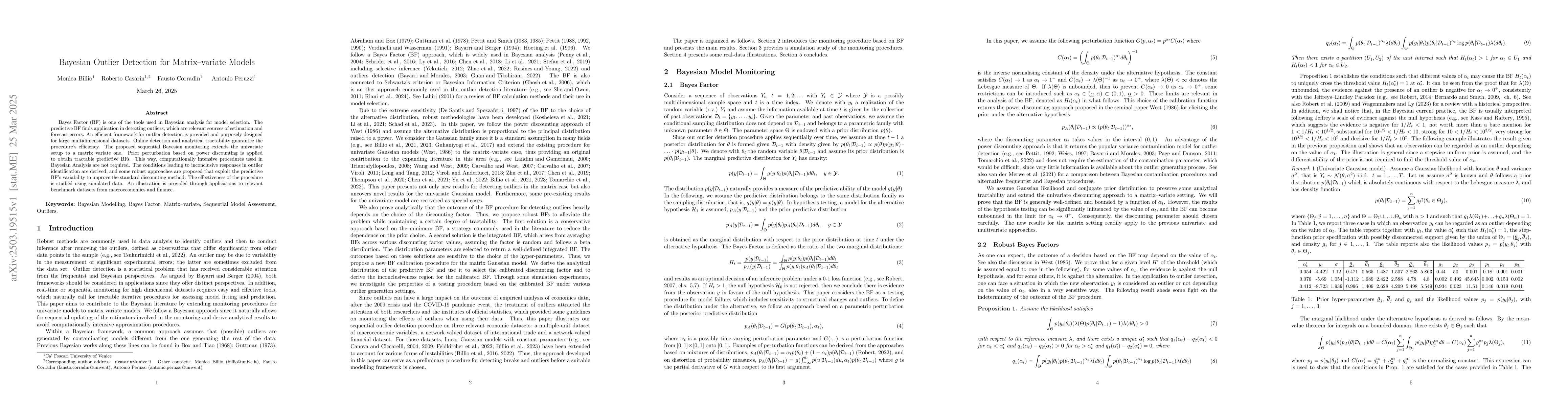

Bayes Factor (BF) is one of the tools used in Bayesian analysis for model

selection. The predictive BF finds application in detecting outliers, which are

relevant sources of estimation and forecast errors. An efficient framework for

outlier detection is provided and purposely designed for large multidimensional

datasets. Online detection and analytical tractability guarantee the

procedure's efficiency. The proposed sequential Bayesian monitoring extends the

univariate setup to a matrix--variate one. Prior perturbation based on power

discounting is applied to obtain tractable predictive BFs. This way,

computationally intensive procedures used in Bayesian Analysis are not

required. The conditions leading to inconclusive responses in outlier

identification are derived, and some robust approaches are proposed that

exploit the predictive BF's variability to improve the standard discounting

method. The effectiveness of the procedure is studied using simulated data. An

illustration is provided through applications to relevant benchmark datasets

from macroeconomics and finance.

Discussion 0