01

MethodologyHow they did it

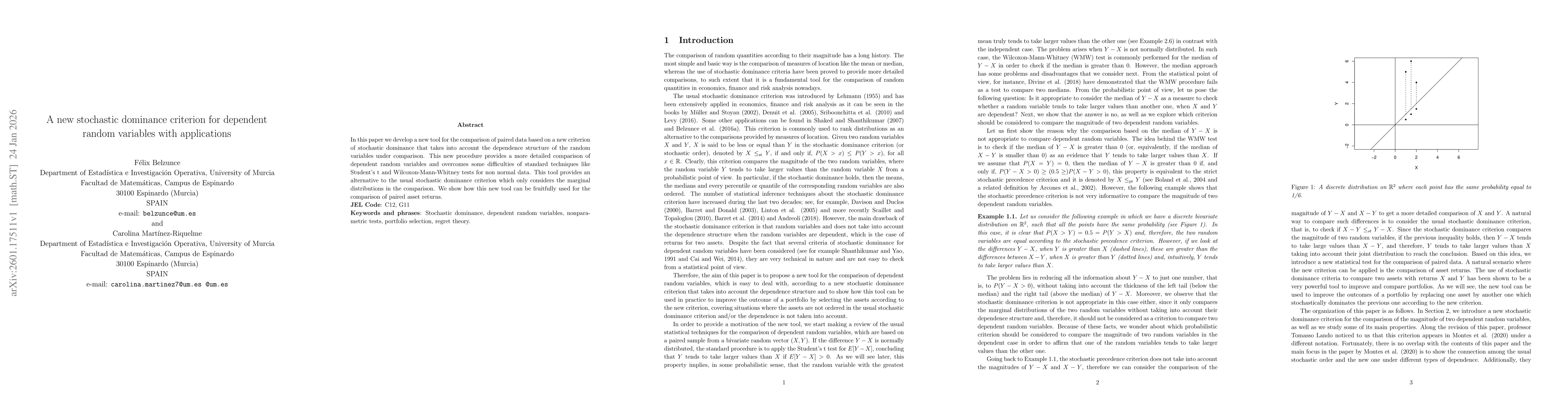

The research introduces a new stochastic dominance criterion that accounts for the dependence structure between random variables, using probabilistic and inferential methods to compare paired data. It employs nonparametric tests and copula-based models to analyze relationships.

Discussion 0