An Economy of Neural Networks: Learning from Heterogeneous Experiences

Publication

Metrics

Paper Preview

Abstract

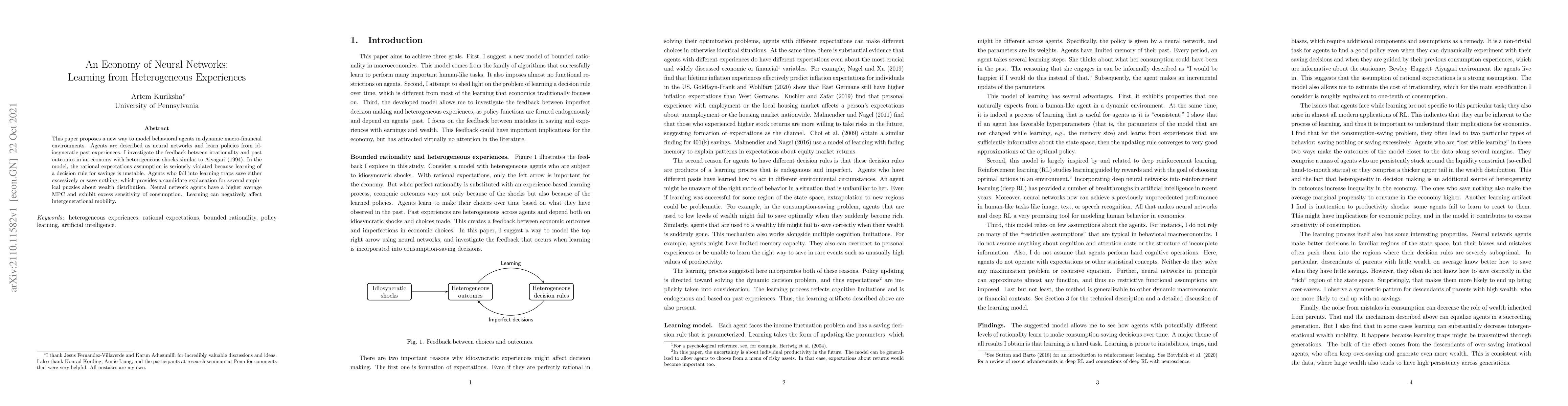

This paper proposes a new way to model behavioral agents in dynamic macro-financial environments. Agents are described as neural networks and learn policies from idiosyncratic past experiences. I investigate the feedback between irrationality and past outcomes in an economy with heterogeneous shocks similar to Aiyagari (1994). In the model, the rational expectations assumption is seriously violated because learning of a decision rule for savings is unstable. Agents who fall into learning traps save either excessively or save nothing, which provides a candidate explanation for several empirical puzzles about wealth distribution. Neural network agents have a higher average MPC and exhibit excess sensitivity of consumption. Learning can negatively affect intergenerational mobility.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0