Publication

Metrics

Quick Actions

AI Quick Summary

This research proposes a deep reinforcement learning approach utilizing a multi-agent asynchronous distribution framework, specifically the A3C algorithm, to optimize trading strategies in the forex market. The results show that both A3C models outperform traditional Proximal Policy Optimization, with A3C with lock excelling in single currency trading and A3C without lock in multi-currency scenarios, thereby enhancing trading returns and efficiency.

Paper Preview

Abstract

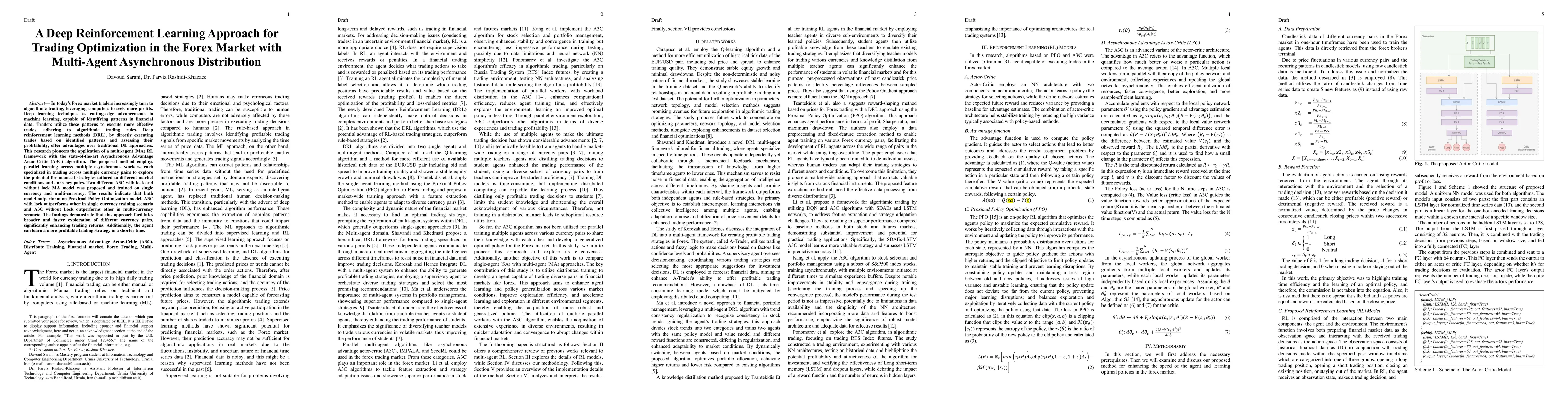

In today's forex market traders increasingly turn to algorithmic trading, leveraging computers to seek more profits. Deep learning techniques as cutting-edge advancements in machine learning, capable of identifying patterns in financial data. Traders utilize these patterns to execute more effective trades, adhering to algorithmic trading rules. Deep reinforcement learning methods (DRL), by directly executing trades based on identified patterns and assessing their profitability, offer advantages over traditional DL approaches. This research pioneers the application of a multi-agent (MA) RL framework with the state-of-the-art Asynchronous Advantage Actor-Critic (A3C) algorithm. The proposed method employs parallel learning across multiple asynchronous workers, each specialized in trading across multiple currency pairs to explore the potential for nuanced strategies tailored to different market conditions and currency pairs. Two different A3C with lock and without lock MA model was proposed and trained on single currency and multi-currency. The results indicate that both model outperform on Proximal Policy Optimization model. A3C with lock outperforms other in single currency training scenario and A3C without Lock outperforms other in multi-currency scenario. The findings demonstrate that this approach facilitates broader and faster exploration of different currency pairs, significantly enhancing trading returns. Additionally, the agent can learn a more profitable trading strategy in a shorter time.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

How to Cite This Paper

@article{sarani2024a,

title = {A Deep Reinforcement Learning Approach for Trading Optimization in the

Forex Market with Multi-Agent Asynchronous Distribution},

author = {Sarani, Davoud and Rashidi-Khazaee, Dr. Parviz},

year = {2024},

eprint = {2405.19982},

archivePrefix = {arXiv},

primaryClass = {cs.CE},

}Sarani, D., & Rashidi-Khazaee, D. (2024). A Deep Reinforcement Learning Approach for Trading Optimization in the

Forex Market with Multi-Agent Asynchronous Distribution. arXiv. https://arxiv.org/abs/2405.19982Sarani, Davoud, and Dr. Parviz Rashidi-Khazaee. "A Deep Reinforcement Learning Approach for Trading Optimization in the

Forex Market with Multi-Agent Asynchronous Distribution." arXiv, 2024, arxiv.org/abs/2405.19982.PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersOnline Trading Models with Deep Reinforcement Learning in the Forex Market Considering Transaction Costs

Koya Ishikawa, Kazuhide Nakata

Improving Deep Reinforcement Learning Agent Trading Performance in Forex using Auxiliary Task

Sahar Arabha, Davoud Sarani, Parviz Rashidi-Khazaee

Deep Reinforcement Learning Approach for Trading Automation in The Stock Market

Taylan Kabbani, Ekrem Duman

Multi-Agent Deep Reinforcement Learning for Zonal Ancillary Market Coupling

Francesco Morri, Hélène Le Cadre, Pierre Gruet et al.

No citations found for this paper.

Comments (0)