Summary

We present examples of agent-based and stochastic models of competition and business processes in economics and finance. We start from as simple as possible models, which have microscopic, agent-based, versions and macroscopic treatment in behavior. Microscopic and macroscopic versions of herding model proposed by Kirman and Bass diffusion of new products are considered in this contribution as two basic ideas. Further we demonstrate that general herding behavior can be considered as a background of nonlinear stochastic model of financial fluctuations.

AI Key Findings

Generated Sep 07, 2025

Methodology

The paper presents examples of agent-based and stochastic models of competition and business processes in economics and finance, starting from simple models with microscopic, agent-based versions and macroscopic treatments in behavior, such as the herding model proposed by Kirman and Bass diffusion of new products.

Key Results

- General herding behavior can be considered as a background of nonlinear stochastic model of financial fluctuations.

- A more sophisticated version of SDE was proposed to model trading activity and returns, incorporating two power-law regions with different values of β.

- The proposed form of the SDE enables reproduction of the main statistical properties of the return observed in financial markets, including two-power-law statistics for the probability density function and power spectral density.

Significance

This research contributes to the understanding of financial market dynamics by providing agent-based and macroscopic models, bridging the gap between microscopic and macroscopic approaches, and offering insights into the behavior-dependent trading activity exhibiting calm and excited stages.

Technical Contribution

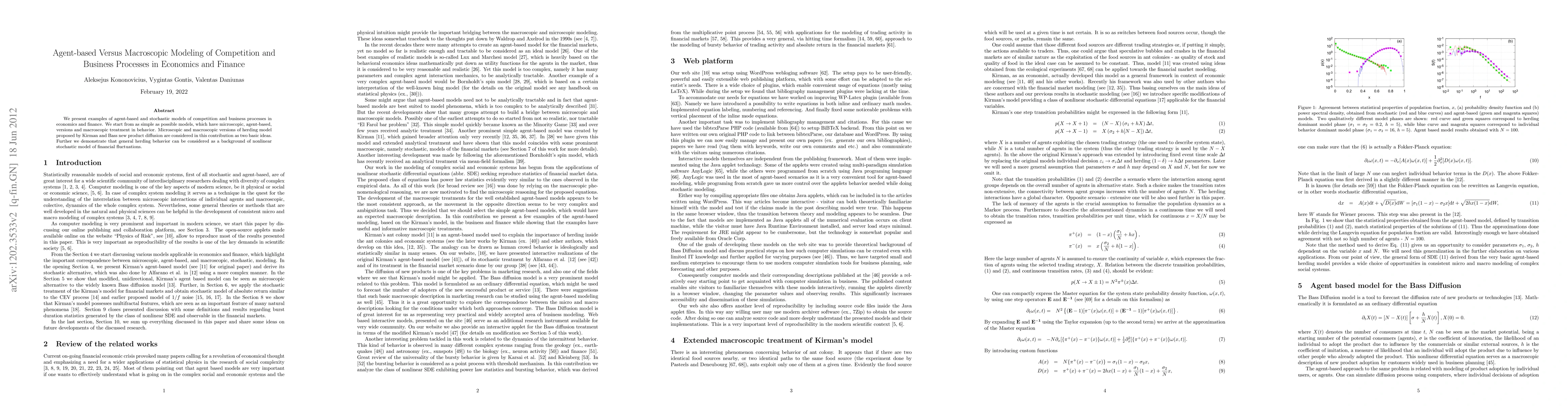

The paper introduces a nonlinear stochastic differential equation (17) to model return in financial markets, deriving the probability density function of burst durations and demonstrating its agreement with empirical time series of return.

Novelty

The work extends Kirman's ant colony model, introducing interevent time or trading activity as a function of the driving return, which generates feedback from macroscopic variables on the rate of microscopic processes and introduces strong nonlinearity in stochastic differential equations responsible for the long-range power-law statistics of financial variables.

Limitations

- The paper does not provide extensive empirical validation of the proposed models against real-world financial market data.

- The complexity of the models might limit their applicability in certain practical scenarios due to computational constraints.

Future Work

- Further development of stochastic models based on herding behavior of agents and nonlinear SDE (17) to better capture empirical data.

- Investigating burst statistics in financial markets in comparison with analytical results from nonlinear SDE as an independent method to adjust model parameters to empirical data.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

| Title | Authors | Year | Actions |

|---|

Comments (0)