An Efficient and Generalizable Symbolic Regression Method for Time Series Analysis

Publication

Metrics

AI Quick Summary

This research introduces NEMoTS, a Neural-Enhanced Monte Carlo Tree Search method for efficient and generalizable symbolic regression in time series analysis, improving both computational efficiency and interpretability over existing quantitative methods. Experiments on real-world datasets show NEMoTS's superior performance in terms of speed, reliability, and ability to reveal underlying patterns.

Paper Preview

Abstract

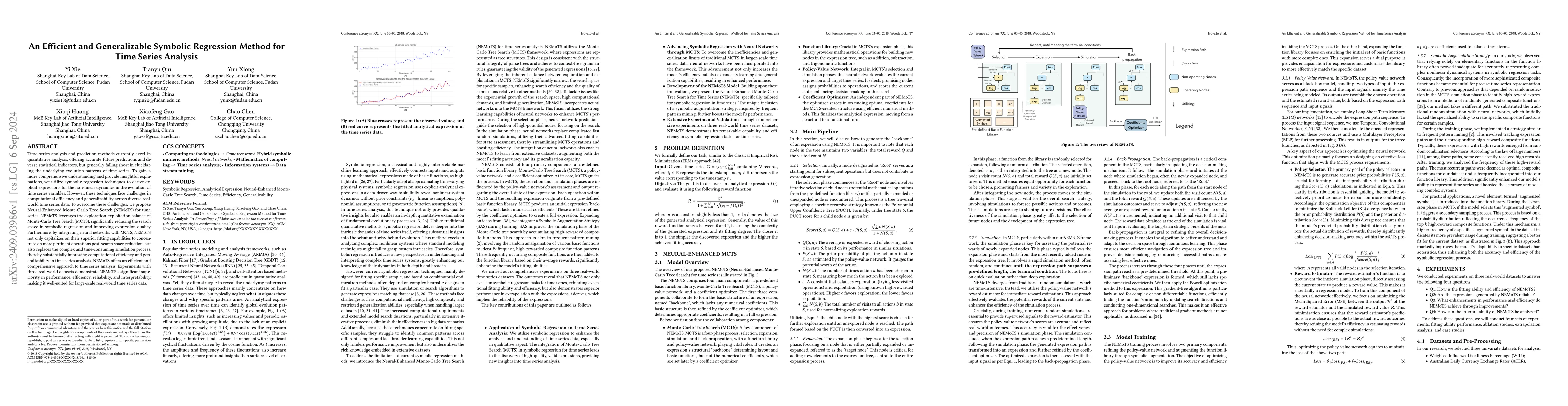

Time series analysis and prediction methods currently excel in quantitative analysis, offering accurate future predictions and diverse statistical indicators, but generally falling short in elucidating the underlying evolution patterns of time series. To gain a more comprehensive understanding and provide insightful explanations, we utilize symbolic regression techniques to derive explicit expressions for the non-linear dynamics in the evolution of time series variables. However, these techniques face challenges in computational efficiency and generalizability across diverse real-world time series data. To overcome these challenges, we propose \textbf{N}eural-\textbf{E}nhanced \textbf{Mo}nte-Carlo \textbf{T}ree \textbf{S}earch (NEMoTS) for time series. NEMoTS leverages the exploration-exploitation balance of Monte-Carlo Tree Search (MCTS), significantly reducing the search space in symbolic regression and improving expression quality. Furthermore, by integrating neural networks with MCTS, NEMoTS not only capitalizes on their superior fitting capabilities to concentrate on more pertinent operations post-search space reduction, but also replaces the complex and time-consuming simulation process, thereby substantially improving computational efficiency and generalizability in time series analysis. NEMoTS offers an efficient and comprehensive approach to time series analysis. Experiments with three real-world datasets demonstrate NEMoTS's significant superiority in performance, efficiency, reliability, and interpretability, making it well-suited for large-scale real-world time series data.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0