Summary

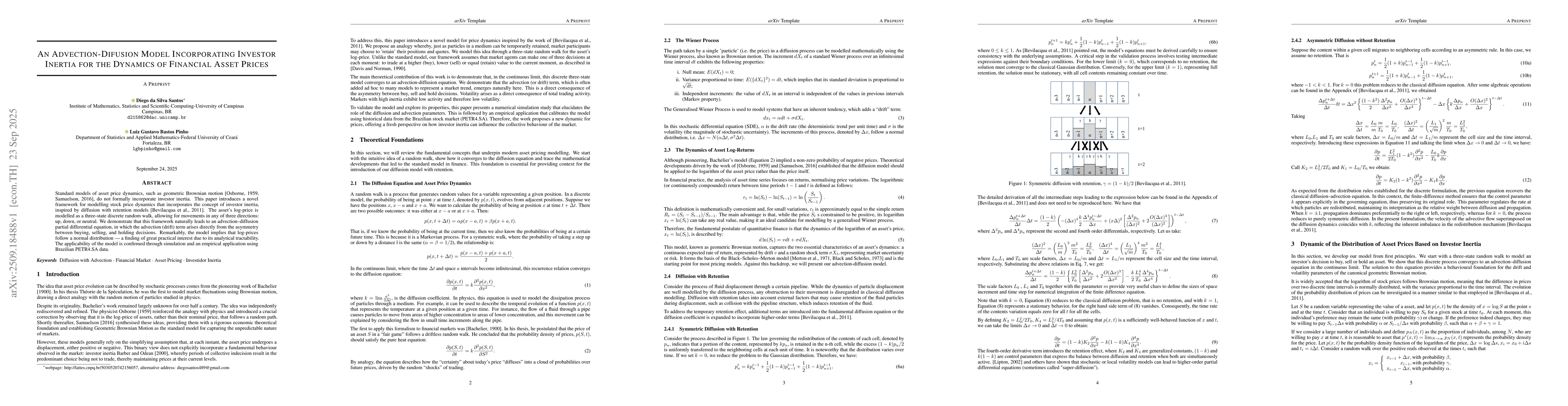

Standard models of asset price dynamics, such as geometric Brownian motion (Osborne, 1959, Samuelson, 2016), do not formally incorporate investor inertia. This paper introduces a novel framework for modelling stock price dynamics that incorporates the concept of investor inertia, inspired by diffusion with retention models (Bevilacqua, 2011). The asset's log-price is modelled as a three-state discrete random walk, allowing for movements in any of three directions: up, down, or neutral. We demonstrate that this framework naturally leads to an advection-diffusion partial differential equation, in which the advection (drift) term arises directly from the asymmetry between buying, selling, and holding decisions. Remarkably, the model implies that log-prices follow a normal distribution a finding of great practical interest due to its analytical tractability. The applicability of the model is confirmed through simulation and an empirical application using Brazilian PETR4.SA data.

AI Key Findings

Generated Sep 29, 2025

Methodology

The research derives the classical advection-diffusion equation from a discrete three-state random walk representing investor decisions: buy (β), sell (α), or refrain (γ). It validates the model using historical stock market data for PETR4.SA, estimating parameters from real-time series to generate stochastic price trajectories.

Key Results

- The model shows that volatility arises directly from total trading activity (α+β) or market inertia (1−γ).

- The advection coefficient (drift) is proportional to the imbalance between buying and selling forces (β−α), explaining market trends as a result of sentiment imbalance.

- The model produces normal distributions for log-returns, serving as a useful first-order approximation but failing to capture extreme events.

Significance

This research provides a microeconomic foundation for macroscopic market parameters (drift and volatility), bridging the gap between individual investor behavior and aggregate market dynamics. It offers a more intuitive understanding of volatility as a consequence of trading activity rather than an exogenous factor.

Technical Contribution

The paper rigorously derives the classical advection-diffusion equation from a discrete three-state random walk, establishing a clear link between investor decision probabilities (β, α, γ) and macroscopic market parameters (drift and volatility).

Novelty

This work introduces a microeconomic foundation for the advection-diffusion equation in financial markets by explicitly modeling investor decision-making processes, which is absent in traditional macroeconomic models of asset pricing.

Limitations

- The model's simplest solution yields normal distributions for log-returns, which cannot capture extreme market events observed in empirical data.

- The study does not explore higher-order differential terms that could explain heavy-tailed distributions in financial markets.

Future Work

- Investigate how the inertia parameter γ could introduce fourth-order differential terms to better model heavy-tailed distributions.

- Apply the model to other financial assets and market conditions to test its generalizability.

- Incorporate machine learning techniques to improve parameter estimation and model calibration.

Comments (0)