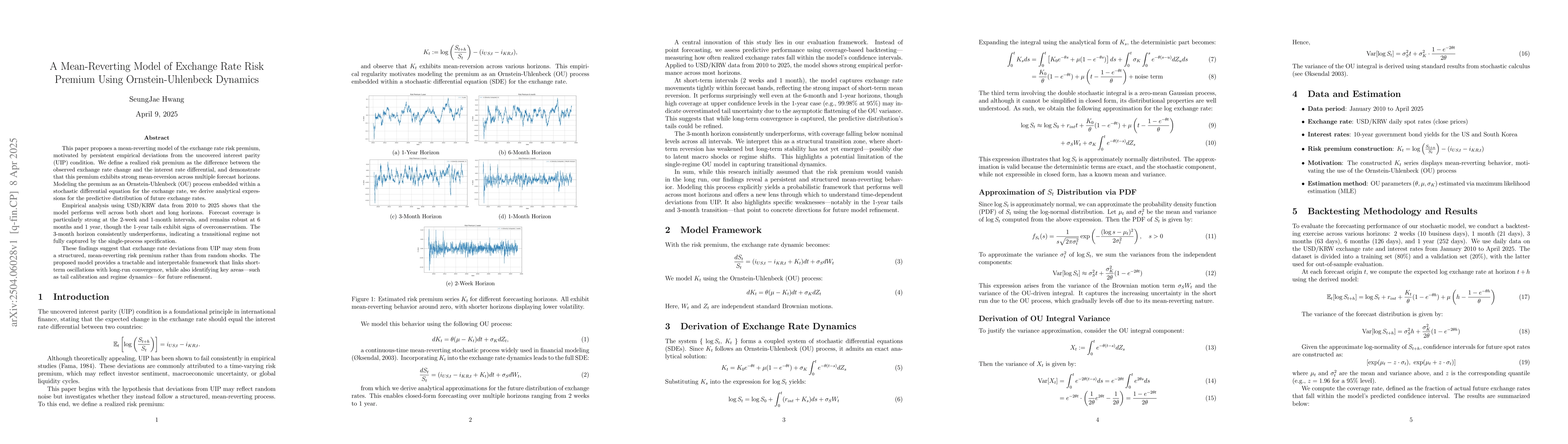

This paper examines the empirical failure of uncovered interest parity (UIP)

and proposes a structural explanation based on a mean-reverting risk premium.

We define a realized premium as the deviation between observed exchange rate

returns and the interest rate differential, and demonstrate its strong

mean-reverting behavior across multiple horizons. Motivated by this pattern, we

model the risk premium using an Ornstein-Uhlenbeck (OU) process embedded within

a stochastic differential equation for the exchange rate.

Our model yields closed-form approximations for future exchange rate

distributions, which we evaluate using coverage-based backtesting. Applied to

USD/KRW data from 2010 to 2025, the model shows strong predictive performance

at both short-term and long-term horizons, while underperforming at

intermediate (3-month) horizons and showing conservative behavior in the tails

of long-term forecasts. These results suggest that exchange rate deviations

from UIP may reflect structured, forecastable dynamics rather than pure noise,

and point to future modeling improvements via regime-switching or time-varying

volatility.

Discussion 0