BigVAR: Tools for Modeling Sparse High-Dimensional Multivariate Time Series

Publication

Metrics

Paper Preview

Abstract

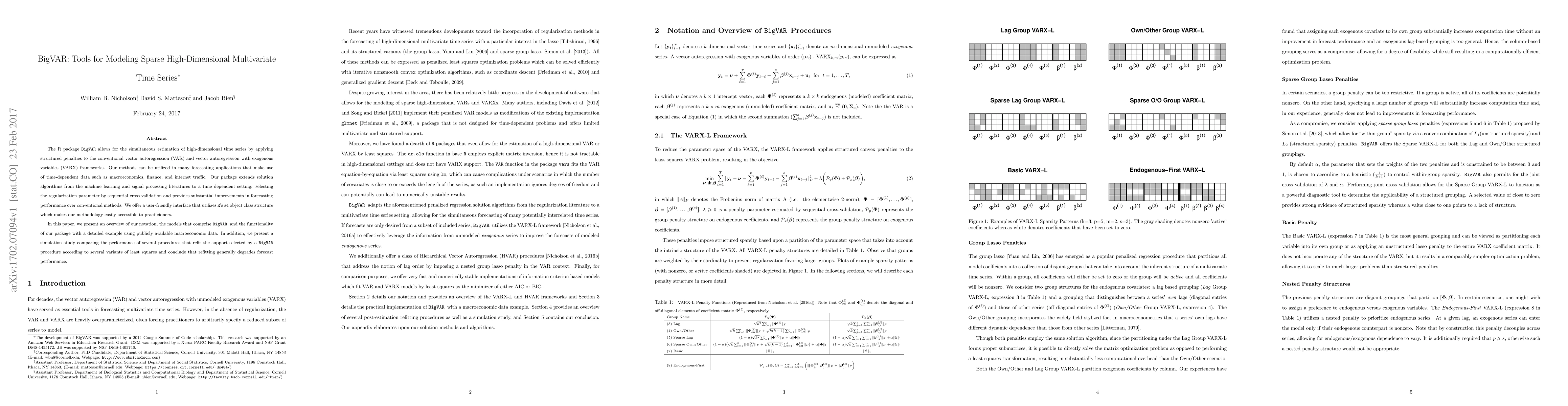

The R package BigVAR allows for the simultaneous estimation of high-dimensional time series by applying structured penalties to the conventional vector autoregression (VAR) and vector autoregression with exogenous variables (VARX) frameworks. Our methods can be utilized in many forecasting applications that make use of time-dependent data such as macroeconomics, finance, and internet traffic. Our package extends solution algorithms from the machine learning and signal processing literatures to a time dependent setting: selecting the regularization parameter by sequential cross validation and provides substantial improvements in forecasting performance over conventional methods. We offer a user-friendly interface that utilizes R's s4 object class structure which makes our methodology easily accessible to practicioners. In this paper, we present an overview of our notation, the models that comprise BigVAR, and the functionality of our package with a detailed example using publicly available macroeconomic data. In addition, we present a simulation study comparing the performance of several procedures that refit the support selected by a BigVAR procedure according to several variants of least squares and conclude that refitting generally degrades forecast performance.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0