Publication

Metrics

AI Quick Summary

This paper explores adversarial machine learning attacks on deep learning models used in algorithmic trading, introducing new attack strategies tailored to minimize costs while evaluating the robustness of financial models. The study also investigates the feasibility of realistic adversarial attacks that could deceive automated trading systems.

Paper Preview

Abstract

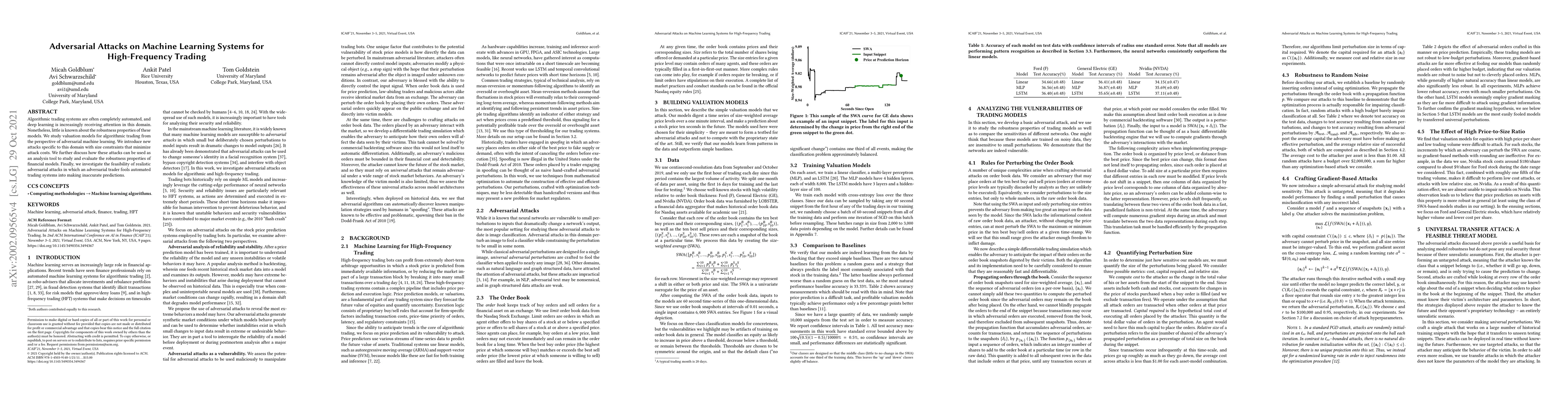

Algorithmic trading systems are often completely automated, and deep learning is increasingly receiving attention in this domain. Nonetheless, little is known about the robustness properties of these models. We study valuation models for algorithmic trading from the perspective of adversarial machine learning. We introduce new attacks specific to this domain with size constraints that minimize attack costs. We further discuss how these attacks can be used as an analysis tool to study and evaluate the robustness properties of financial models. Finally, we investigate the feasibility of realistic adversarial attacks in which an adversarial trader fools automated trading systems into making inaccurate predictions.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0