Stock prices are highly volatile and sudden changes in trends are often very

problematic for traditional forecasting models to handle. The standard Long

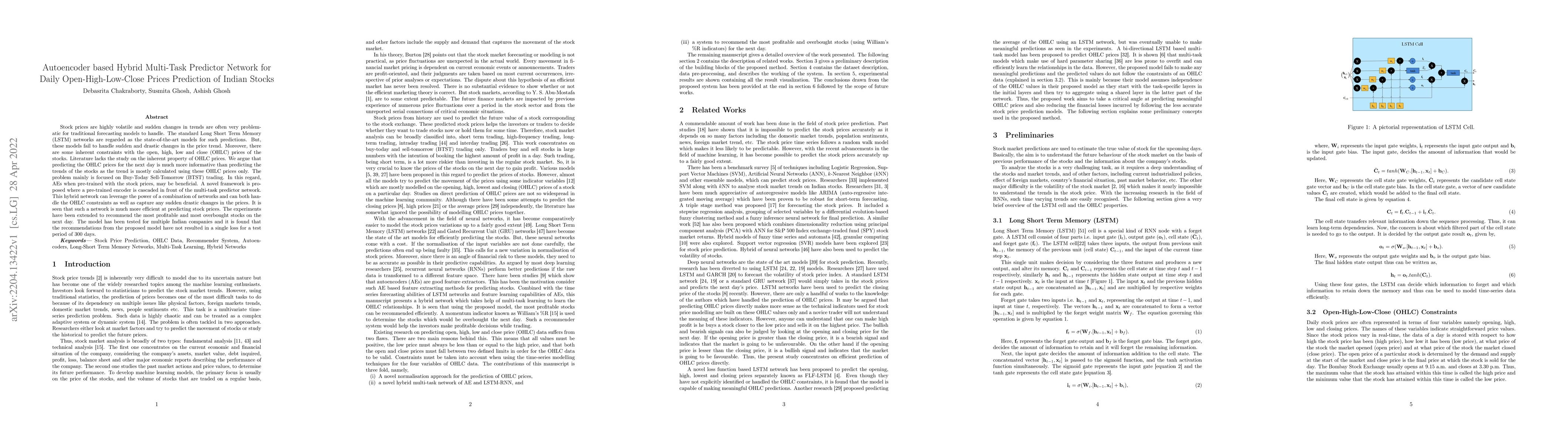

Short Term Memory (LSTM) networks are regarded as the state-of-the-art models

for such predictions. But, these models fail to handle sudden and drastic

changes in the price trend. Moreover, there are some inherent constraints with

the open, high, low and close (OHLC) prices of the stocks. Literature lacks the

study on the inherent property of OHLC prices. We argue that predicting the

OHLC prices for the next day is much more informative than predicting the

trends of the stocks as the trend is mostly calculated using these OHLC prices

only. The problem mainly is focused on Buy-Today Sell-Tomorrow (BTST) trading.

In this regard, AEs when pre-trained with the stock prices, may be beneficial.

A novel framework is proposed where a pre-trained encoder is cascaded in front

of the multi-task predictor network. This hybrid network can leverage the power

of a combination of networks and can both handle the OHLC constraints as well

as capture any sudden drastic changes in the prices. It is seen that such a

network is much more efficient at predicting stock prices. The experiments have

been extended to recommend the most profitable and most overbought stocks on

the next day. The model has been tested for multiple Indian companies and it is

found that the recommendations from the proposed model have not resulted in a

single loss for a test period of 300 days.

Discussion 0