A dual approach to nonparametric characterization for random utility models

Publication

Metrics

AI Quick Summary

This paper introduces a dual nonparametric characterization for random utility models (RUM) using matrix $\Xi$ to represent revealed preference relations. It shows that consistency with RUMs is determined by $\Xi\pi \geq \mathbb{1}$, and provides insights into cyclical choices and maximal weights on rational patterns.

Paper Preview

Abstract

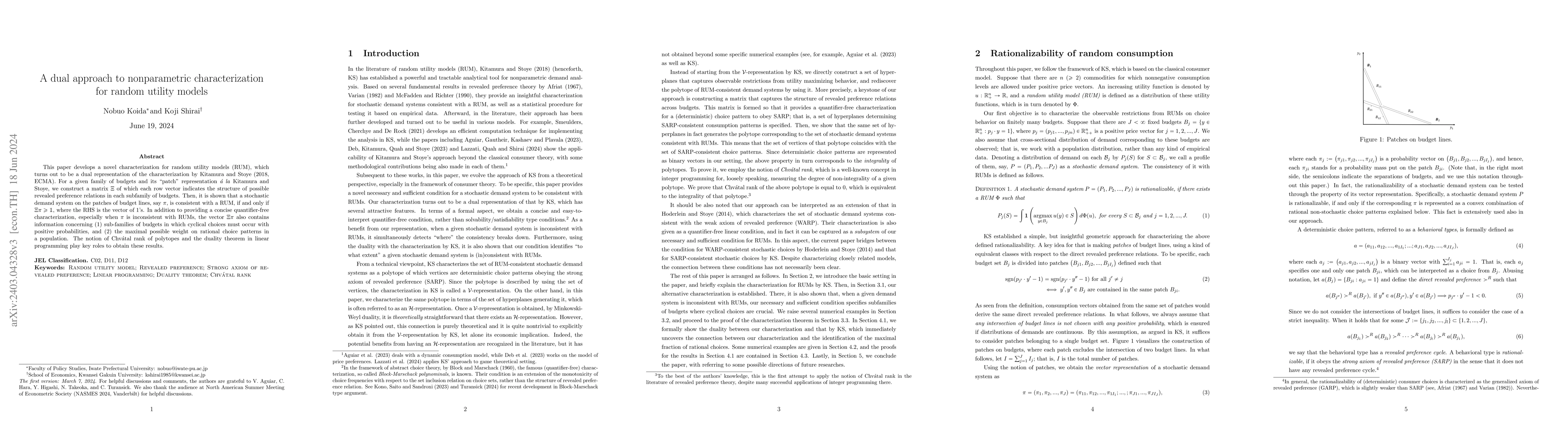

This paper develops a novel characterization for random utility models (RUM), which turns out to be a dual representation of the characterization by Kitamura and Stoye (2018, ECMA). For a given family of budgets and its "patch" representation \'a la Kitamura and Stoye, we construct a matrix $\Xi$ of which each row vector indicates the structure of possible revealed preference relations in each subfamily of budgets. Then, it is shown that a stochastic demand system on the patches of budget lines, say $\pi$, is consistent with a RUM, if and only if $\Xi\pi \geq \mathbb{1}$, where the RHS is the vector of $1$'s. In addition to providing a concise quantifier-free characterization, especially when $\pi$ is inconsistent with RUMs, the vector $\Xi\pi$ also contains information concerning (1) sub-families of budgets in which cyclical choices must occur with positive probabilities, and (2) the maximal possible weights on rational choice patterns in a population. The notion of Chv\'atal rank of polytopes and the duality theorem in linear programming play key roles to obtain these results.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0