A Mathematical Analysis of Benford's Law and its Generalization

Publication

Metrics

AI Quick Summary

This paper presents Kossovsky's generalization of Benford's Law, applying it to various natural data sequences and showing that the models based on normal and reflected Gumbel densities are generally more compliant than the actual data. The findings suggest potential improvements in density estimation for statistical pattern recognition and machine learning.

Paper Preview

Abstract

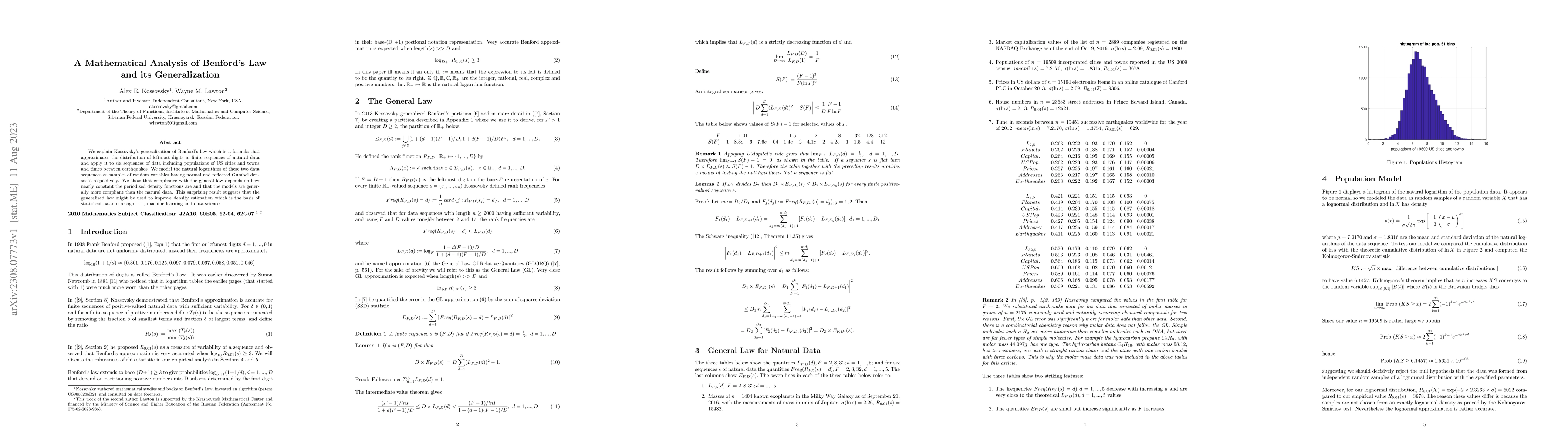

We explain Kossovsky's generalization of Benford's law which is a formula that approximates the distribution of leftmost digits in finite sequences of natural data and apply it to six sequences of data including populations of US cities and towns and times between earthquakes. We model the natural logarithms of these two data sequences as samples of random variables having normal and reflected Gumbel densities respectively. We show that compliance with the general law depends on how nearly constant the periodized density functions are and that the models are generally more compliant than the natural data. This surprising result suggests that the generalized law might be used to improve density estimation which is the basis of statistical pattern recognition, machine learning and data science.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0