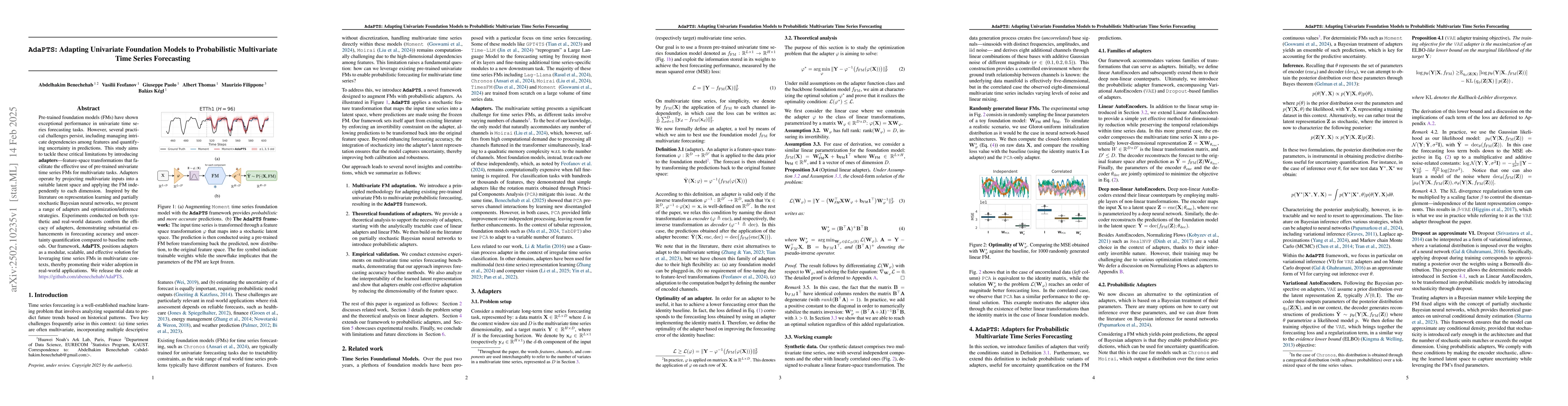

Pre-trained foundation models (FMs) have shown exceptional performance in

univariate time series forecasting tasks. However, several practical challenges

persist, including managing intricate dependencies among features and

quantifying uncertainty in predictions. This study aims to tackle these

critical limitations by introducing adapters; feature-space transformations

that facilitate the effective use of pre-trained univariate time series FMs for

multivariate tasks. Adapters operate by projecting multivariate inputs into a

suitable latent space and applying the FM independently to each dimension.

Inspired by the literature on representation learning and partially stochastic

Bayesian neural networks, we present a range of adapters and

optimization/inference strategies. Experiments conducted on both synthetic and

real-world datasets confirm the efficacy of adapters, demonstrating substantial

enhancements in forecasting accuracy and uncertainty quantification compared to

baseline methods. Our framework, AdaPTS, positions adapters as a modular,

scalable, and effective solution for leveraging time series FMs in multivariate

contexts, thereby promoting their wider adoption in real-world applications. We

release the code at https://github.com/abenechehab/AdaPTS.

Discussion 0