A General Stochastic Optimization Framework for Convergence Bidding

Publication

Metrics

AI Quick Summary

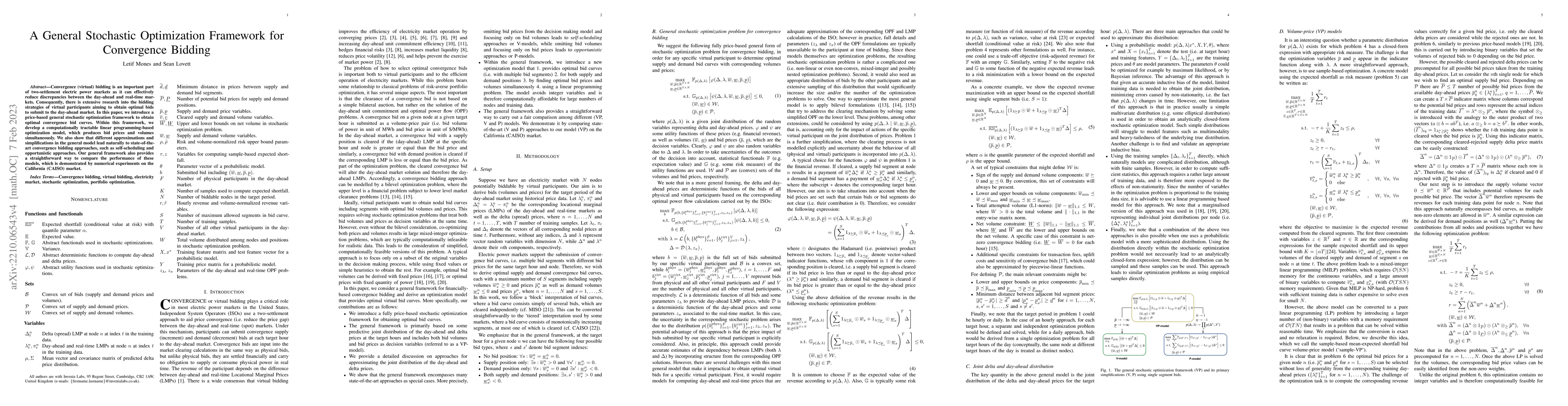

This paper presents a general stochastic optimization framework for convergence bidding in electric power markets, introducing a linear programming model to derive optimal bid curves. The framework allows for comparison of various bidding strategies and is demonstrated through numerical experiments on the California Independent System Operator (CAISO) market.

Paper Preview

Abstract

Convergence (virtual) bidding is an important part of two-settlement electric power markets as it can effectively reduce discrepancies between the day-ahead and real-time markets. Consequently, there is extensive research into the bidding strategies of virtual participants aiming to obtain optimal bids to submit to the day-ahead market. In this paper, we introduce a price-based general stochastic optimization framework to obtain optimal convergence bid curves. Within this framework, we develop a computationally tractable linear programming-based optimization model, which produces bid prices and volumes simultaneously. We also show that different approximations and simplifications in the general model lead naturally to state-of-the-art convergence bidding approaches, such as self-scheduling and opportunistic approaches. Our general framework also provides a straightforward way to compare the performance of these models, which is demonstrated by numerical experiments on the California (CAISO) market.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0