A Model of Synchronization for Self-Organized Crowding Behavior

Publication

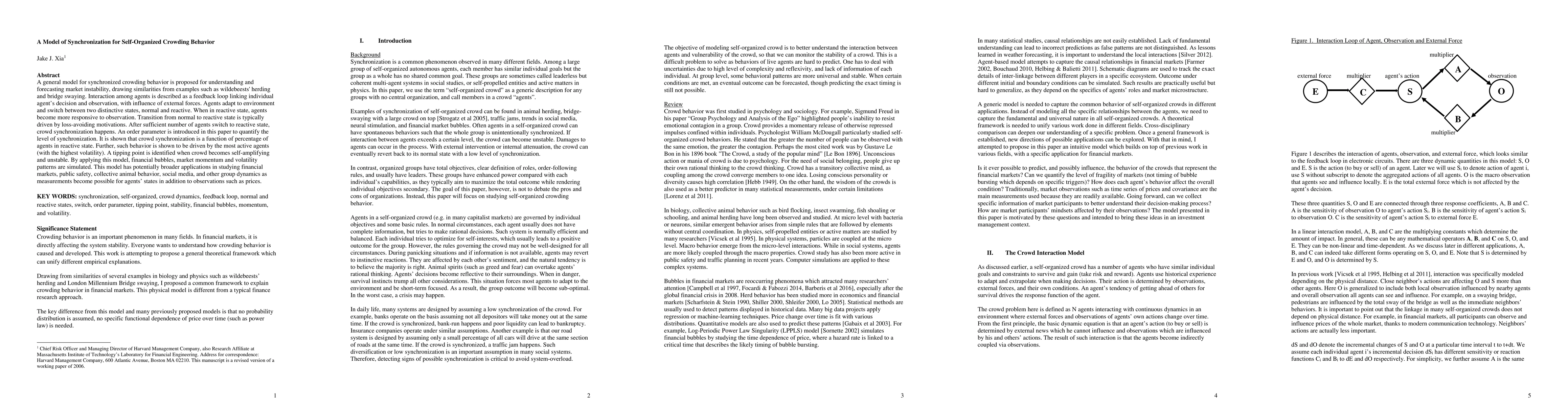

Metrics

Paper Preview

Abstract

This paper proposes a general model for synchronized crowding behavior. An order parameter is introduced to quantify the level of synchronization which is shown a function of percentage of agents in reactive state. Further, synchronization is shown to be driven by the most active agents with the highest volatility. A tipping point is identified when crowd becomes self-amplifying and unstable. By applying this model, financial bubbles, market momentum and volatility patterns are simulated.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0