A Tale of Two Cities: Pessimism and Opportunism in Offline Dynamic Pricing

Publication

Metrics

AI Quick Summary

This paper proposes a novel partial identification framework for offline dynamic pricing without data coverage, addressing scenarios where optimal prices may not be observed. It introduces pessimistic and opportunistic strategies within this framework and demonstrates superior performance through synthetic tests, offering valuable insights for sustainable pricing strategy in challenging settings.

Paper Preview

Abstract

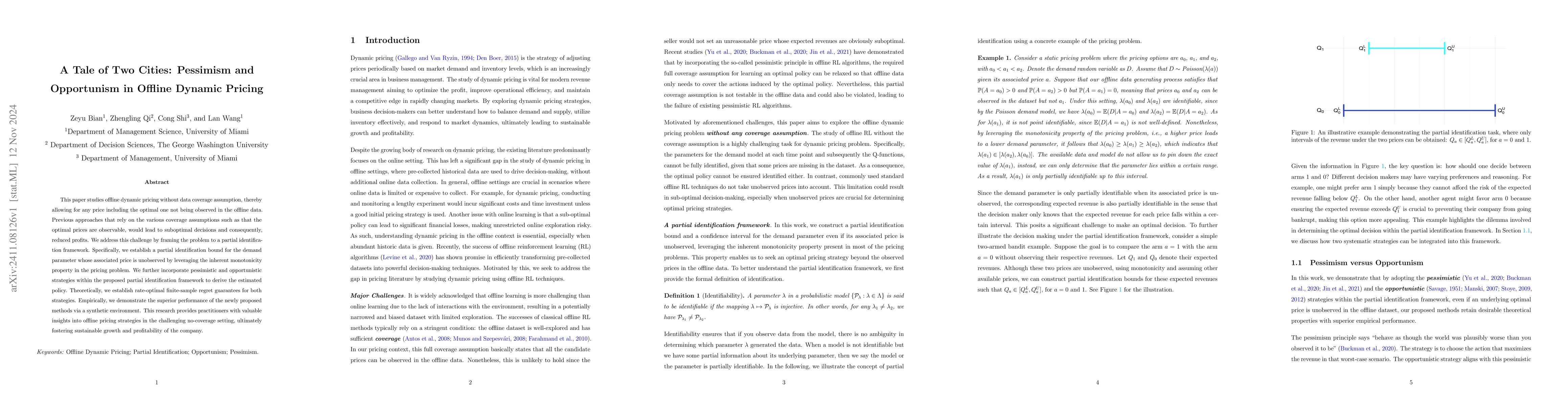

This paper studies offline dynamic pricing without data coverage assumption, thereby allowing for any price including the optimal one not being observed in the offline data. Previous approaches that rely on the various coverage assumptions such as that the optimal prices are observable, would lead to suboptimal decisions and consequently, reduced profits. We address this challenge by framing the problem to a partial identification framework. Specifically, we establish a partial identification bound for the demand parameter whose associated price is unobserved by leveraging the inherent monotonicity property in the pricing problem. We further incorporate pessimistic and opportunistic strategies within the proposed partial identification framework to derive the estimated policy. Theoretically, we establish rate-optimal finite-sample regret guarantees for both strategies. Empirically, we demonstrate the superior performance of the newly proposed methods via a synthetic environment. This research provides practitioners with valuable insights into offline pricing strategies in the challenging no-coverage setting, ultimately fostering sustainable growth and profitability of the company.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0