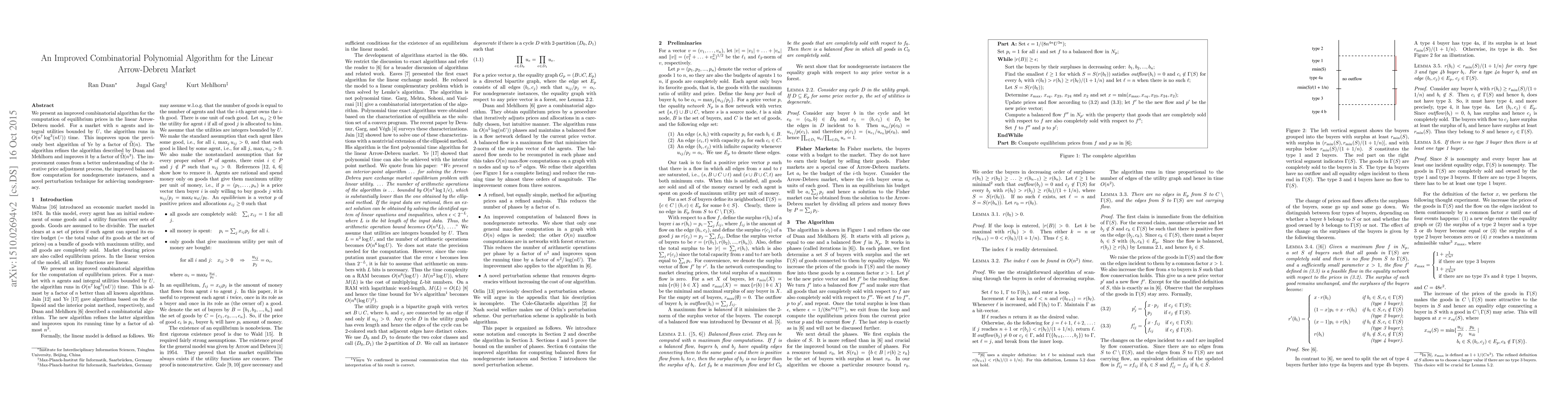

An Improved Combinatorial Polynomial Algorithm for the Linear Arrow-Debreu Market

Publication

Metrics

AI Quick Summary

This paper presents an enhanced combinatorial algorithm for computing equilibrium prices in the linear Arrow-Debreu market, achieving a runtime of $O(n^7 \log^3 (nU))$, which improves upon previous algorithms by factors of $\tOmega(n)$ and $\tOmega(n^3)$. The enhancements stem from a refined iterative price adjustment, improved balanced flow computation, and a novel perturbation technique.

Paper Preview

Abstract

We present an improved combinatorial algorithm for the computation of equilibrium prices in the linear Arrow-Debreu model. For a market with $n$ agents and integral utilities bounded by $U$, the algorithm runs in $O(n^7 \log^3 (nU))$ time. This improves upon the previously best algorithm of Ye by a factor of $\tOmega(n)$. The algorithm refines the algorithm described by Duan and Mehlhorn and improves it by a factor of $\tOmega(n^3)$. The improvement comes from a better understanding of the iterative price adjustment process, the improved balanced flow computation for nondegenerate instances, and a novel perturbation technique for achieving nondegeneracy.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0