Bayesian Poisson-Randomized Gamma Tensor Factorization with Application to International Trade Flows

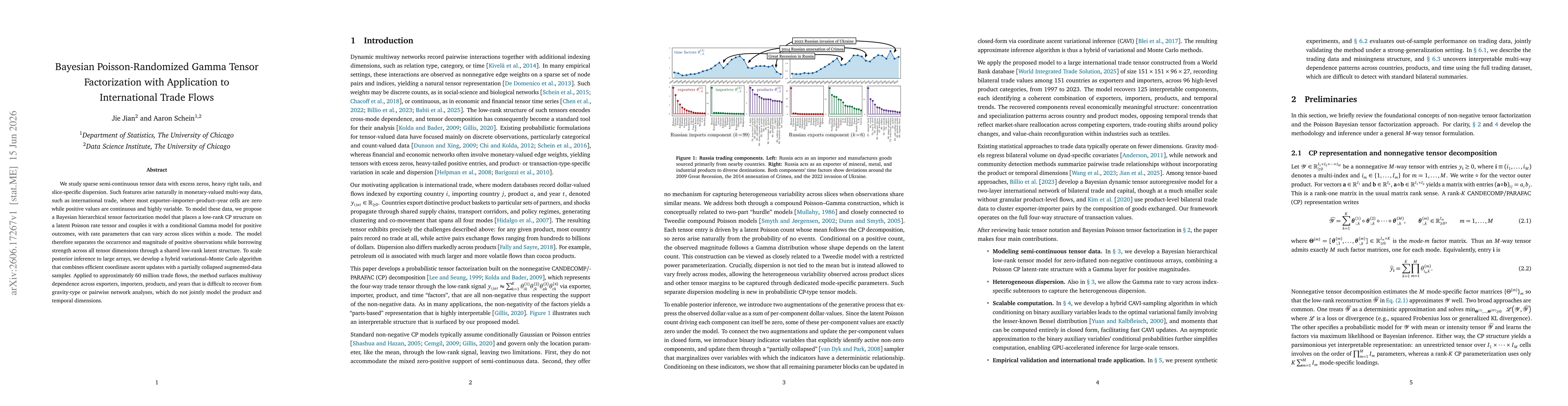

Publication

Metrics

AI Quick Summary

The paper develops a Bayesian tensor factorization model for sparse, heavy-tailed multiway data by combining a low-rank Poisson rate tensor with a conditional Gamma model for positive values, allowing slice-specific dispersion across exporters, importers, products, and years. It introduces a scalable hybrid variational–Monte Carlo inference method and shows it uncovers multiway trade patterns in about 60 million flows that are hard to detect with traditional gravity or pairwise analyses.

Paper Preview

Abstract

We study sparse semi-continuous tensor data with excess zeros, heavy right tails, and slice-specific dispersion. Such features arise naturally in monetary-valued multi-way data, such as international trade, where most exporter--importer--product--year cells are zero while positive values are continuous and highly variable. To model these data, we propose a Bayesian hierarchical tensor factorization model that places a low-rank CP structure on a latent Poisson rate tensor and couples it with a conditional Gamma model for positive outcomes, with rate parameters that can vary across slices within a mode. The model therefore separates the occurrence and magnitude of positive observations while borrowing strength across all tensor dimensions through a shared low-rank latent structure. To scale posterior inference to large arrays, we develop a hybrid variational--Monte Carlo algorithm that combines efficient coordinate ascent updates with a partially collapsed augmented-data sampler. Applied to approximately 60 million trade flows, the method surfaces multiway dependence across exporters, importers, products, and years that is difficult to recover from gravity-type or pairwise network analyses, which do not jointly model the product and temporal dimensions.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0