Auto-Regressive Moving Diffusion Models for Time Series Forecasting

Publication

Metrics

AI Quick Summary

The paper proposes an Auto-Regressive Moving Diffusion (ARMD) model for time series forecasting that aligns the diffusion process with the forecasting objective by leveraging intermediate state information, achieving state-of-the-art performance on seven datasets compared to existing diffusion-based models. The ARMD model reinterprets diffusion using a sliding-based technique, starting from future series as the initial state and historical series as the final state.

Paper Preview

Abstract

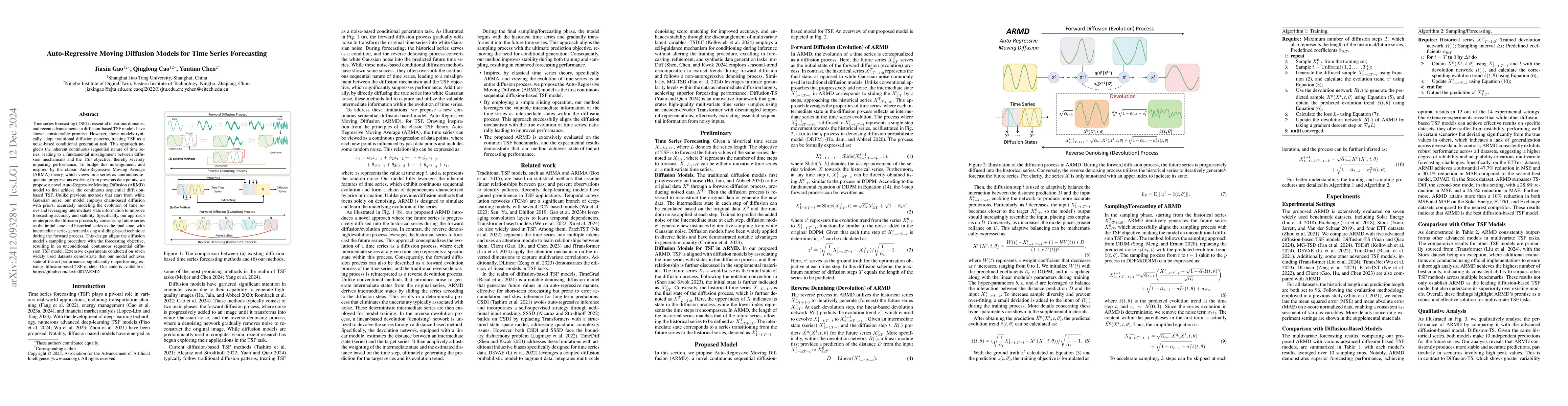

Time series forecasting (TSF) is essential in various domains, and recent advancements in diffusion-based TSF models have shown considerable promise. However, these models typically adopt traditional diffusion patterns, treating TSF as a noise-based conditional generation task. This approach neglects the inherent continuous sequential nature of time series, leading to a fundamental misalignment between diffusion mechanisms and the TSF objective, thereby severely impairing performance. To bridge this misalignment, and inspired by the classic Auto-Regressive Moving Average (ARMA) theory, which views time series as continuous sequential progressions evolving from previous data points, we propose a novel Auto-Regressive Moving Diffusion (ARMD) model to first achieve the continuous sequential diffusion-based TSF. Unlike previous methods that start from white Gaussian noise, our model employs chain-based diffusion with priors, accurately modeling the evolution of time series and leveraging intermediate state information to improve forecasting accuracy and stability. Specifically, our approach reinterprets the diffusion process by considering future series as the initial state and historical series as the final state, with intermediate series generated using a sliding-based technique during the forward process. This design aligns the diffusion model's sampling procedure with the forecasting objective, resulting in an unconditional, continuous sequential diffusion TSF model. Extensive experiments conducted on seven widely used datasets demonstrate that our model achieves state-of-the-art performance, significantly outperforming existing diffusion-based TSF models. Our code is available on GitHub: https://github.com/daxin007/ARMD.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Paper Details

Authors

PDF Preview

Related Papers

No references found for this paper.

Discussion 0