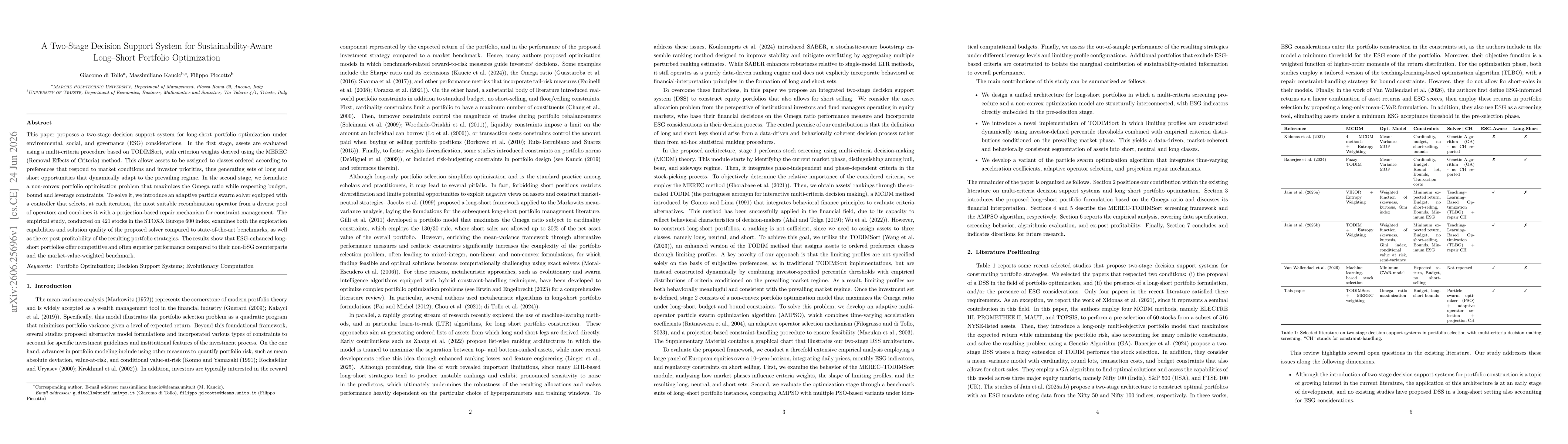

This paper proposes a two-stage decision support system for long-short portfolio optimization under environmental, social, and governance (ESG) considerations. In the first stage, assets are evaluated using a multi-criteria procedure based on TODIMSort, with criterion weights derived using the MEREC (Removal Effects of Criteria) method. This allows assets to be assigned to classes ordered according to preferences that respond to market conditions and investor priorities, thus generating sets of long and short opportunities that dynamically adapt to the prevailing regime. In the second stage, we formulate a non-convex portfolio optimization problem that maximizes the Omega ratio while respecting budget, bound and leverage constraints. To solve it, we introduce an adaptive particle swarm solver equipped with a controller that selects, at each iteration, the most suitable recombination operator from a diverse pool of operators and combines it with a projection-based repair mechanism for constraint management. The empirical study, conducted on 421 stocks in the STOXX Europe 600 index, examines both the exploration capabilities and solution quality of the proposed solver compared to state-of-the-art benchmarks, as well as the ex post profitability of the resulting portfolio strategies. The results show that ESG-enhanced long-short portfolios offer competitive and often superior performance compared to their non-ESG counterparts and the market-value-weighted benchmark.

Discussion 0