Background

The paper situates flexibility as a core virtue in decision making, tracing robust and adaptive strands of thought from Stigler to more modern influence-diagram and decision-tree frameworks. The central challenge is that real-world uncertainty is rarely fully capturable by a model; unmodeled or unforeseen factors can degrade plan performance. The author argues for a simple, decision-analytic method that remains broadly compatible with existing models while explicitly accounting for the uncertainty that the model misses. A key insight is to manipulate the distribution of the value attribute directly, rather than trying to exhaustively enrich the model itself, to reflect missing uncertainty.

A foundational concept is the monetary equivalence for prospects and the delta property. When a decision-maker’s utility for money exhibits constant absolute risk aversion, the delta property holds, and the willingness-to-pay for a prospect can be expressed linearly through the certain equivalence. This provides a tractable bridge from qualitative notions of flexibility to quantitative comparisons across different decision situations.

Problem / Research Question

The core question is how to define and compute a notion of flexibility that is both general enough to apply to diverse decision models (trees, influence diagrams) and computationally tractable for practical use. The aim is to compare two uncertain monetary prospects by asking how their relative flexibility evolves as uncertainty is magnified. The problem is made sharper by unavoidable unmodeled uncertainty and by the desire to use a single, consistent metric that guides both evaluation and the search for more flexible alternatives.

Innovation / Contribution

The breakthrough is a simple, normative framework that ties flexibility to the certain equivalence (CE) of transformed prospects. By introducing a parameter k to magnify uncertainty (and by adding an independent uncertainty Z via the transformation X → kX + Z), the author defines a dominance relation: one prospect X is more flexible than another Y if, for all k ≥ 1, the CE of kX + Z exceeds that of kY + Z. Under the delta property with constant absolute risk aversion r > 0, this yields a clean, analyzable rule for comparing plans across a continuum of magnified uncertainty. The framework unites robust and adaptive notions and remains applicable to general decision models, not just specialized cases.

A practical simplification occurs in the Gaussian case: when X is Gaussian, the CE becomes a linear function of k, making the comparison even more transparent. The results also cover dominance and non-dominance in flexibility, and they explain when waiting or choosing now (in sequential structures) can dominate other alternatives in flexibility.

Methodology / Approach

The method rests on a monetary-equivalent, risk-averse decision-maker satisfying the delta property. The key objects are uncertain monetary prospects X and Y, and an independent perturbation Z that captures unmodeled uncertainty. The comparison uses transformed prospects kX + Z and kY + Z for increasing k, leveraging Theorem 1 (Delta Property) and Theorem 2 (Certain Equivalence) to relate risk preferences to CE calculations. The corollaries show how linear transformations preserve or alter ordering when r > 0, enabling straightforward comparisons even as uncertainty is scaled.

The core definition—X is (strictly) more flexible than Y if there exists some positive K such that CE(kX + Z | r) > CE(kY + Z | r) for all k ≥ K—provides a robust, intuitive criterion. The author discusses graphical illustrations (Figures 5–7) and demonstrates that, in stochastic environments with Gaussian X, the CE is linear in k, so one can detect dominance with relatively simple analyses. The approach is also shown to accommodate complex decision structures, including adaptive and robust plans, and to yield insights for generating new, more flexible alternatives.

Experiments / Evaluation

The work is primarily theoretical and analytical, offering rigorous theorems, corollaries, and illustrative scenarios rather than empirical experiments. It recasts classic examples (Stigler’s robust configurations, adaptive influence diagrams, and sequential decision trees) within the proposed CE-based flexibility framework, showing how CEs behave as k grows and how dominance relationships emerge. The Gaussian specialization provides a concrete, tractable evaluation path and serves as a validation of the tractability claim for common distributions.

Key Results

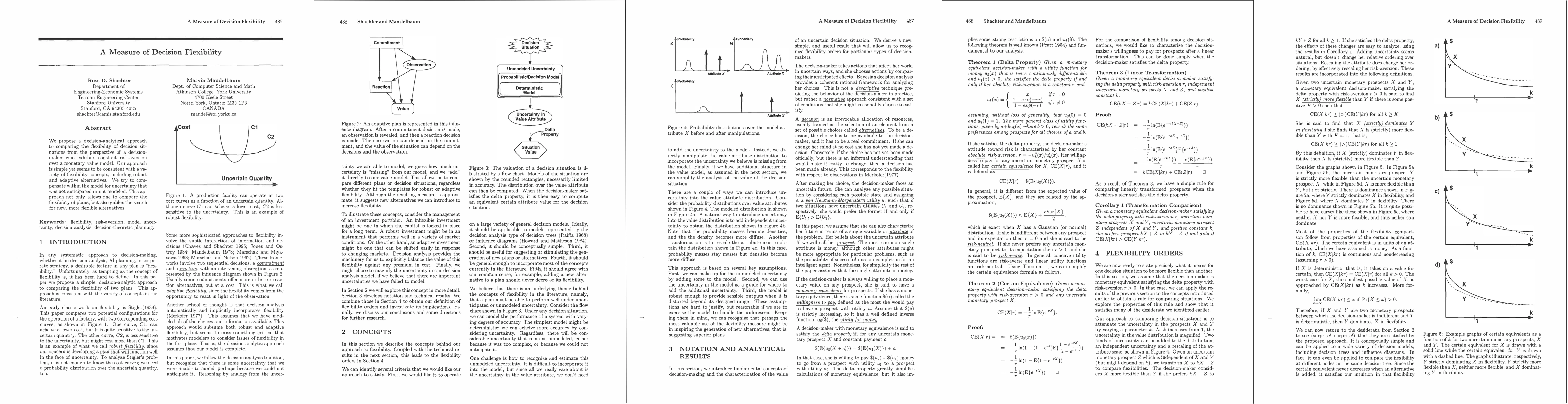

The Delta Property (Theorem 1) characterizes risk aversion and shows when monetary equivalence functions are well-behaved under price shifts. The Certain Equivalence (Theorem 2) links the CE to the underlying risk-aversion and the distribution of X, enabling practical calculations. The Linear Transformation result (Theorem 3) and its corollary (Corollary 1) establish how linear scaling and the addition of independent uncertainty Z affect preferences over X and Y, allowing direct comparisons of transformed prospects. The central Flexibility Order definition then shows that increasing k magnifies unmodeled uncertainty in a controlled way, enabling a rigorous notion of dominance: if X dominates Y in flexibility, it remains preferable as uncertainty is scaled, under the delta-property assumptions. The Gaussian case further simplifies CE(X|kr) to a linear function of k, making dominance checks particularly straightforward in that setting.

Practical Applications

This framework provides practitioners with a general, decision-analytic tool for evaluating and ranking plans by their resilience to unanticipated uncertainty. It can guide the search for new, more flexible alternatives and assist in automated reasoning tasks where model complexity must be balanced against tractable analysis. The method is designed to work with common decision representations (decision trees and influence diagrams) and to offer a way to quantify the value of additional flexibility when considering new options or delaying commitments.

Limitations & Considerations

The analysis relies on the delta-property assumption and constant absolute risk aversion (r > 0). Real decision-makers may exhibit different risk preferences (e.g., CRRA with variable risk aversion) or nonmonotone utility structures, which could alter the results. The key modeler’s step—adding unmodeled uncertainty via Z and assuming independence from X—may be questionable in some domains, and the approach remains approximate when the model is stretched beyond its designed range. The Gaussian simplification is helpful but limits applicability to non-Gaussian outcomes. Finally, practical estimation of Z, correlation structures, and the sensitivity of results to the choice of k and Z require empirical validation and methodological elaboration.

Discussion 0