AlgoXpert Alpha Research Framework. A Rigorous IS WFA OOS Protocol for Mitigating Overfitting in Quantitative Strategies

Publication

Metrics

Paper Preview

Abstract

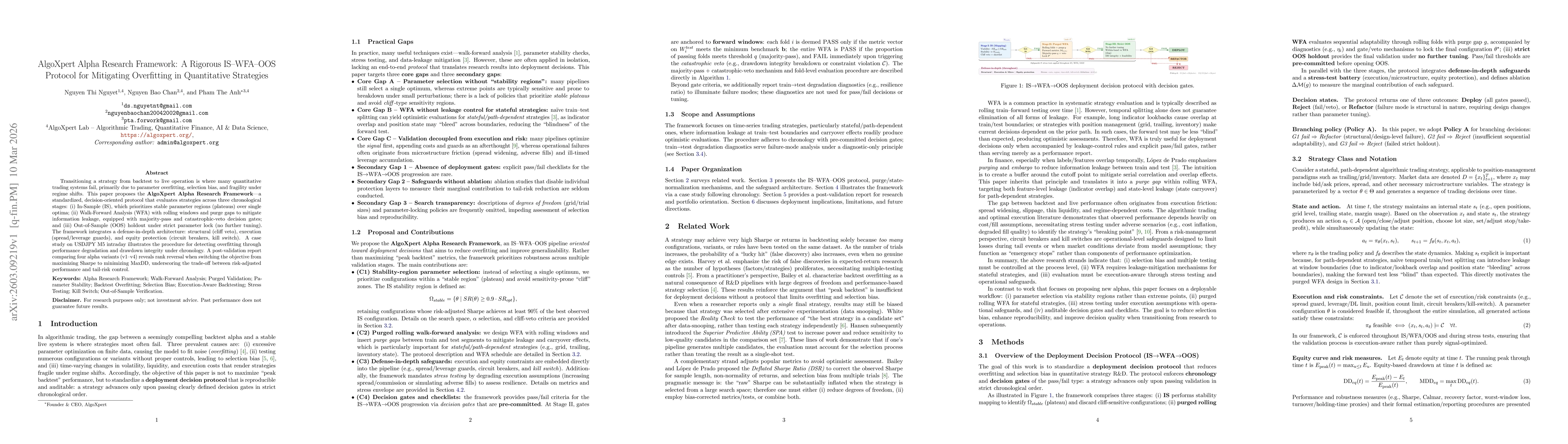

Transitioning a strategy from backtest to live trading is a common failure point for quantitative systems due to parameter overfitting, selection bias, and sensitivity to regime changes. This paper presents the AlgoXpert Alpha Research Framework, a standardized protocol that evaluates strategies across three stages: In Sample (IS), which focuses on stable parameter regions instead of single optima; Walk Forward Analysis (WFA) using rolling windows and purge gaps to reduce information leakage, supported by majority pass and catastrophic veto rules; and Out of Sample (OOS) testing under strict parameter lock with no further tuning. The framework applies a defense in depth structure that includes structural safeguards such as cliff veto, execution controls such as spread and leverage guards, and equity protection mechanisms such as circuit breakers and a kill switch. A case study on USDJPY M5 intraday data demonstrates how to detect overfitting through performance decay and drawdown behavior across chronological stages. A post validation comparison of four alpha variants (v1 to v4) shows rank reversal when the objective changes from maximizing Sharpe to minimizing maximum drawdown, highlighting the trade off between risk adjusted performance and tail risk control.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0