An Outer Approximation Method for Solving Mixed-Integer Convex Quadratic Programs with Indicators

Publication

Metrics

AI Quick Summary

This paper proposes a new outer approximation method for solving mixed-integer convex quadratic programs with indicator variables, leveraging advanced cutting planes derived from convex relaxations. The study demonstrates significant speedups in solving large-scale problems, particularly in the context of sparse portfolio selection, compared to existing state-of-the-art methods.

Paper Preview

Abstract

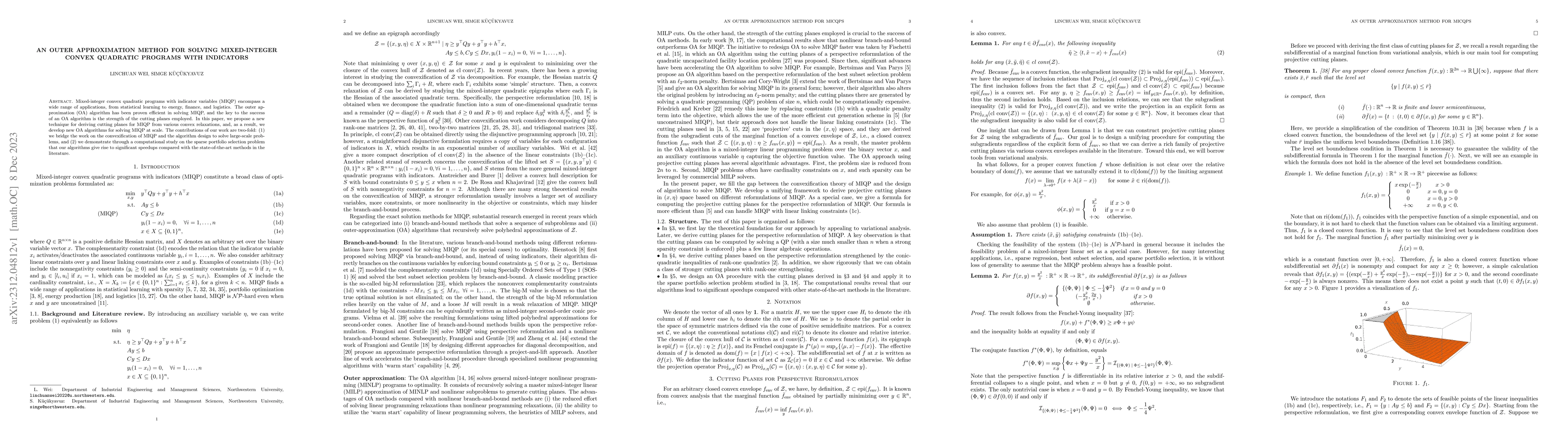

Mixed-integer convex quadratic programs with indicator variables (MIQP) encompass a wide range of applications, from statistical learning to energy, finance, and logistics. The outer approximation (OA) algorithm has been proven efficient in solving MIQP, and the key to the success of an OA algorithm is the strength of the cutting planes employed. In this paper, we propose a new technique for deriving cutting planes for MIQP from various convex relaxations, and, as a result, we develop new OA algorithms for solving MIQP at scale. The contributions of our work are two-fold: (1) we bridge the work on the convexification of MIQP and the algorithm design to solve large-scale problems, and (2) we demonstrate through a computational study on the sparse portfolio selection problem that our algorithms give rise to significant speedups compared with the state-of-the-art methods in the literature.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0