A "Toy" Model for Operational Risk Quantification using Credibility Theory

Publication

Metrics

AI Quick Summary

This paper proposes a credibility theory approach for quantifying operational risk under the Basel II framework, focusing on combining internal data, expert opinions, and external industry data to estimate the frequency and severity of high-impact losses exceeding a specified threshold. The method aims to address the challenge of integrating diverse data sources for operational risk management.

Paper Preview

Abstract

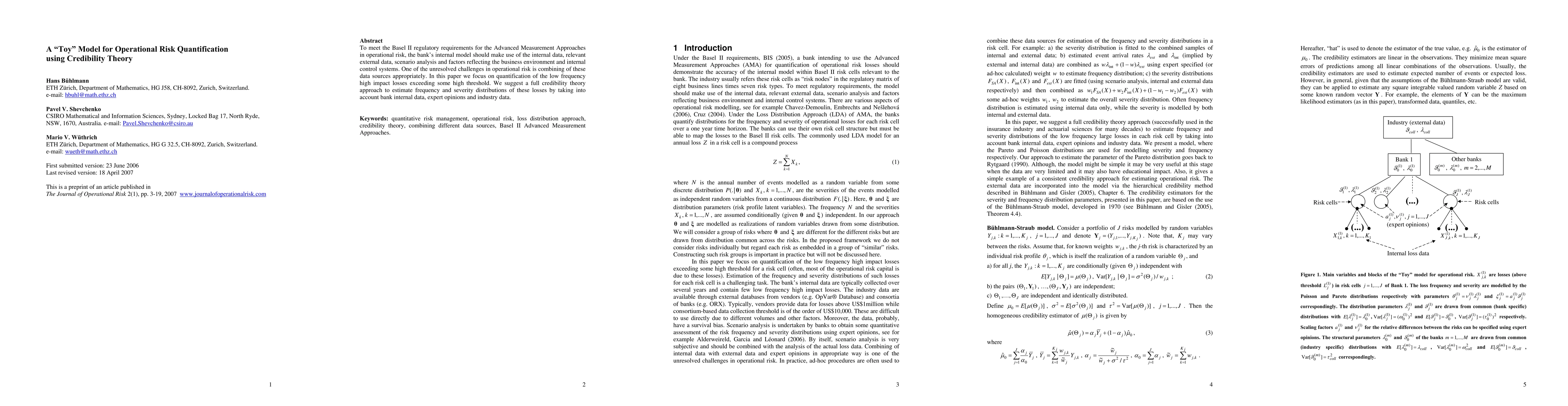

To meet the Basel II regulatory requirements for the Advanced Measurement Approaches in operational risk, the bank's internal model should make use of the internal data, relevant external data, scenario analysis and factors reflecting the business environment and internal control systems. One of the unresolved challenges in operational risk is combining of these data sources appropriately. In this paper we focus on quantification of the low frequency high impact losses exceeding some high threshold. We suggest a full credibility theory approach to estimate frequency and severity distributions of these losses by taking into account bank internal data, expert opinions and industry data.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0