Background-aware Multi-source Fusion Financial Trend Forecasting Mechanism

Publication

Metrics

AI Quick Summary

This research proposes a background-aware multi-source fusion mechanism for financial trend forecasting that integrates textual and numerical data. It leverages large language models to extract and fuse policy and stock review texts with stock price data, using deep learning architectures for improved prediction accuracy. Comparative results show superior performance over traditional models.

Paper Preview

Abstract

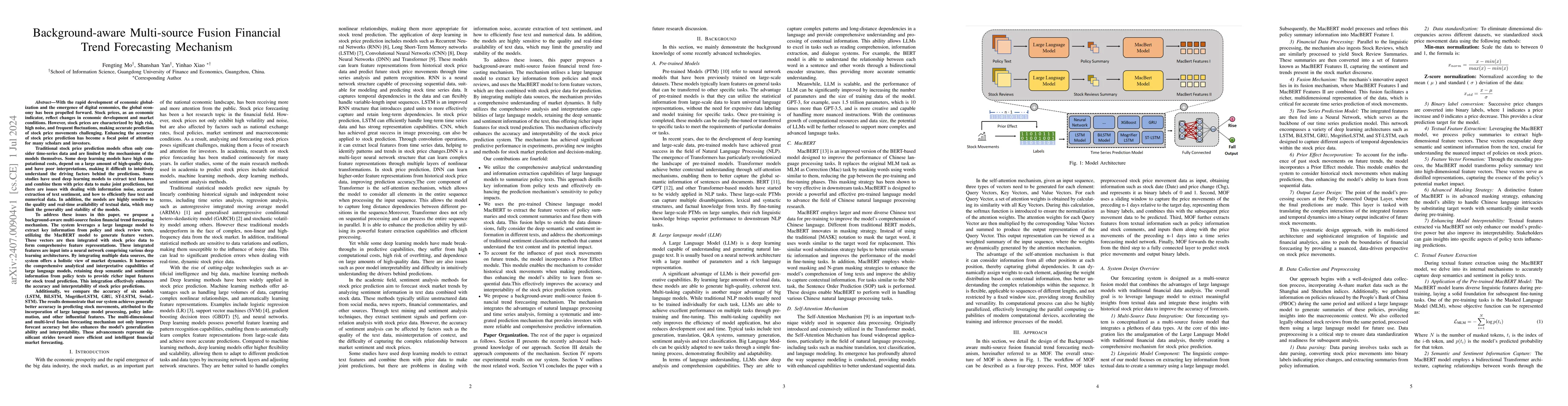

Stock prices, as an economic indicator, reflect changes in economic development and market conditions. Traditional stock price prediction models often only consider time-series data and are limited by the mechanisms of the models themselves. Some deep learning models have high computational costs, depend on a large amount of high-quality data, and have poor interpretations, making it difficult to intuitively understand the driving factors behind the predictions. Some studies have used deep learning models to extract text features and combine them with price data to make joint predictions, but there are issues with dealing with information noise, accurate extraction of text sentiment, and how to efficiently fuse text and numerical data. To address these issues in this paper, we propose a background-aware multi-source fusion financial trend forecasting mechanism. The system leverages a large language model to extract key information from policy and stock review texts, utilizing the MacBERT model to generate feature vectors. These vectors are then integrated with stock price data to form comprehensive feature representations. These integrated features are input into a neural network comprising various deep learning architectures. By integrating multiple data sources, the system offers a holistic view of market dynamics. It harnesses the comprehensive analytical and interpretative capabilities of large language models, retaining deep semantic and sentiment information from policy texts to provide richer input features for stock trend prediction. Additionally, we compare the accuracy of six models (LSTM, BiLSTM, MogrifierLSTM, GRU, ST-LSTM, SwinLSTM). The results demonstrate that our system achieves generally better accuracy in predicting stock movements, attributed to the incorporation of large language model processing, policy information, and other influential features.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0