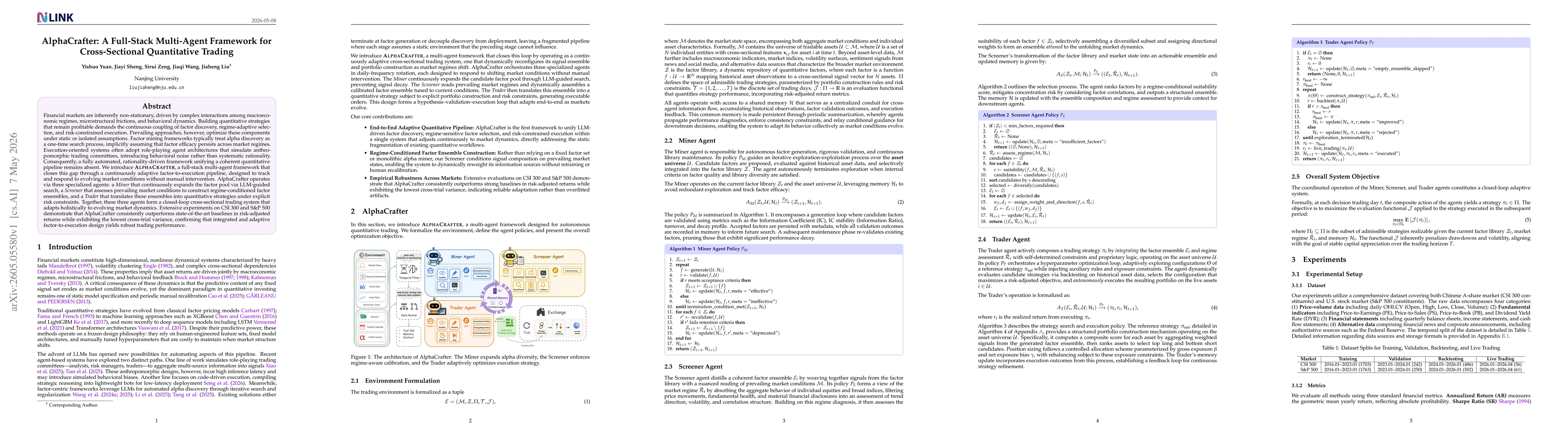

Financial markets are inherently non-stationary, driven by complex interactions among macroeconomic regimes, microstructural frictions, and behavioral dynamics. Building quantitative strategies that remain profitable demands the continuous coupling of factor discovery, regime-adaptive selection, and risk-constrained execution. Prevailing approaches, however, optimize these components under static or isolated assumptions. Factor mining frameworks typically treat alpha discovery as a one-time search process, implicitly assuming that factor efficacy persists across market regimes. Execution-oriented systems often adopt role-playing agent architectures that simulate anthropomorphic trading committees, introducing behavioral noise rather than systematic rationality. Consequently, a fully automated, rationality-driven framework unifying a coherent quantitative pipeline remains absent. We introduce AlphaCrafter, a full-stack multi-agent framework that closes this gap through a continuously adaptive factor-to-execution pipeline, designed to track and respond to evolving market conditions without manual intervention. AlphaCrafter operates via three specialized agents: a Miner that continuously expands the factor pool via LLM-guided search, a Screener that assesses prevailing market conditions to construct regime-conditioned factor ensembles, and a Trader that translates these ensembles into quantitative strategies under explicit risk constraints. Together, these three agents form a closed-loop cross-sectional trading system that adapts holistically to evolving market dynamics. Extensive experiments on CSI 300 and S&P 500 demonstrate that AlphaCrafter consistently outperforms state-of-the-art baselines in risk-adjusted returns while exhibiting the lowest cross-trial variance, confirming that integrated and adaptive factor-to-execution design yields robust trading performance.

Discussion 0