ARMA Cell: A Modular and Effective Approach for Neural Autoregressive Modeling

Publication

Metrics

AI Quick Summary

The ARMA cell presents a modular and effective approach for neural autoregressive modeling, offering a simpler alternative to complex RNNs like LSTMs for time series data. The ConvARMA cell extends this methodology for spatially-correlated time series, demonstrating competitive performance and robustness.

Paper Preview

Abstract

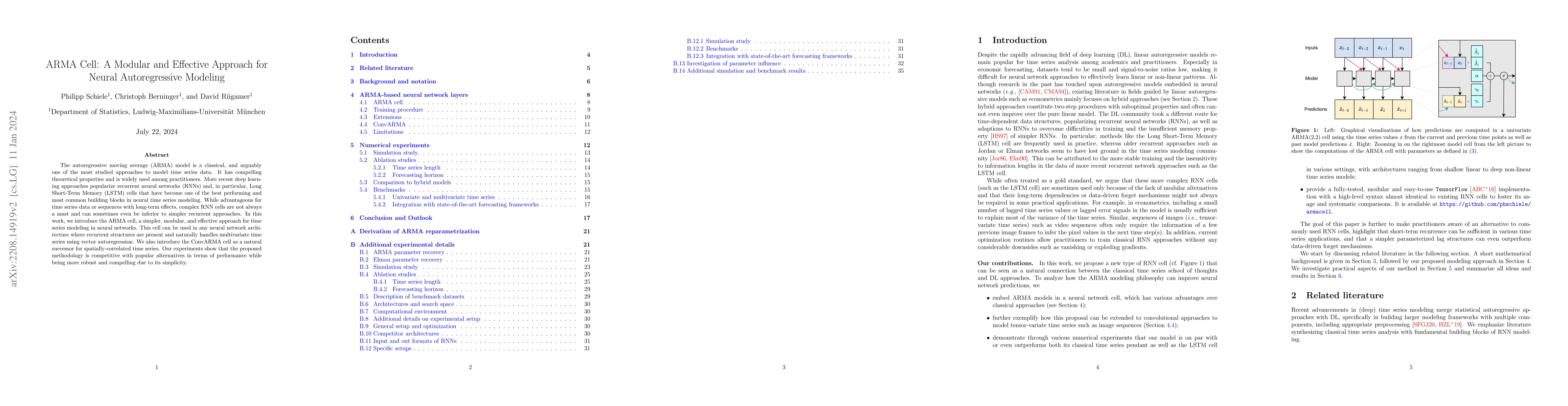

The autoregressive moving average (ARMA) model is a classical, and arguably one of the most studied approaches to model time series data. It has compelling theoretical properties and is widely used among practitioners. More recent deep learning approaches popularize recurrent neural networks (RNNs) and, in particular, Long Short-Term Memory (LSTM) cells that have become one of the best performing and most common building blocks in neural time series modeling. While advantageous for time series data or sequences with long-term effects, complex RNN cells are not always a must and can sometimes even be inferior to simpler recurrent approaches. In this work, we introduce the ARMA cell, a simpler, modular, and effective approach for time series modeling in neural networks. This cell can be used in any neural network architecture where recurrent structures are present and naturally handles multivariate time series using vector autoregression. We also introduce the ConvARMA cell as a natural successor for spatially-correlated time series. Our experiments show that the proposed methodology is competitive with popular alternatives in terms of performance while being more robust and compelling due to its simplicity

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0