01

MethodologyHow they did it

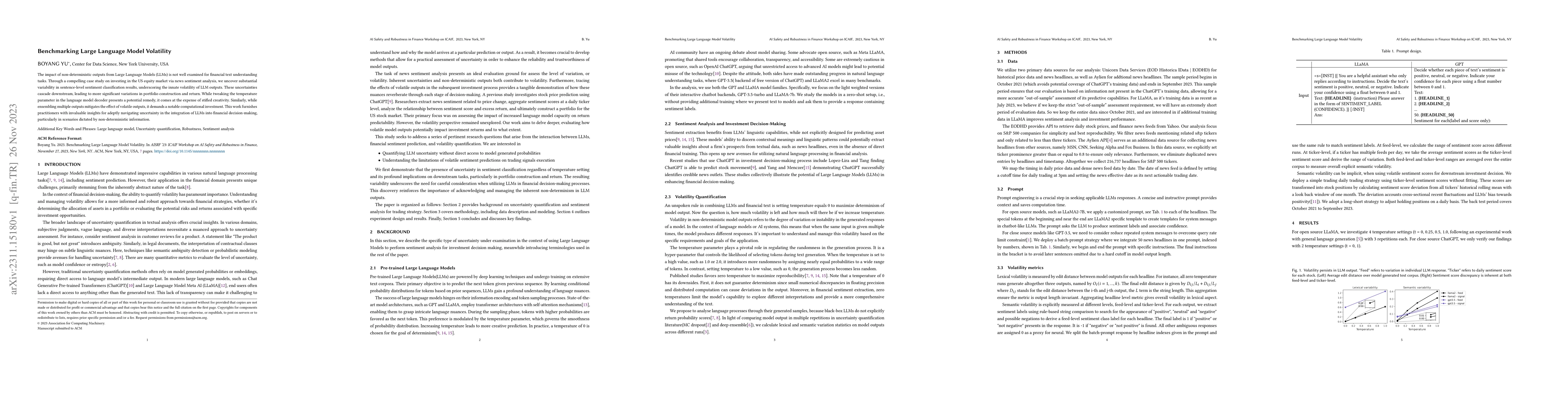

The study utilizes two primary data sources: Unicorn Data Services for historical price data and news headlines, and Aylien for additional news headlines. The analysis focuses on S&P500 companies, filtering news feeds mentioning related tickers. Prompt engineering is crucial, with customized prompts for open-source models like LLaMA2-7B and a batch-prompt strategy for closed-source models like GPT-3.5. Volatility metrics include lexical volatility (edit distance) and semantic volatility (sentiment discrepancy) at feed and ticker levels.

Discussion 0