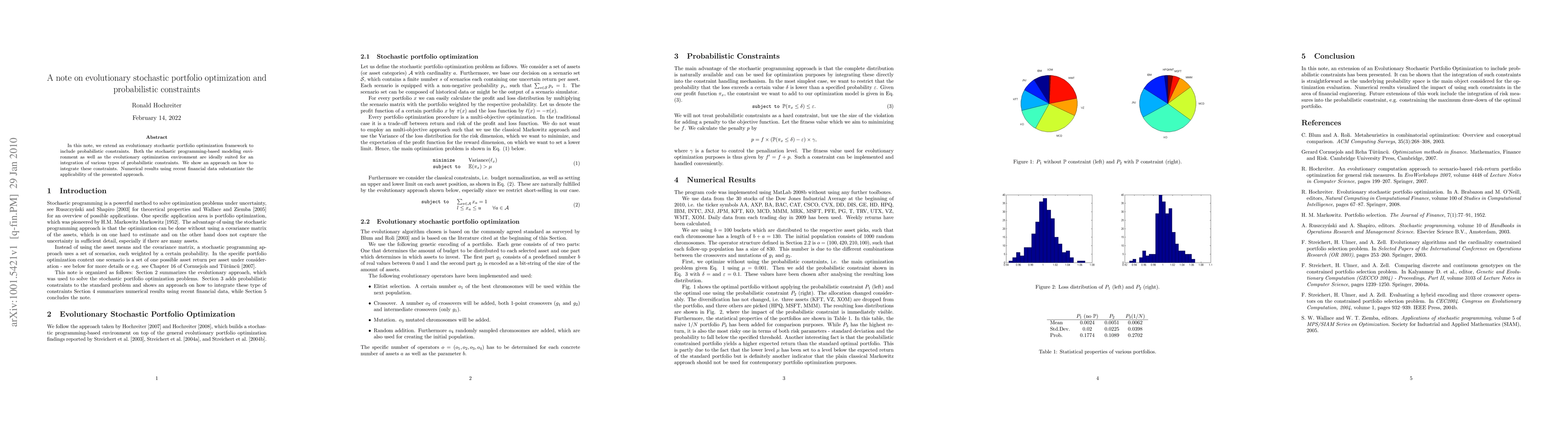

A note on evolutionary stochastic portfolio optimization and probabilistic constraints

Publication

Metrics

AI Quick Summary

This paper extends an evolutionary stochastic portfolio optimization framework to incorporate probabilistic constraints, demonstrating a method for integrating these constraints within a stochastic programming environment. Numerical results using recent financial data validate the effectiveness of the proposed approach.

Paper Preview

Abstract

In this note, we extend an evolutionary stochastic portfolio optimization framework to include probabilistic constraints. Both the stochastic programming-based modeling environment as well as the evolutionary optimization environment are ideally suited for an integration of various types of probabilistic constraints. We show an approach on how to integrate these constraints. Numerical results using recent financial data substantiate the applicability of the presented approach.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0