Publication

Metrics

AI Quick Summary

This study introduces Bayesian Tobit quantile regression models for endogenous variables, assuming zero $\alpha$-th quantile of the error term in the first stage. It estimates the unknown $\alpha$ and demonstrates the model using simulated and real labour supply data.

Paper Preview

Abstract

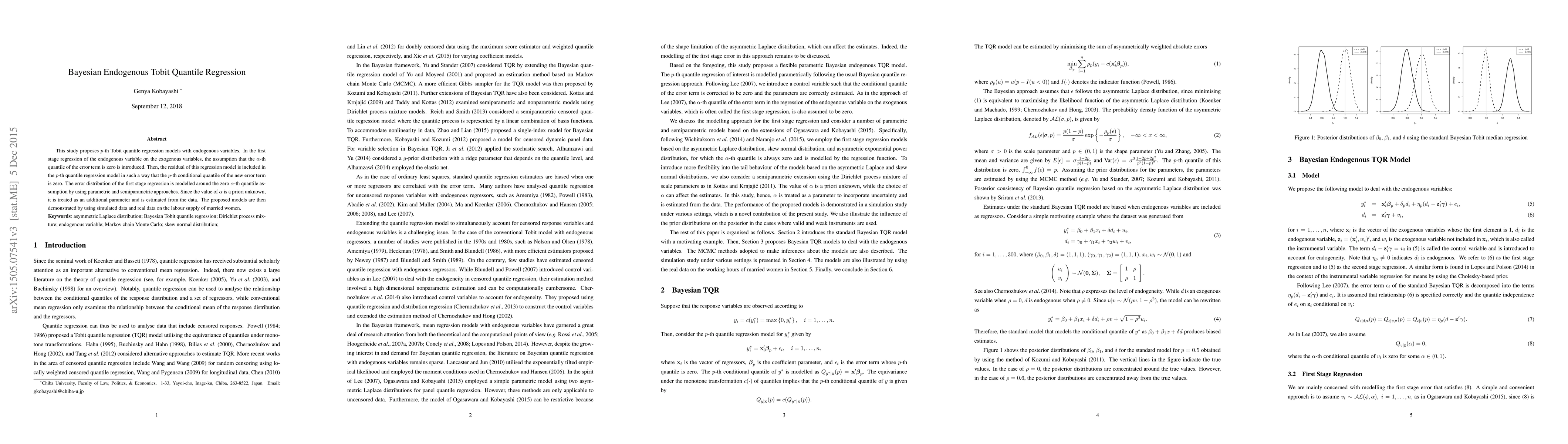

This study proposes $p$-th Tobit quantile regression models with endogenous variables. In the first stage regression of the endogenous variable on the exogenous variables, the assumption that the $\alpha$-th quantile of the error term is zero is introduced. Then, the residual of this regression model is included in the $p$-th quantile regression model in such a way that the $p$-th conditional quantile of the new error term is zero. The error distribution of the first stage regression is modelled around the zero $\alpha$-th quantile assumption by using parametric and semiparametric approaches. Since the value of $\alpha$ is a priori unknown, it is treated as an additional parameter and is estimated from the data. The proposed models are then demonstrated by using simulated data and real data on the labour supply of married women.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0