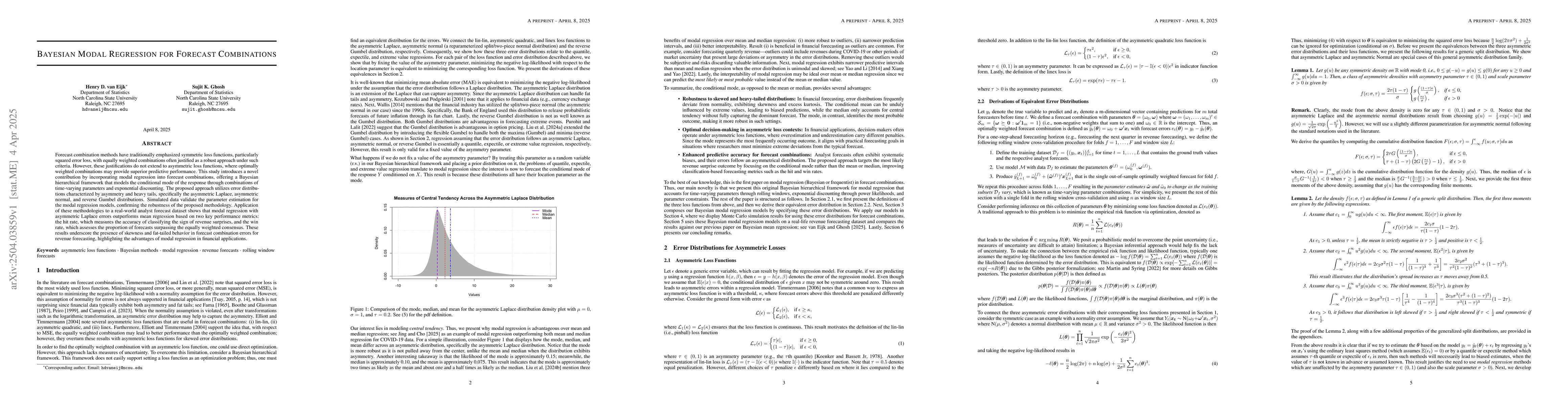

Forecast combination methods have traditionally emphasized symmetric loss

functions, particularly squared error loss, with equally weighted combinations

often justified as a robust approach under such criteria. However, these

justifications do not extend to asymmetric loss functions, where optimally

weighted combinations may provide superior predictive performance. This study

introduces a novel contribution by incorporating modal regression into forecast

combinations, offering a Bayesian hierarchical framework that models the

conditional mode of the response through combinations of time-varying

parameters and exponential discounting. The proposed approach utilizes error

distributions characterized by asymmetry and heavy tails, specifically the

asymmetric Laplace, asymmetric normal, and reverse Gumbel distributions.

Simulated data validate the parameter estimation for the modal regression

models, confirming the robustness of the proposed methodology. Application of

these methodologies to a real-world analyst forecast dataset shows that modal

regression with asymmetric Laplace errors outperforms mean regression based on

two key performance metrics: the hit rate, which measures the accuracy of

classifying the sign of revenue surprises, and the win rate, which assesses the

proportion of forecasts surpassing the equally weighted consensus. These

results underscore the presence of skewness and fat-tailed behavior in forecast

combination errors for revenue forecasting, highlighting the advantages of

modal regression in financial applications.

Discussion 0