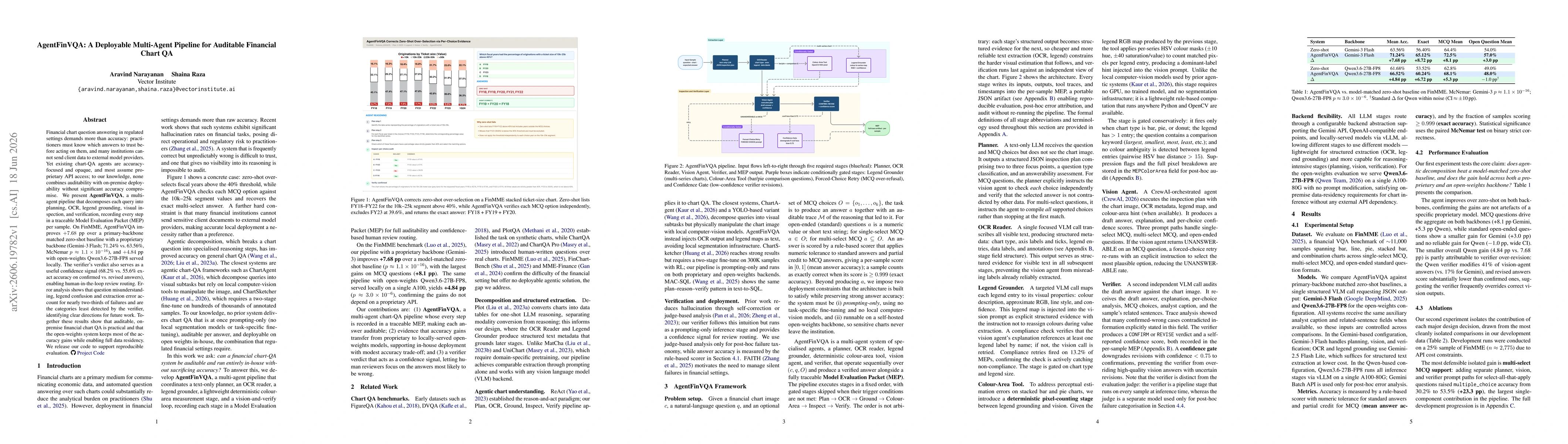

Financial chart question answering in regulated settings demands more than accuracy: practitioners must know which answers to trust before acting on them, and many institutions cannot send client data to external model providers. Yet existing chart-QA agents are accuracy-focused and opaque, and most assume proprietary API access; to our knowledge, none combines auditability with on-premise deployability without significant accuracy compromise. We present AgentFinVQA, a multi-agent pipeline that decomposes each query into planning, OCR, legend grounding, visual inspection, and verification, recording every step in a traceable Model Evaluation Packet (MEP) per sample. On FinMME, AgentFinVQA improves $+7.68$ pp over a primary-backbone matched zero-shot baseline with a proprietary backbone (Gemini-3 Flash; 71.24% vs. 63.56%, McNemar $p \approx 1.1 \times 10^{-16}$), and $+4.84$ pp with open-weights Qwen3.6-27B-FP8 served locally. The verifier's verdict also serves as a useful confidence signal (68.2% vs. 55.6% exact accuracy on confirmed vs. revised answers), enabling human-in-the-loop review routing. Error analysis shows that question misunderstanding, legend confusion and extraction error account for nearly two-thirds of failures and are the categories least detected by the verifier, identifying clear directions for future work. Together these results show that auditable, on-premise financial chart QA is practical and that the open-weights system keeps most of the accuracy gains while enabling full data residency. We release our code to support reproducible evaluation.

Discussion 0