A Relaxed Control Problem With $L^\infty$ Cost and Jump Dynamics Motivated by Cyber Risks Insurance

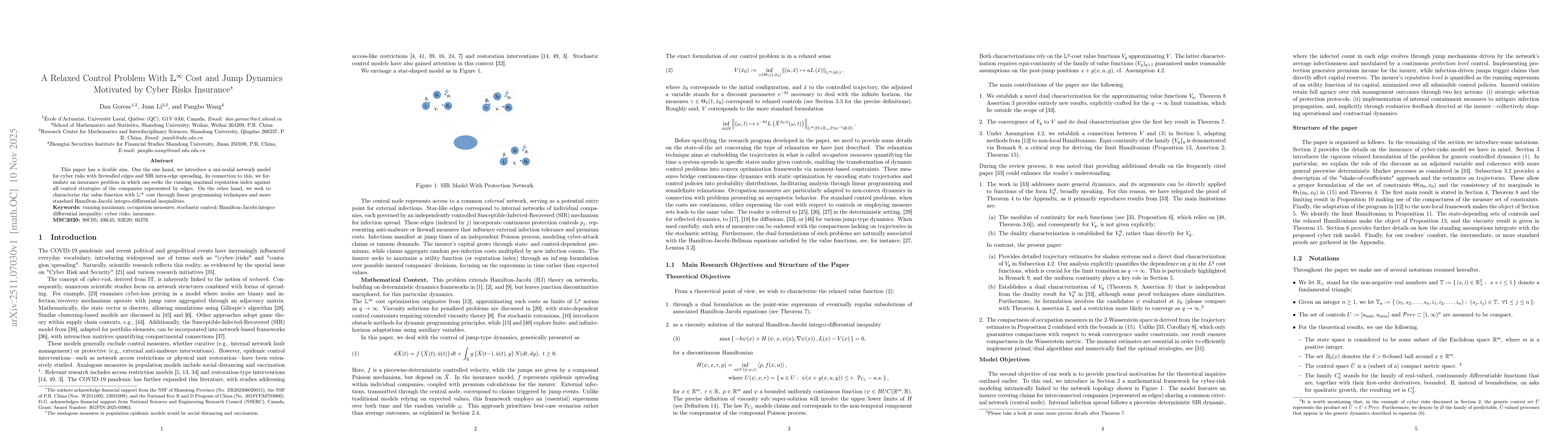

2511.07030

Published Nov 10, 2025

Publication

Published:

Nov 10, 2025

Categories:

math.OC

Metrics

Source:

ArXiv

Paper Preview

Abstract

This paper has a double aim. One the one hand, we introduce a uni-nodal network model for cyber risks with firewalled edges and SIR intra-edge spreading. In connection to this, we formulate an insurance problem in which one seeks the running maximal reputation index against all control strategies of the companies represented by edges. On the other hand, we seek to characterize the value function with $L^\infty$ cost through linear programming techniques and more standard Hamilton-Jacobi integro-differential inequalities.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0