Summary

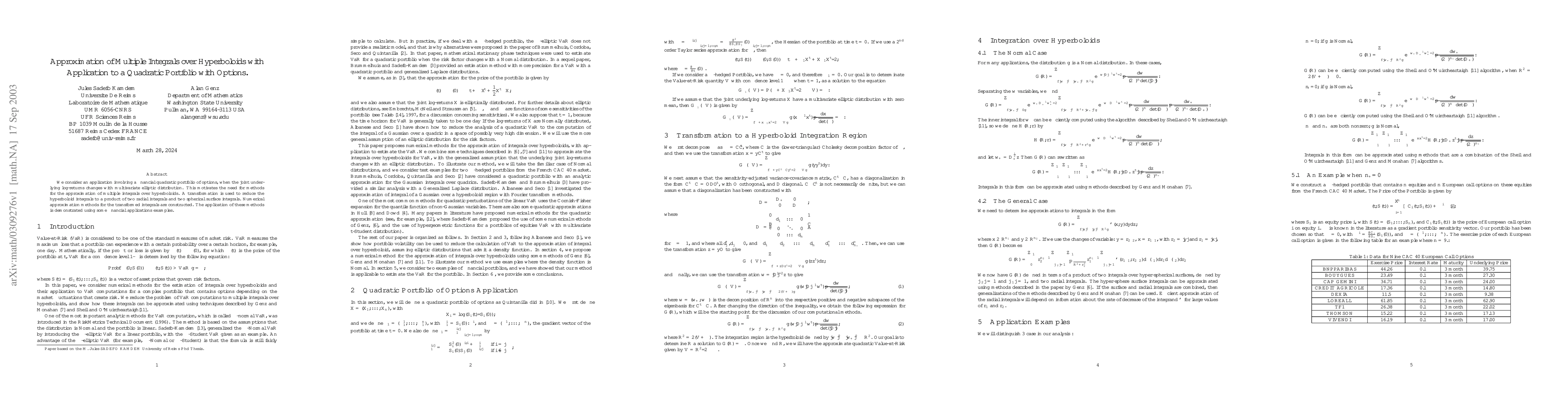

We consider an application involving a financial quadratic portfolio of options, when the joint underlying log-returns changes with multivariate elliptic distribution. This motivates the needs for methods for the approximation of multiple integrals over hyperboloids. A transformation is used to reduce the hyperboloid integrals to a product of two radial integrals and two spherical surface integrals. Numerical approximation methods for the transformed integrals are constructed. The application of these methods is demonstrated using some financial applications examples.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Comments (0)