Approximating inverse cumulative distribution functions to produce approximate random variables

Publication

Metrics

AI Quick Summary

This paper introduces computationally inexpensive approximations to inverse cumulative distribution functions for generating approximate random variables, particularly for Gaussian distributions. These approximations enable significant speedups in Monte Carlo simulations, with demonstrated convergence and bounded error, leading to substantial computational savings in both C and C++ implementations.

Paper Preview

Abstract

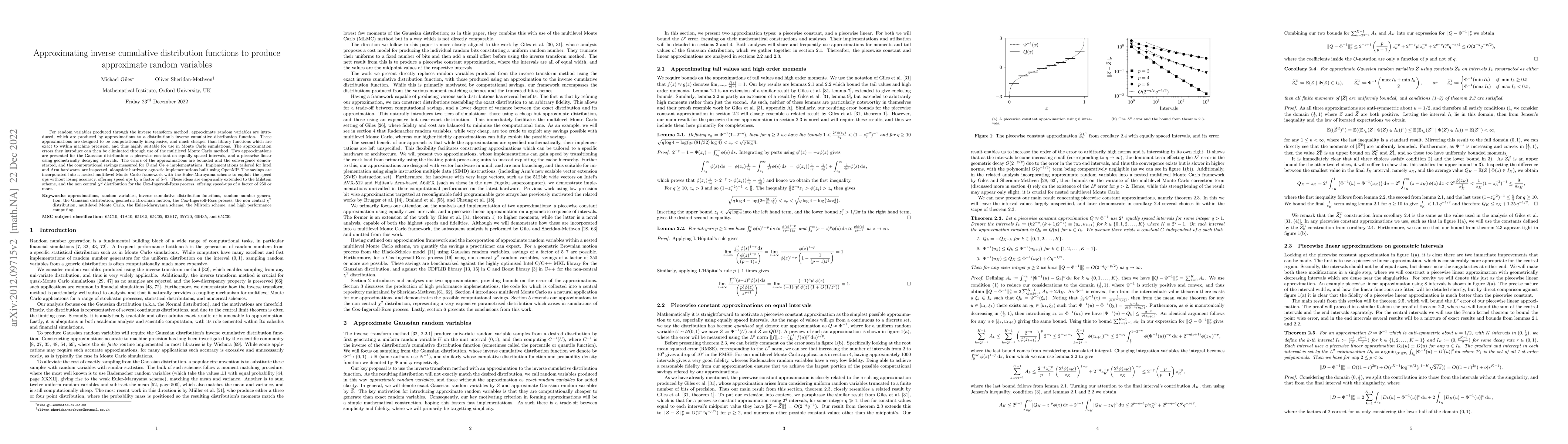

For random variables produced through the inverse transform method, approximate random variables are introduced, which are produced by approximations to a distribution's inverse cumulative distribution function. These approximations are designed to be computationally inexpensive, and much cheaper than exact library functions, and thus highly suitable for use in Monte Carlo simulations. Two approximations are presented for the Gaussian distribution: a piecewise constant on equally spaced intervals, and a piecewise linear using geometrically decaying intervals. The error of the approximations are bounded and the convergence demonstrated, and the computational savings measured for C and C++ implementations. Implementations tailored for Intel and Arm hardwares are inspected, alongside hardware agnostic implementations built using OpenMP. The savings are incorporated into a nested multilevel Monte Carlo framework with the Euler-Maruyama scheme to exploit the speed ups without losing accuracy, offering speed ups by a factor of 5--7. These ideas are empirically extended to the Milstein scheme, and the Cox-Ingersoll-Ross process' non central chi-squared distribution, which offer speed ups by a factor of 250 or more.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0