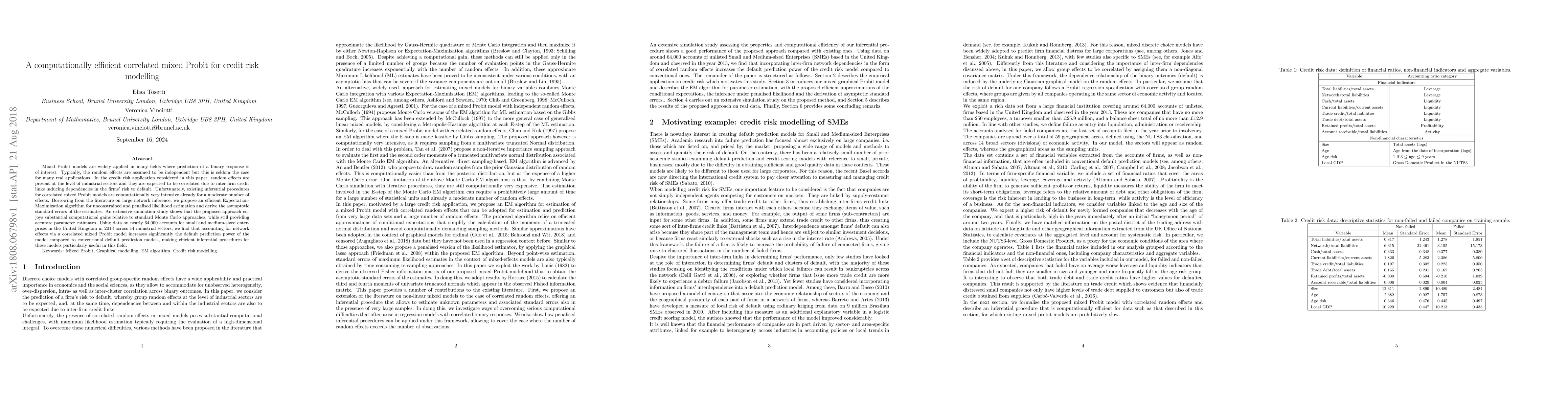

Mixed Probit models are widely applied in many fields where prediction of a binary response is of interest. Typically, the random effects are assumed to be independent but this is seldom the case for many real applications. In the credit risk application considered in this paper, random effects are present at the level of industrial sectors and they are expected to be correlated due to inter-firm credit links inducing dependencies in the firms' risk to default. Unfortunately, existing inferential procedures for correlated mixed Probit models are computationally very intensive already for a moderate number of effects. Borrowing from the literature on large network inference, we propose an efficient Expectation-Maximization algorithm for unconstrained and penalised likelihood estimation and derive the asymptotic standard errors of the estimates. An extensive simulation study shows that the proposed approach enjoys substantial computational gains relative to standard Monte Carlo approaches, while still providing accurate parameter estimates. Using data on nearly 64,000 accounts for small and medium-sized enterprises in the United Kingdom in 2013 across 14 industrial sectors, we find that accounting for network effects via a correlated mixed Probit model increases significantly the default prediction power of the model compared to conventional default prediction models, making efficient inferential procedures for these models particularly useful in this field.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0