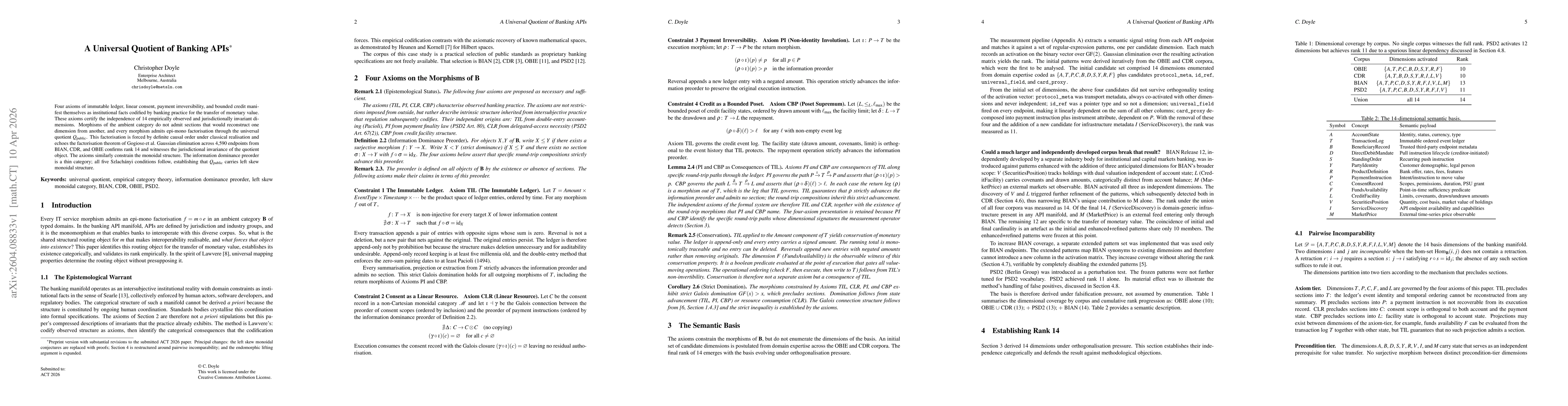

Four axioms of immutable ledger, linear consent, payment irreversibility, and bounded credit manifest themselves as institutional facts codified by banking practice for the transfer of monetary value. These axioms certify the independence of 14 empirically observed and jurisdictionally invariant dimensions. Morphisms of the ambient category do not admit sections that would reconstruct one dimension from another, and every morphism admits epi-mono factorisation through the universal quotient Q_public. This factorisation is forced by definite causal order under classical realisation and echoes the factorisation theorem of Gogioso et al. Gaussian elimination across 4,590 endpoints from BIAN, CDR, and OBIE confirms rank 14 and witnesses the jurisdictional invariance of the quotient object. The axioms similarly constrain the monoidal structure. The information dominance preorder is a thin category; all five Szlachanyi conditions follow, establishing that Q_public carries left skew monoidal structure.

Discussion 0