A Decomposition-based State Space Model for Multivariate Time-Series Forecasting

Publication

Metrics

Paper Preview

Abstract

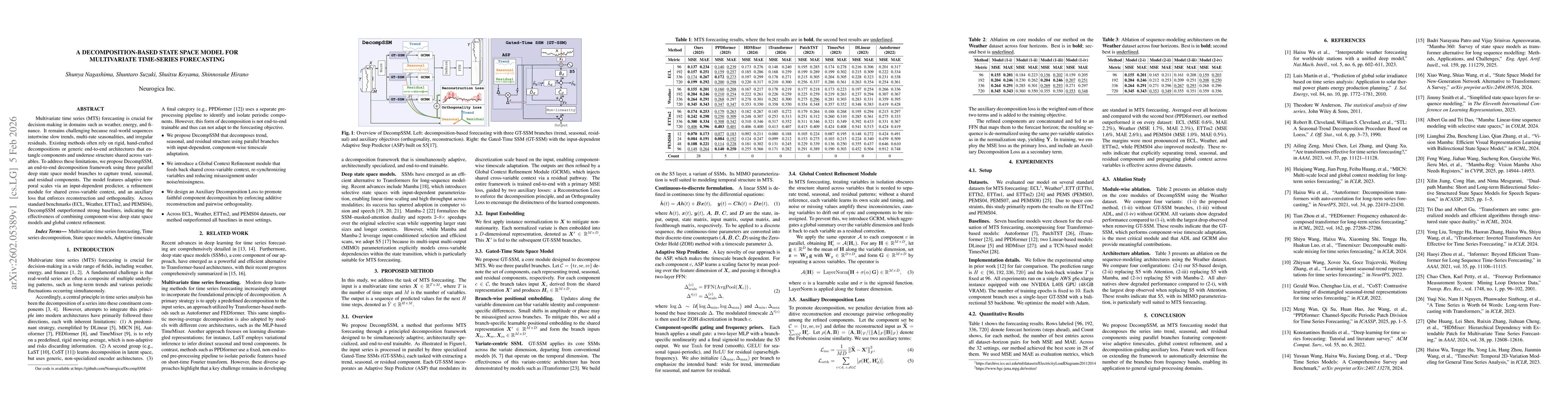

Multivariate time series (MTS) forecasting is crucial for decision-making in domains such as weather, energy, and finance. It remains challenging because real-world sequences intertwine slow trends, multi-rate seasonalities, and irregular residuals. Existing methods often rely on rigid, hand-crafted decompositions or generic end-to-end architectures that entangle components and underuse structure shared across variables. To address these limitations, we propose DecompSSM, an end-to-end decomposition framework using three parallel deep state space model branches to capture trend, seasonal, and residual components. The model features adaptive temporal scales via an input-dependent predictor, a refinement module for shared cross-variable context, and an auxiliary loss that enforces reconstruction and orthogonality. Across standard benchmarks (ECL, Weather, ETTm2, and PEMS04), DecompSSM outperformed strong baselines, indicating the effectiveness of combining component-wise deep state space models and global context refinement.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0