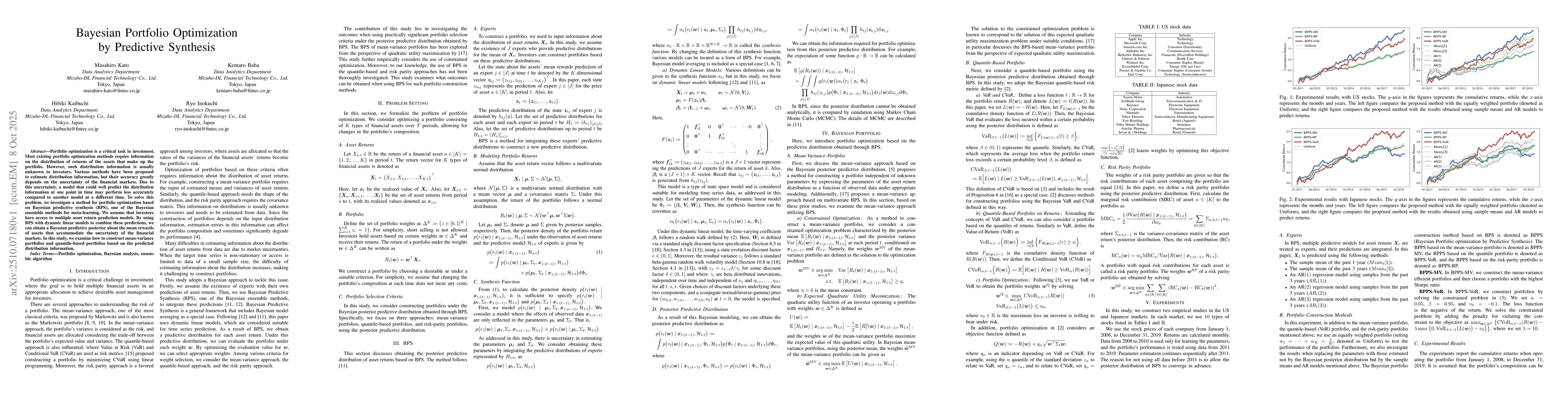

Portfolio optimization is a critical task in investment. Most existing

portfolio optimization methods require information on the distribution of

returns of the assets that make up the portfolio. However, such distribution

information is usually unknown to investors. Various methods have been proposed

to estimate distribution information, but their accuracy greatly depends on the

uncertainty of the financial markets. Due to this uncertainty, a model that

could well predict the distribution information at one point in time may

perform less accurately compared to another model at a different time. To solve

this problem, we investigate a method for portfolio optimization based on

Bayesian predictive synthesis (BPS), one of the Bayesian ensemble methods for

meta-learning. We assume that investors have access to multiple asset return

prediction models. By using BPS with dynamic linear models to combine these

predictions, we can obtain a Bayesian predictive posterior about the mean

rewards of assets that accommodate the uncertainty of the financial markets. In

this study, we examine how to construct mean-variance portfolios and

quantile-based portfolios based on the predicted distribution information.

Discussion 0