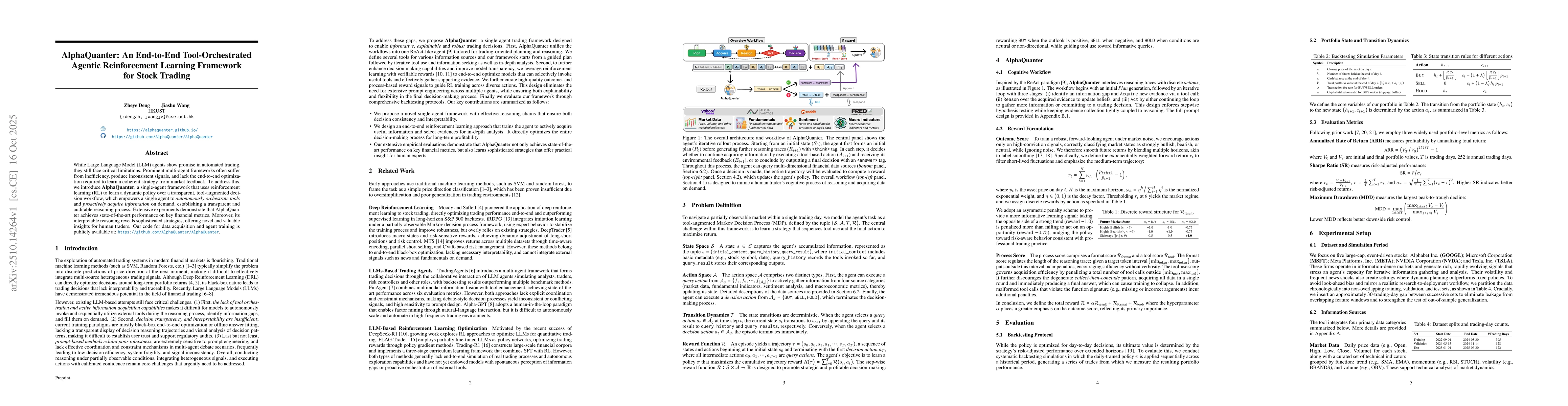

While Large Language Model (LLM) agents show promise in automated trading,

they still face critical limitations. Prominent multi-agent frameworks often

suffer from inefficiency, produce inconsistent signals, and lack the end-to-end

optimization required to learn a coherent strategy from market feedback. To

address this, we introduce AlphaQuanter, a single-agent framework that uses

reinforcement learning (RL) to learn a dynamic policy over a transparent,

tool-augmented decision workflow, which empowers a single agent to autonomously

orchestrate tools and proactively acquire information on demand, establishing a

transparent and auditable reasoning process. Extensive experiments demonstrate

that AlphaQuanter achieves state-of-the-art performance on key financial

metrics. Moreover, its interpretable reasoning reveals sophisticated

strategies, offering novel and valuable insights for human traders. Our code

for data acquisition and agent training is publicly available at:

https://github.com/AlphaQuanter/AlphaQuanter

Discussion 0